10 Auto Loan Mistakes That Cost Buyers Thousands (Avoid These!)

Auto loans make car buying easier, but small mistakes can cost you thousands over time.

Many buyers rush the process without understanding interest, loan terms, or hidden fees.

By knowing the most common auto loan mistakes, you can avoid financial stress and make smarter decisions.

Focusing Only on Monthly Payments

One of the biggest mistakes buyers make is focusing only on the monthly payment instead of the total loan cost.

Dealers often lower monthly payments by extending the loan term, which increases total interest paid over time.

This can make a car seem affordable while actually costing much more in the long run.

Instead of looking only at monthly affordability, always consider the full repayment amount.

Using an auto loan calculator helps you see the total cost and avoid falling into this common trap.

Not Checking Your Credit Score Before Applying

Your credit score directly affects your interest rate and loan approval.

Many borrowers apply without checking their score, only to receive higher rates than expected. Errors in your credit report can also negatively impact your application.

Reviewing your credit score in advance allows you to fix issues and improve your profile.

Understanding auto loan approval factors helps you prepare better and secure more favorable loan terms.

Choosing a Loan Term That’s Too Long

Longer loan terms, such as 72 months or more, may reduce your monthly payment but significantly increase the total interest paid.

This means you end up paying far more for the same car.

Longer terms also increase the risk of negative equity. While lower payments may seem attractive, they often lead to higher long-term costs.

Learning about auto loan term length options helps you choose a term that balances affordability with total savings.

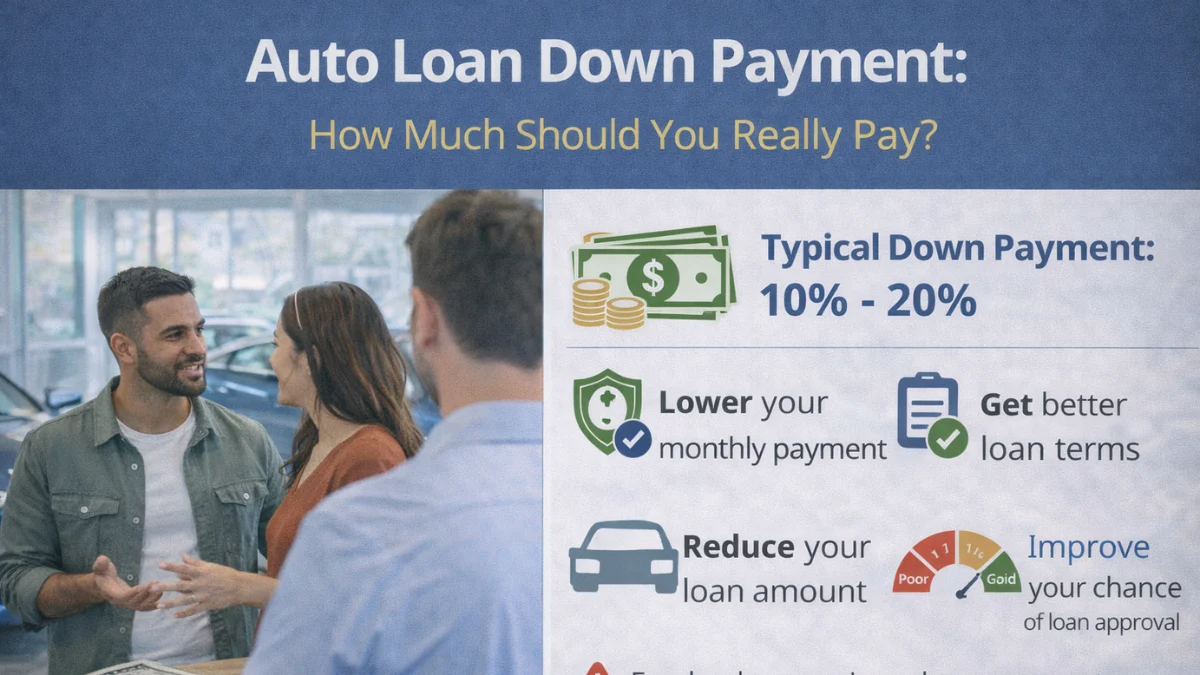

Skipping the Down Payment

Many buyers opt for zero down payment loans to reduce upfront costs, but this increases the loan amount and total interest.

Without a down payment, you may also face higher interest rates and greater financial risk.

A reasonable down payment reduces your borrowing amount and improves loan terms.

Exploring auto loan down payment strategies helps you minimize costs and secure better financing options.

Not Comparing Multiple Lenders

Accepting the first loan offer you receive can be a costly mistake. Different lenders offer different interest rates, terms, and fees.

Without comparing options, you may end up paying more than necessary. Shopping around allows you to find the best deal and negotiate better terms.

Understanding how auto loan interest works helps you evaluate offers effectively and choose the most affordable option.

Ignoring Hidden Fees and Extra Costs

Auto loans often include additional fees such as processing charges, documentation fees, and insurance add-ons.

Many buyers overlook these costs, which can increase the total loan amount.

Some lenders may also include unnecessary extras that add to your monthly payment.

It’s important to review all charges before signing any agreement.

Learning about auto loan hidden fees ensures you understand the true cost of your loan.

Not Getting Pre-Approved Before Buying

Skipping pre-approval puts you at a disadvantage when negotiating with dealers.

Without pre-approval, you may rely on dealership financing, which often comes with higher interest rates. Pre-approval gives you a clear bud

get and better negotiating power. It also speeds up the buying process.

Understanding auto loan pre-approval benefits helps you secure better loan terms and avoid unnecessary costs.

Borrowing More Than You Can Afford

Many buyers stretch their budget to purchase a more expensive car, leading to financial strain later.

High monthly payments can affect your ability to manage other expenses and savings. It’s important to choose a loan amount that fits comfortably within your budget.

Calculating affordability using an auto loan affordability guide helps you avoid overborrowing and maintain financial stability.

Not Understanding Interest and Total Cost

Some borrowers don’t fully understand how interest works, leading them to underestimate the total cost of the loan.

Even a small increase in interest rate can significantly raise the amount you pay over time.

Understanding how interest accumulates helps you make better decisions when choosing a loan.

Learning how auto loan interest works ensures you don’t overpay due to lack of knowledge.

Ignoring Early Repayment or Refinancing Options

Many borrowers stick with their original loan terms without considering better options later.

If your credit score improves or interest rates drop, refinancing can help reduce your monthly payments or total cost.

Similarly, making extra payments can lower your interest burden. Exploring auto loan refinancing options helps you take advantage of opportunities to save money over time.

Frequently Asked Questions

Conclusion

Avoiding common auto loan mistakes can save you thousands and protect your financial health.

From understanding interest rates to choosing the right loan term and comparing lenders, every step matters.

By planning carefully, using tools like an auto loan calculator, and making informed decisions, you can secure a loan that fits your budget.

The key is to focus on total cost, not just monthly payments, and avoid shortcuts that lead to long-term expenses.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.