How Auto Loan Interest Works (And How to Pay Less Over Time)

Auto loan interest is one of the biggest factors that determines how much you actually pay for your car.

Many borrowers focus only on monthly payments without realizing how interest increases total cost.

Understanding how auto loan interest works can help you save thousands over time.

What Is Auto Loan Interest and Why It Matters

Auto loan interest is the cost you pay to borrow money from a lender to purchase a car.

It is usually expressed as an annual percentage rate (APR) and directly affects your total loan cost.

Even a small difference in interest rate can significantly increase how much you pay over time.

Many first-time borrowers underestimate this impact and focus only on affordability.

Understanding how auto loans work helps you see why interest is a critical factor in every financing decision and why choosing the right loan terms matters.

How Auto Loan Interest Is Calculated

Auto loan interest is typically calculated using a simple interest formula based on your remaining loan balance.

This means interest is charged on the outstanding amount, not the original loan every time.

As you make payments, more of your money goes toward reducing the principal, which lowers future interest charges.

However, in the early months, a larger portion of your payment goes toward interest.

To clearly understand how this affects your payments, you can use an auto loan calculator to break down principal vs interest over time.

Fixed vs Variable Interest Rates Explained

Most auto loans come with fixed interest rates, meaning your rate stays the same throughout the loan term. This provides predictable monthly payments and stability.

Some lenders may offer variable rates, which can change over time based on market conditions.

While variable rates may start lower, they can increase and make your loan more expensive. For most borrowers, fixed rates are safer and easier to manage.

Understanding auto loan term length options alongside interest types helps you choose a loan that fits your financial comfort level.

How Interest Affects Your Monthly Payments

Interest plays a major role in determining your monthly auto loan payments.

Higher interest rates increase your monthly payment and total repayment amount, while lower rates make the loan more affordable.

However, loan term also affects this relationship—longer terms reduce monthly payments but increase total interest paid.

Many borrowers choose lower monthly payments without realizing the long-term cost.

Learning about auto loan monthly payments helps you balance affordability with total loan cost effectively.

The Total Cost of Interest Over Time

The total interest you pay over the life of your loan can be surprisingly high, especially with longer loan terms.

For example, extending your loan from 36 to 72 months may lower your monthly payment but significantly increase total interest.

This is why focusing only on monthly affordability can be misleading.

Instead, you should always evaluate the full cost of borrowing.

Using an auto loan affordability guide helps you understand how interest accumulates and how to minimize it.

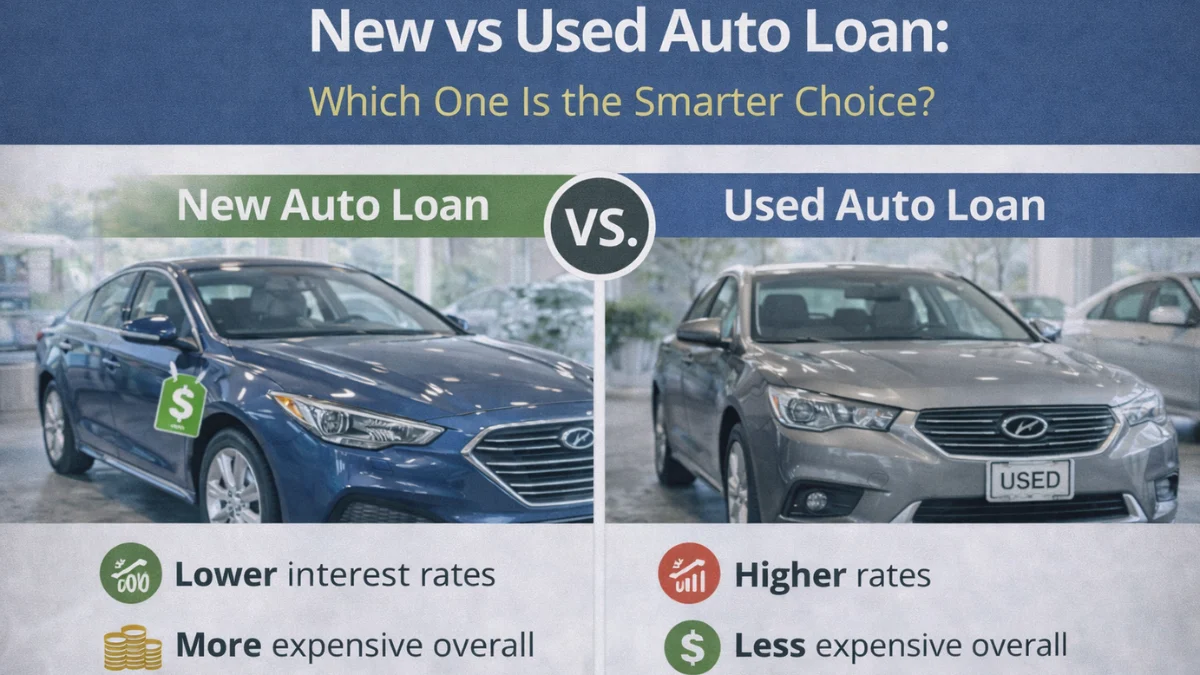

Factors That Affect Your Auto Loan Interest Rate

Several factors determine the interest rate you receive on an auto loan. Your credit score is the most important—higher scores qualify for lower rates.

Other factors include your income, employment history, loan term, and the type of car you’re purchasing.

New cars often come with lower rates than used cars. Lenders also consider your down payment and debt-to-income ratio.

Understanding auto loan approval factors helps you improve your profile and secure better interest rates.

How to Reduce Auto Loan Interest (Smart Strategies)

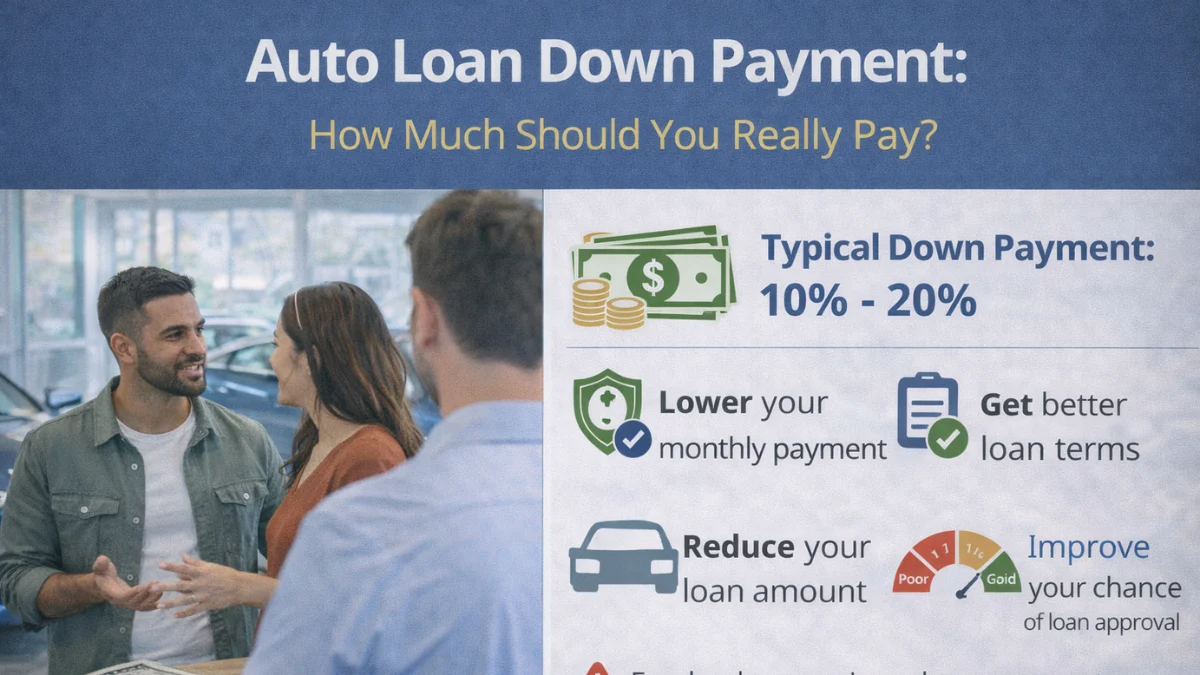

Reducing your auto loan interest starts before you even apply. Improving your credit score, comparing multiple lenders, and making a larger down payment can all help you secure lower rates.

Choosing a shorter loan term also reduces total interest, even if monthly payments are higher. Negotiating with lenders and avoiding dealer-only financing can also save money.

Following tips from auto loan mistakes to avoid ensures you don’t overpay due to poor decisions.

Paying Off Your Loan Early to Save Interest

One of the most effective ways to reduce interest is by paying off your loan early.

Making extra payments toward the principal reduces your outstanding balance faster, which lowers future interest charges.

Even small additional payments can make a big difference over time.

However, it’s important to check for prepayment penalties before doing this.

Exploring auto loan refinancing options can also help you secure better terms and reduce interest if your financial situation improves.

Refinancing to Lower Your Interest Rate

Refinancing allows you to replace your current auto loan with a new one at a lower interest rate.

This can reduce your monthly payments or shorten your loan term, saving you money over time. It’s especially beneficial if your credit score has improved since you first took the loan.

However, refinancing may involve fees, so it’s important to calculate whether the savings outweigh the costs.

Understanding auto loan refinancing options helps you decide when refinancing is the right move.

Common Interest Mistakes Borrowers Make

Many borrowers make the mistake of focusing only on monthly payments rather than total interest cost. Others fail to compare lenders or accept high dealer rates without negotiation.

Choosing long loan terms or skipping a down payment can also increase interest significantly. Not understanding how interest works leads to overpaying.

Learning from auto loan mistakes to avoid helps you make smarter financial decisions and minimize unnecessary costs.

Frequently Asked Questions

Conclusion

Understanding how auto loan interest works is essential for making a smart financial decision.

Interest affects not only your monthly payments but also the total cost of your loan.

By improving your credit, choosing the right loan term, and using tools like an auto loan calculator, you can significantly reduce how much you pay over time.

The key is to focus on total cost, not just monthly affordability, and take proactive steps to minimize interest expenses.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.