What Affects Your Auto Loan Approval? (Lenders’ Secret Criteria)

Auto loan approval isn’t random—lenders follow specific criteria to decide whether you qualify and what interest rate you get.

Many borrowers get rejected or overpay simply because they don’t understand these factors.

Knowing what lenders look for can help you get approved faster and secure better terms.

How Auto Loan Approval Really Works Behind the Scenes

When you apply for an auto loan, lenders evaluate your financial profile to determine how risky it is to lend you money.

They use a mix of data, including your credit history, income stability, and current debts, to decide whether to approve your application and at what interest rate.

This process is designed to minimize risk for the lender. Even if two borrowers apply for the same loan, their terms can differ significantly.

Understanding how auto loans work helps you see why approval is not just about applying—it’s about how strong your financial profile looks to lenders.

Credit Score: The Most Important Factor

Your credit score is the single biggest factor affecting your auto loan approval. It reflects your past borrowing behavior and how reliably you repay debt.

Higher credit scores usually result in faster approvals and lower interest rates, while lower scores may lead to higher rates or rejection.

Even a small improvement in your score can make a big difference. Before applying, it’s important to check your credit report and fix any errors.

Learning how auto loan interest works helps you understand how your credit score directly impacts the cost of borrowing.

Income and Employment Stability

Lenders want to ensure that you have a stable source of income to repay the loan.

They typically look at your monthly income, job history, and employment type. A consistent income stream reduces risk and improves your chances of approval.

Self-employed borrowers may need to provide additional documentation. If your income is unstable, lenders may hesitate to approve your application.

Understanding how to get auto loan approval fast helps you prepare the right documents and present a strong financial profile.

Debt-to-Income Ratio (DTI) Explained

Your debt-to-income ratio (DTI) measures how much of your income goes toward existing debts.

A lower DTI indicates that you have enough income to manage a new loan, making you a safer borrower.

High DTI can reduce your approval chances or result in higher interest rates. Lenders prefer borrowers with balanced financial obligations.

Calculating your affordability using an auto loan calculator helps you understand how much loan you can handle without exceeding safe limits.

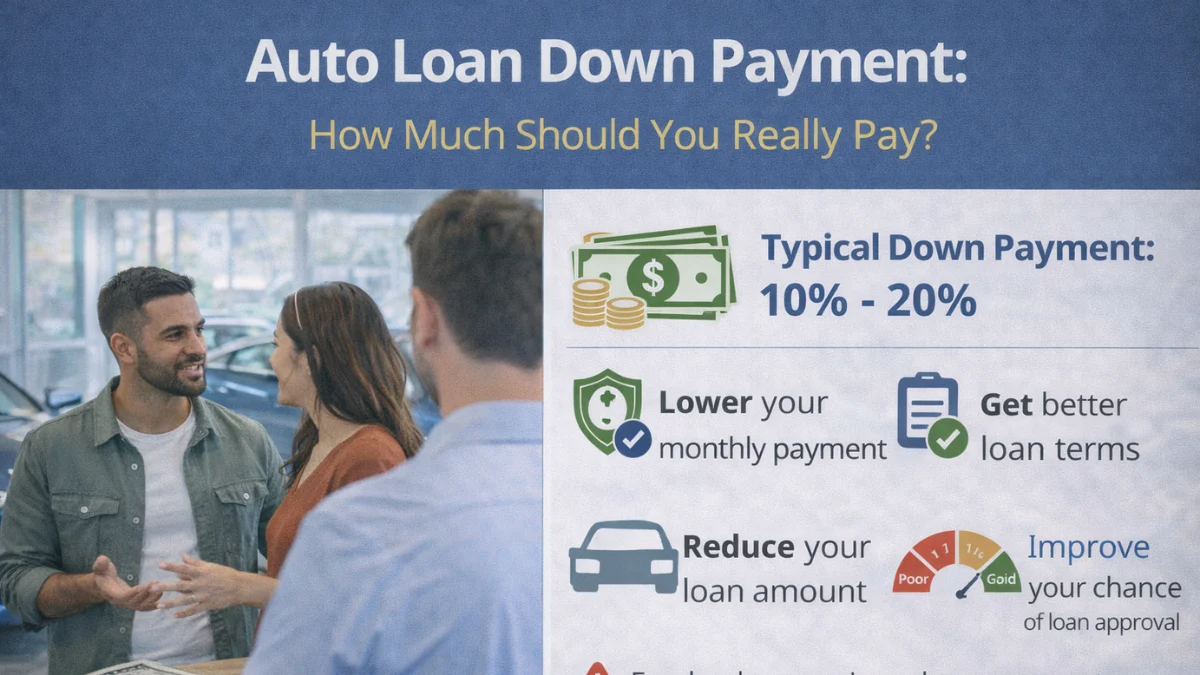

Down Payment: A Key Approval Booster

A higher down payment significantly improves your chances of auto loan approval.

It reduces the loan amount and shows lenders that you are financially committed.

This lowers their risk and may help you secure better interest rates. Even if you have a lower credit score, a strong down payment can offset some of the risk.

Understanding auto loan down payment strategies helps you use this factor to your advantage when applying for a loan.

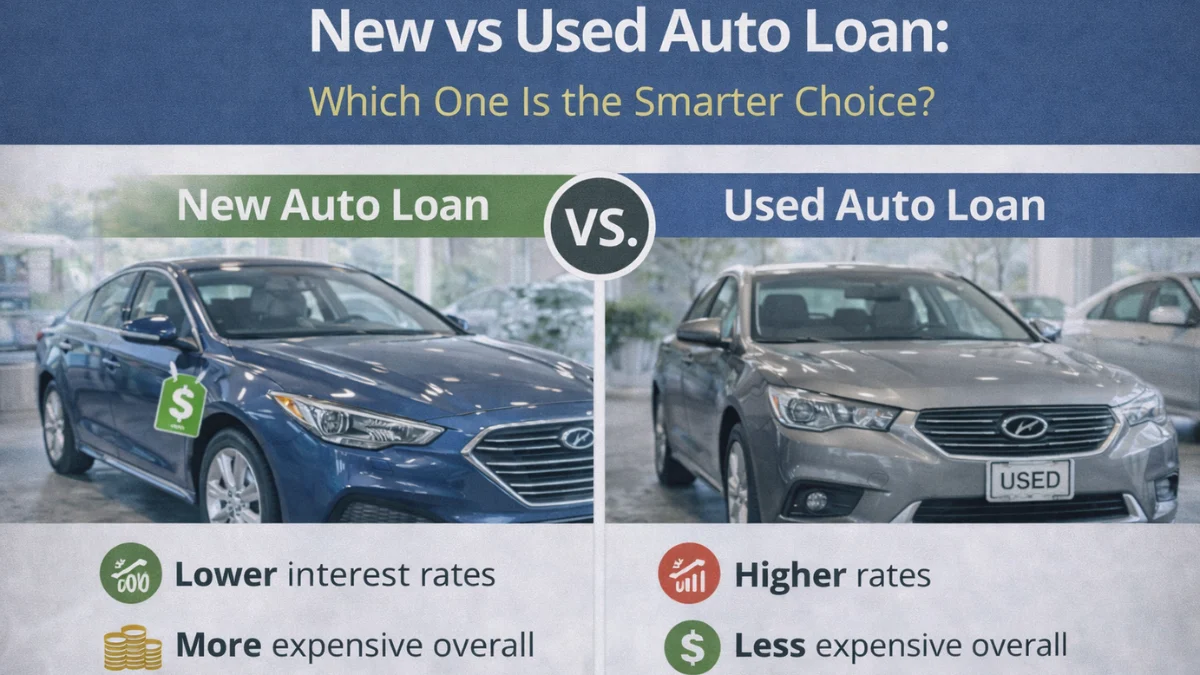

Loan Amount and Car Type Matter

The amount you borrow and the type of car you choose also influence approval.

Lenders assess whether the loan amount is reasonable compared to your income and the car’s value.

New cars are generally easier to finance because they have higher resale value, while older vehicles may come with stricter conditions.

Applying for a realistic loan amount increases your chances of approval.

Learning about auto loan affordability planning helps you choose a loan that aligns with your financial capacity.

Credit History and Payment Behavior

Beyond your credit score, lenders also analyze your credit history in detail.

They look at your past payment behavior, including late payments, defaults, and outstanding debts.

A history of missed payments can raise red flags and reduce approval chances. On the other hand, consistent on-time payments build trust with lenders.

Understanding auto loan default consequences helps you see how past behavior affects your future borrowing ability.

The Impact of Loan Term Length

Loan term length can also affect approval decisions. Longer loan terms reduce monthly payments, making the loan appear more affordable, which may improve approval chances.

However, they increase total interest costs. Shorter terms may be harder to qualify for due to higher monthly payments.

Choosing the right term is crucial for balancing approval and affordability.

Exploring auto loan term length options helps you select a loan structure that works for both you and the lender.

Why Pre-Approval Increases Your Chances

Getting pre-approved can significantly improve your chances of final approval. It shows sellers and lenders that you are a serious buyer with verified financial credentials.

Pre-approval also helps you understand your budget and avoid applying for unrealistic loan amounts. This reduces the likelihood of rejection.

Learning about auto loan pre-approval benefits ensures you enter the process prepared and confident.

Common Mistakes That Hurt Your Approval Chances

Many borrowers unknowingly reduce their approval chances by making avoidable mistakes.

Applying for multiple loans at once, ignoring their credit score, or providing incomplete information can delay or harm approval.

Taking on new debt before applying can also negatively impact your profile.

To improve your chances, it’s important to avoid these errors. Following guidance from auto loan mistakes to avoid helps you present a stronger application.

Frequently Asked Questions

Conclusion

Auto loan approval depends on multiple factors, including your credit score, income, debt, and loan details.

Understanding these criteria helps you prepare a strong application and avoid unnecessary delays or rejections.

By improving your financial profile, choosing a realistic loan amount, and using tools like an auto loan calculator, you can increase your chances of approval and secure better terms.

The more informed you are, the easier it becomes to get approved and finance your car with confidence.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.