How Much Auto Loan Can You Afford? (Avoid Overpaying Mistakes)

Before taking an auto loan, knowing how much you can truly afford is crucial to avoid financial stress.

Many buyers focus only on monthly payments, but affordability depends on income, expenses, loan terms, and interest rates.

Understanding this helps you make smarter car-buying decisions.

What Does Auto Loan Affordability Really Mean?

Auto loan affordability is not just about whether you can manage a monthly payment—it’s about whether the loan fits comfortably within your overall financial situation.

Many borrowers make the mistake of stretching their budget to afford a higher-priced car, only to struggle later.

True affordability considers your income, fixed expenses, savings goals, and lifestyle.

Financial experts often recommend keeping your car payment within a reasonable percentage of your monthly income.

Before deciding, it’s important to calculate realistic numbers using an auto loan calculator so you understand what you can safely afford without financial pressure.

The 20/4/10 Rule for Auto Loan Budgeting

One of the most effective ways to determine affordability is the 20/4/10 rule.

This guideline suggests putting at least 20% down, choosing a loan term of no more than four years, and keeping total car expenses under 10% of your monthly income.

This approach helps reduce interest costs and prevents long-term debt.

While not everyone can follow this rule exactly, it provides a strong baseline for smart borrowing.

Understanding these principles alongside auto loan term length options helps you balance affordability and total loan cost effectively.

How Your Income and Expenses Affect Loan Affordability

Your income plays a major role in determining how much auto loan you can afford, but your expenses are equally important.

Lenders look at your debt-to-income ratio to evaluate your ability to repay the loan. High existing debts can limit your borrowing capacity, even if your income is strong.

It’s essential to review your monthly expenses, including rent, utilities, and other loans, before committing to a car loan.

Knowing how auto loan approval factors work can help you assess your financial position and improve your chances of getting better loan terms.

Why Monthly Payment Alone Can Be Misleading

Many buyers focus only on whether they can afford the monthly payment, but this can lead to costly mistakes.

A lower monthly payment often comes from extending the loan term, which increases total interest paid over time.

This means you may end up paying significantly more for the same car.

Instead of focusing only on monthly affordability, consider the total cost of the loan.

Learning how auto loan monthly payments work helps you understand the full financial impact and avoid overpaying in the long run.

The Impact of Interest Rates on Affordability

Interest rates directly affect how much you pay over the life of your auto loan. Even a small increase in the rate can significantly raise your monthly payment and total cost.

Borrowers with higher credit scores usually qualify for lower rates, making the loan more affordable.

Improving your credit before applying can save you a substantial amount of money.

Understanding how auto loan interest works allows you to compare offers, negotiate better terms, and reduce your overall borrowing cost.

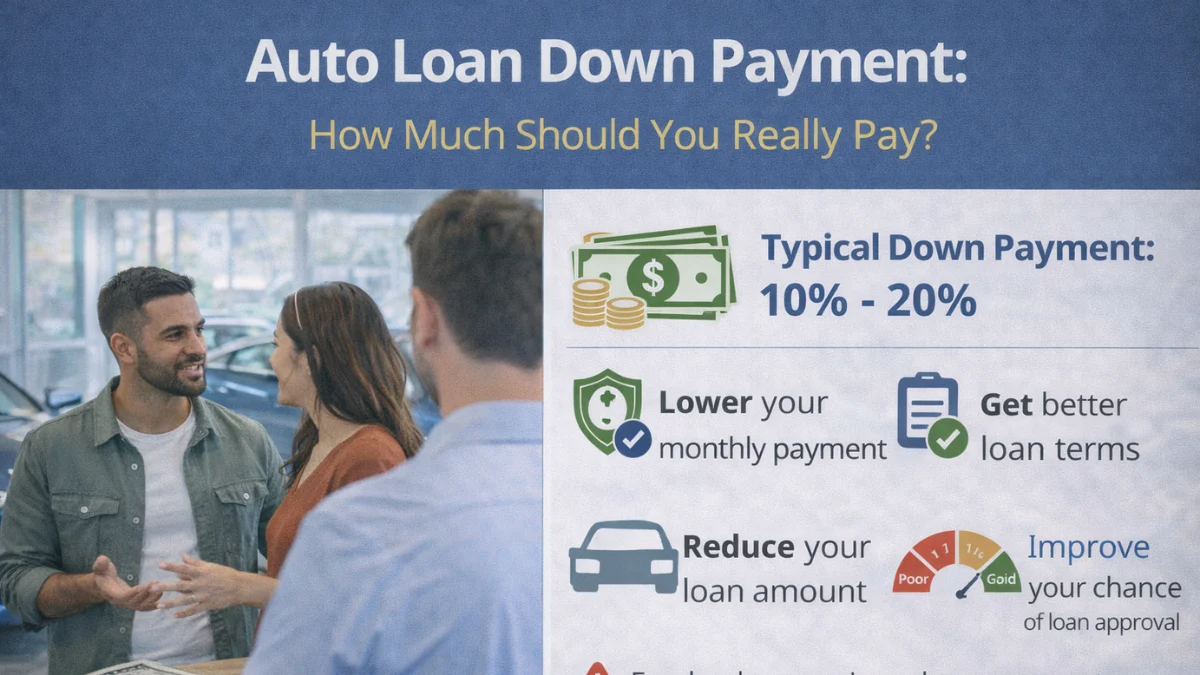

How Much Down Payment Should You Make?

A larger down payment reduces the amount you need to borrow, which lowers both your monthly payments and total interest.

It also improves your chances of approval and may help you secure better interest rates. While some lenders offer zero-down financing, this often results in higher long-term costs.

Financially, it’s safer to put down at least 10%–20% of the car price.

Exploring auto loan down payment strategies can help you make smarter decisions and reduce financial risk.

Choosing the Right Loan Term for Your Budget

Loan term length plays a critical role in affordability. Shorter terms like 36 or 48 months have higher monthly payments but lower total interest.

Longer terms like 60 or 72 months reduce monthly payments but increase overall cost.

Many buyers choose longer terms to make payments manageable, but this can lead to paying more than the car’s value over time.

Understanding auto loan term length options helps you choose a loan that fits your budget without increasing long-term financial burden.

Hidden Costs That Affect Your Real Affordability

The true cost of an auto loan goes beyond monthly payments.

Expenses such as insurance, maintenance, taxes, registration fees, and fuel can significantly impact your budget.

Many borrowers overlook these costs when calculating affordability, leading to financial strain later. It’s important to factor in all ownership costs before deciding how much you can borrow.

Learning about auto loan hidden fees ensures you understand the full financial picture and avoid unexpected expenses.

How to Avoid Overpaying on an Auto Loan

Avoiding overpayment starts with proper planning and informed decision-making.

Compare multiple lenders, negotiate interest rates, and avoid unnecessary add-ons offered by dealerships.

Stick to your budget and resist the temptation to upgrade beyond what you can afford. Pre-approval can also help you secure better terms and stay within your financial limits.

Following strategies from auto loan mistakes to avoid can save you thousands over the life of your loan.

Frequently Asked Questions

Conclusion

Understanding how much auto loan you can afford is essential to making a smart financial decision.

It’s not just about monthly payments but the total cost, interest rates, and long-term impact on your budget.

By using tools like an auto loan calculator, considering all expenses, and choosing the right loan terms, you can avoid overpaying and stay financially secure.

A well-planned auto loan ensures you enjoy your car without unnecessary financial stress.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.