How Auto Loan Monthly Payments Are Calculated (With Examples)

Understanding how auto loan monthly payments are calculated is essential before financing a car.

Many buyers focus only on affordability without knowing what actually determines their payment.

By learning how loan amount, interest rate, and term work together, you can avoid costly mistakes and plan smarter.

What Determines Your Auto Loan Monthly Payment?

Your monthly auto loan payment is calculated based on three main factors: the loan amount, interest rate, and loan term. The loan amount is the total money you borrow after your down payment.

The interest rate determines the cost of borrowing, and the loan term decides how long you’ll repay it. These three elements work together to define your monthly obligation.

Many buyers ignore this relationship and focus only on monthly affordability. To get a clear estimate, using an auto loan calculator helps you understand how these variables affect your payments before applying.

The Basic Formula Behind Auto Loan Payments

Auto loan payments are calculated using a standard amortization formula that spreads the loan amount and interest over the loan term.

While the formula itself may seem complex, the concept is simple—you repay a portion of the principal plus interest each month.

Early payments include more interest, while later payments reduce the principal faster.

This is why understanding the calculation is important for long-term savings.

Learning how auto loans work helps you see how each payment contributes to reducing your loan balance over time.

Example 1: Simple Auto Loan Calculation

Let’s say you take a loan of $25,000 at an interest rate of 8% for 60 months. Your monthly payment would be approximately $507.

Over five years, you’ll pay both the principal and interest, with total interest adding a noticeable amount to your overall cost.

This example shows how even moderate interest rates can increase total repayment.

Using an auto loan monthly payment guide helps you break down these numbers and understand how much you’ll actually pay over time.

Example 2: How Loan Term Changes Your Payment

Now consider the same $25,000 loan at 8% interest, but with different loan terms.

At 36 months, your monthly payment would be higher, but total interest would be lower.

At 72 months, your monthly payment would drop, but total interest would increase significantly.

This demonstrates the trade-off between affordability and cost. Many borrowers choose longer terms for lower payments without realizing the long-term impact.

Understanding auto loan term length options helps you make a smarter decision based on your financial goals.

How Interest Rate Impacts Monthly Payments

Interest rates play a major role in determining your monthly payment.

A lower interest rate reduces both your monthly payment and total cost, while a higher rate increases both. Even a 1–2% difference can significantly change your payment amount.

Borrowers with higher credit scores usually qualify for better rates, making loans more affordable.

Learning how auto loan interest works helps you compare offers and choose the most cost-effective option.

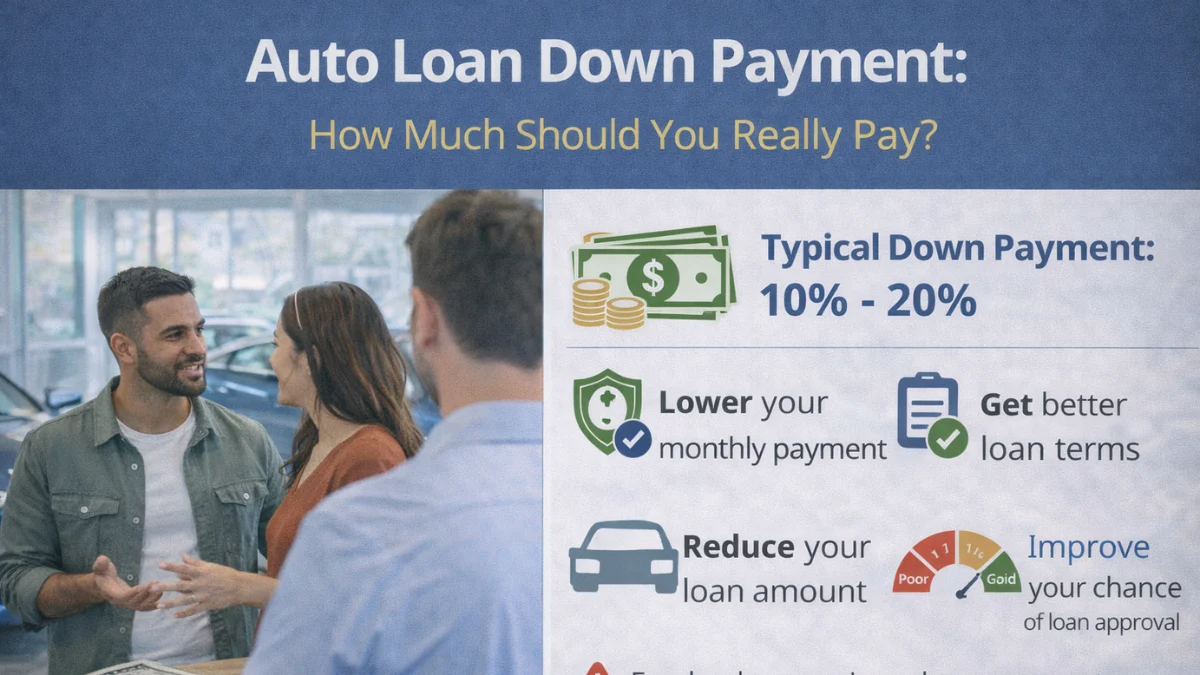

The Role of Down Payment in Monthly Payments

A larger down payment reduces your loan amount, which directly lowers your monthly payment.

For example, paying $5,000 upfront on a $30,000 car reduces your loan to $25,000, resulting in lower payments and less interest.

This can also improve your chances of approval and help you secure better loan terms.

However, you should balance your down payment with your savings.

Understanding auto loan down payment strategies helps you reduce your financial burden without exhausting your funds.

Hidden Costs That Affect Your Monthly Payment

Your monthly auto loan payment may include more than just principal and interest. Taxes, registration fees, insurance, and dealer charges can increase your overall payment.

Some lenders may also include add-ons like extended warranties.

Ignoring these costs can lead to underestimating your budget. Before finalizing your loan, it’s important to calculate the full cost.

Learning about auto loan hidden fees ensures you avoid surprises and plan your finances accurately.

How to Lower Your Monthly Auto Loan Payment

There are several ways to reduce your monthly auto loan payment.

You can increase your down payment, choose a longer loan term, or secure a lower interest rate. Improving your credit score before applying can also help you qualify for better terms.

However, extending the loan term should be done carefully, as it increases total interest.

Following strategies from auto loan affordability planning helps you balance lower payments with long-term savings.

Common Mistakes When Calculating Payments

Many borrowers rely on rough estimates instead of accurate calculations, leading to financial surprises later.

Others focus only on monthly payments without considering total cost or interest.

Ignoring additional fees and choosing long loan terms without understanding their impact are also common mistakes.

To avoid these issues, it’s important to use proper tools and compare options carefully.

Learning from auto loan mistakes to avoid helps you make more informed financial decisions.

Frequently Asked Questions

Conclusion

Understanding how auto loan monthly payments are calculated helps you make smarter financial decisions when buying a car.

By considering loan amount, interest rate, and term length, you can estimate your payments accurately and avoid overpaying.

Using tools like an auto loan calculator and evaluating all costs ensures you stay within your budget.

The key is to balance affordability with long-term savings so your car purchase remains financially sustainable.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.