How to Apply for an Online Loan (Step-by-Step to Get Approved Faster)

Applying for a loan online is quick and convenient, but many borrowers make mistakes that delay approval or increase costs.

Understanding the correct step-by-step process helps you apply confidently, get approved faster, and avoid common errors when borrowing money online.

Step 1: Understand What Type of Online Loan You Need

Before applying, you should clearly identify the type of loan that fits your needs.

Online loans include personal loans, instant loans, business loans, and lines of credit. Choosing the wrong type can lead to higher costs or repayment issues.

Think about your purpose—whether it’s an emergency, planned expense, or business need. Selecting the right loan ensures better terms and easier repayment.

If you’re unsure, reviewing an online loan guide helps you understand different loan types and choose wisely.

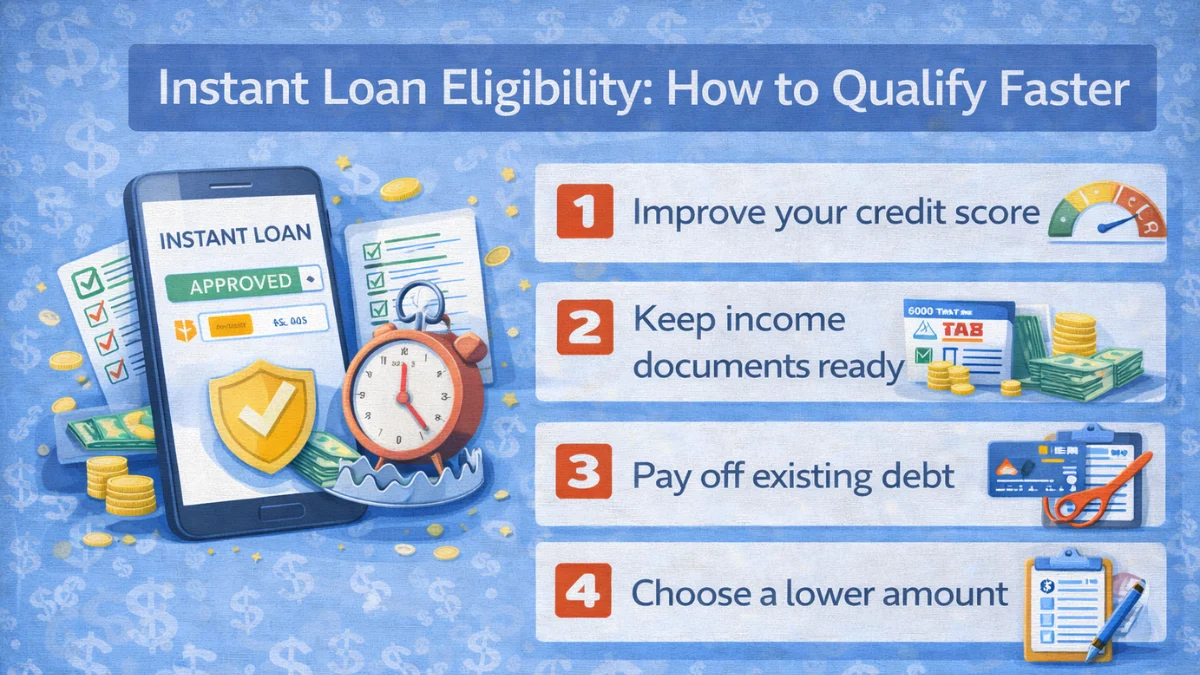

Step 2: Check Your Eligibility Before Applying

Checking your eligibility in advance saves time and prevents rejection.

Lenders evaluate factors such as your credit score, income, employment stability, and existing debts. Knowing where you stand helps you apply to the right lenders.

Some platforms also offer pre-check tools that don’t affect your credit score. This step is crucial for improving approval chances.

Understanding online loan eligibility helps you prepare your profile before submitting an application.

Step 3: Compare Online Lenders Carefully

Not all lenders offer the same interest rates, fees, or terms. Comparing multiple lenders helps you find the best deal and avoid overpaying.

Look at interest rates, processing fees, repayment terms, and customer reviews. Choosing the right lender can significantly reduce your total loan cost. Avoid rushing into the first offer you see.

Learning how to check online lender legit ensures you choose a safe and reliable provider.

Step 4: Gather Required Documents

Even though the process is digital, you still need to provide basic documents.

These may include identity proof, address proof, income details, and bank account information.

Having these documents ready speeds up the application process.

Make sure all details are accurate and up to date. Incorrect or incomplete information can lead to delays or rejection.

Understanding online loan eligibility helps you know what documents are required.

Step 5: Fill Out the Online Application Form

Once you’ve selected a lender, fill out the application form on their website or app. Provide accurate details about your personal information, income, and financial history.

Double-check all entries before submitting. Even small mistakes can cause delays or rejection. The application process is usually simple and takes only a few minutes.

Understanding online loan approval process helps you know what happens after submission.

Step 6: Complete Digital Verification (e-KYC)

After submitting your application, you’ll need to complete digital verification, often through e-KYC. This may include uploading documents or verifying your identity through OTP or video verification.

This step ensures your identity and reduces fraud risk. The process is usually quick and automated. Providing clear and accurate information ensures smooth verification.

Understanding protect from online loan scams helps you stay safe during this step.

Step 7: Wait for Loan Approval Decision

Once verification is complete, the lender evaluates your application using automated systems. This includes checking your credit score, income, and financial behavior.

Approval times can vary from a few minutes to a few days depending on the lender. If approved, you’ll receive a loan offer with terms and conditions.

Understanding online loan approval process helps you know how decisions are made.

Step 8: Review Loan Offer Carefully

Before accepting the loan, carefully review the offer details, including interest rate, repayment term, fees, and penalties.

Many borrowers skip this step and later face unexpected costs. Always calculate the total repayment amount, not just the monthly payment. If anything seems unclear, ask the lender for clarification.

Learning from online loan mistakes helps you avoid costly errors.

Step 9: Accept the Loan and Receive Funds

After reviewing the terms, you can accept the loan agreement digitally. Once accepted, the lender disburses the funds directly to your bank account.

This process can be very fast, especially with instant online loans. Ensure your bank details are correct to avoid delays.

Understanding online loan approval process helps you know how quickly funds can be transferred.

Step 10: Plan Your Repayment in Advance

Repayment planning is crucial for avoiding financial stress. Know your due dates, monthly payment amount, and total repayment cost.

Set reminders or enable auto-debit to avoid missing payments. Proper planning ensures you stay on track and maintain a good credit score.

Understanding after online loan application helps you know what to expect after receiving the loan.

Common Mistakes to Avoid When Applying Online

Many borrowers make mistakes such as applying without checking eligibility, choosing unverified lenders, or ignoring loan terms.

These errors can lead to rejection or higher costs. Taking time to prepare and review your application improves your chances of success.

Learning from online loan mistakes helps you avoid these issues and apply confidently.

Frequently Asked Questions

Conclusion

Applying for a loan online is simple when you follow the right steps.

From choosing the right loan type to comparing lenders and planning repayment, each step plays an important role in your financial journey.

By staying informed, avoiding common mistakes, and using insights from an online loan guide, you can apply confidently and secure the best loan terms.

The key is to be careful, prepared, and responsible when borrowing online.

I create mortgage calculator and loan calculators, along with Guides for Mortgagerateschecker, helping users understand mortgage rates, personal loans, auto loans, student loans, and overall loan affordability. Content is for educational purposes only and not financial advice.