Auto Loan vs Leasing: Which Option Saves You More Money?

When buying a car, one of the biggest decisions is whether to take an auto loan or lease a vehicle.

Both options offer advantages, but the real question is which one saves you more money.

Understanding the differences in cost, ownership, and long-term value is essential before making a decision.

What Is the Difference Between Auto Loan and Leasing?

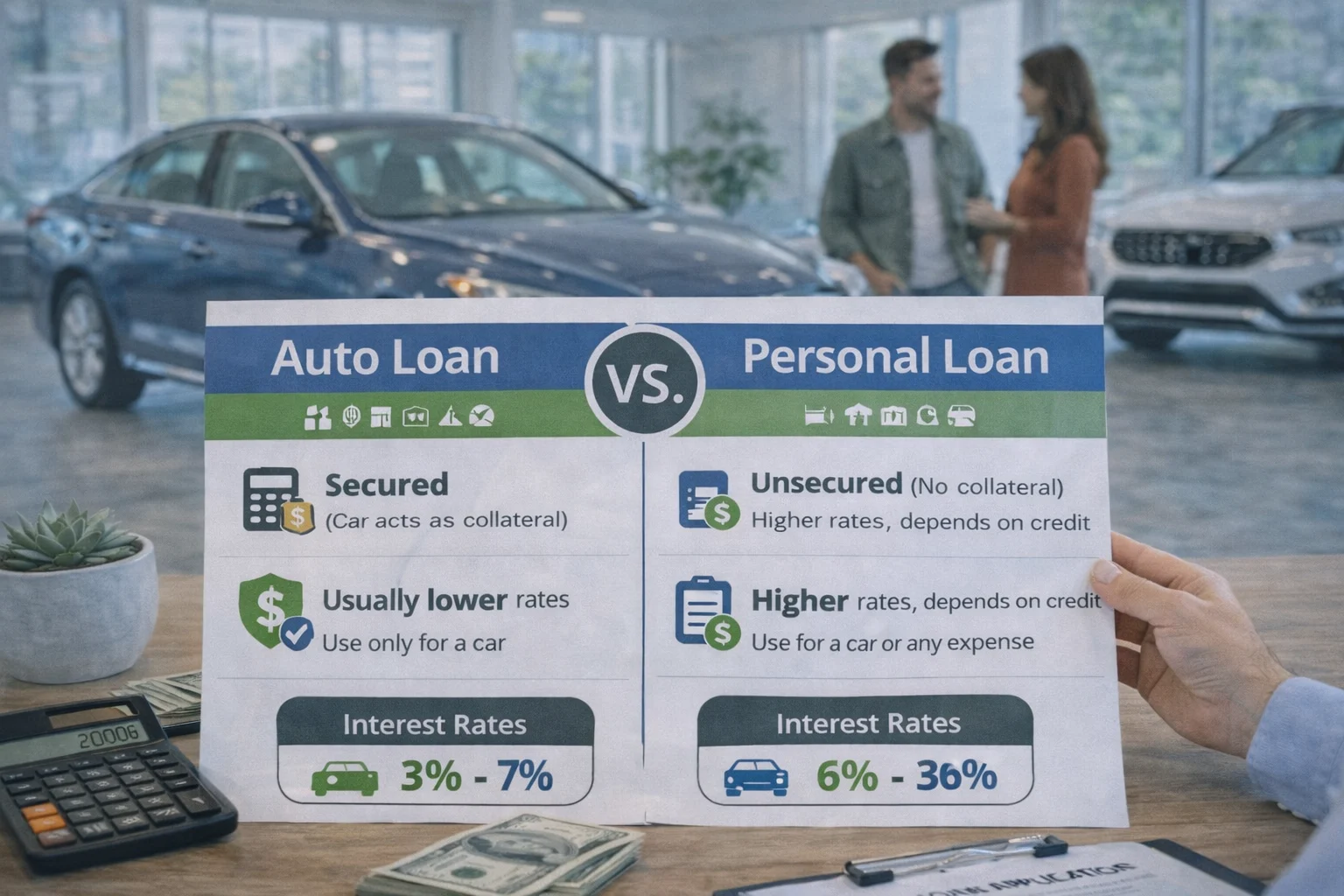

An auto loan allows you to borrow money to purchase a car, which you eventually own after completing all payments.

Leasing, on the other hand, is like renting a car for a fixed period, typically 2–4 years, with no ownership at the end unless you choose to buy it.

With a loan, your payments go toward building equity, while lease payments only cover depreciation and usage.

Understanding this core difference is essential before deciding. If you’re new to financing, start by learning how auto loans work to see how ownership impacts your long-term finances.

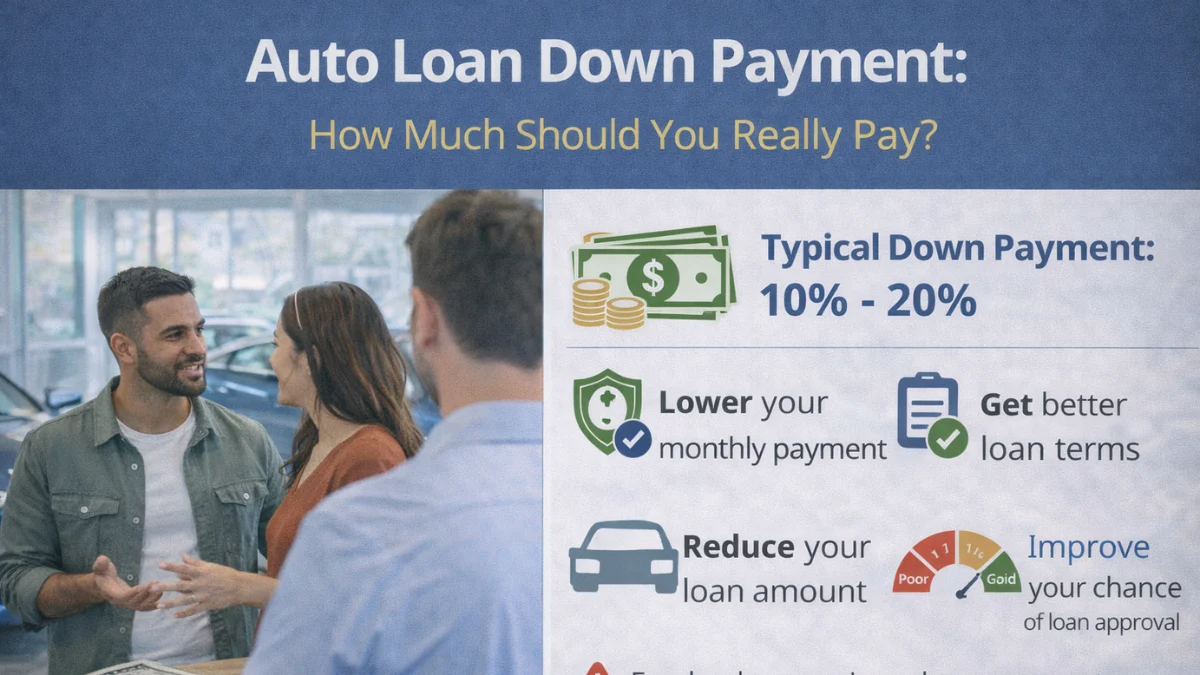

Which Option Has Lower Monthly Payments?

Leasing usually offers lower monthly payments compared to auto loans because you’re only paying for the vehicle’s depreciation during the lease term.

Auto loans have higher monthly payments since you’re paying off the entire car value plus interest.

However, lower payments don’t always mean better savings. Leasing may seem more affordable upfront, but you don’t gain any ownership.

Before deciding, calculate your estimated payments using an auto loan calculator to compare real costs and understand which option fits your budget.

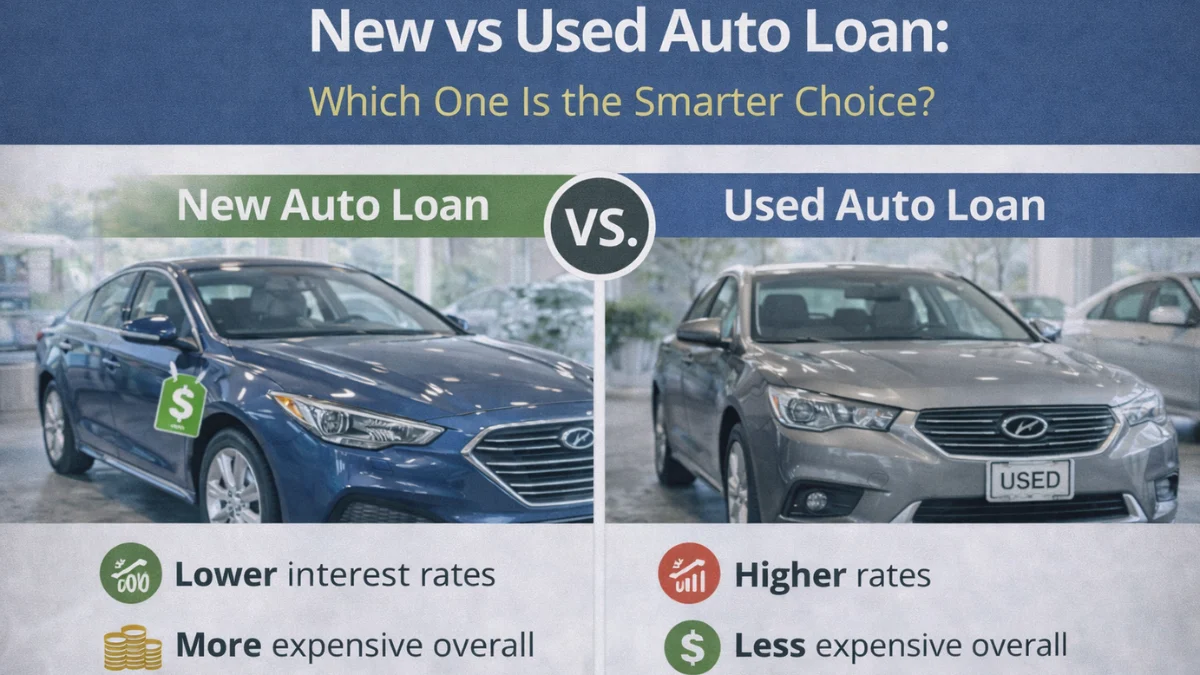

Total Cost Comparison: Loan vs Lease Over Time

While leasing offers lower monthly payments, the total cost over time can be higher if you continue leasing vehicles repeatedly.

With an auto loan, once you complete payments, you own the car and no longer have monthly obligations.

This makes auto loans more cost-effective in the long run for many buyers. Leasing, however, may cost less in the short term but creates ongoing expenses.

Understanding the full financial picture, including auto loan monthly payments, helps you avoid focusing only on short-term savings.

Ownership vs No Ownership: Why It Matters

Ownership is one of the biggest advantages of an auto loan. Once the loan is paid off, the car becomes a valuable asset that you can keep, sell, or trade.

Leasing offers no ownership unless you pay a buyout price at the end. For buyers who prefer long-term value, loans are usually the better option.

However, if you prefer driving new cars frequently without worrying about resale value, leasing might suit your lifestyle.

Knowing the benefits of ownership through auto loan affordability planning helps you make a financially sound decision.

Flexibility and Restrictions: Loan vs Lease

Auto loans provide full flexibility—you can drive as much as you want, customize your vehicle, and sell it anytime.

Leasing, however, comes with restrictions such as mileage limits, wear-and-tear charges, and penalties for early termination.

These restrictions can increase your overall cost if not managed carefully. If you drive long distances or plan to modify your car, leasing may not be ideal.

Understanding these limitations alongside auto loan term length options helps you choose the right financing method based on your lifestyle.

Interest Rates and Financial Impact

Interest rates play a key role in auto loan costs, while leasing involves a money factor (similar to interest).

Borrowers with strong credit can secure lower interest rates, making auto loans more affordable. Leasing may offer attractive deals, but hidden costs and fees can add up.

Improving your credit score before applying can significantly reduce borrowing costs.

Learning how auto loan interest works helps you compare financing options more effectively and choose the one that saves you money.

Which Option Is Better for First-Time Buyers?

For first-time car buyers, auto loans are often the better option because they build ownership and financial stability over time.

Leasing can be appealing due to lower monthly payments, but it doesn’t contribute to long-term asset building.

Additionally, loans provide more flexibility and fewer restrictions.

If you’re just starting out, understanding auto loan approval factors can help you prepare better and secure a loan that fits your budget.

When Leasing Might Be the Better Choice

Leasing can be a good option if you prefer lower monthly payments, drive a new car every few years, and don’t want to deal with maintenance costs of older vehicles.

It’s also ideal for people who drive limited miles annually and want predictable expenses. However, leasing is not ideal for those looking to save money long-term.

Comparing scenarios using auto loan vs leasing options helps you determine whether leasing aligns with your financial goals.

Common Mistakes When Choosing Between Loan and Lease

Many buyers make the mistake of choosing leasing simply because of lower monthly payments without considering long-term costs.

Others take auto loans without evaluating interest rates or loan terms properly.

Not comparing multiple lenders or ignoring hidden fees can also lead to overpaying.

To make the right decision, it’s important to research both options thoroughly.

Learning from auto loan mistakes to avoid helps you avoid costly errors and make a smarter financial choice.

Frequently Asked Questions

Conclusion

Choosing between an auto loan and leasing depends on your financial goals, driving habits, and long-term plans.

While leasing offers lower monthly payments and flexibility in driving new cars, auto loans provide ownership and better long-term value.

By comparing total costs, understanding restrictions, and using tools like an auto loan calculator, you can make a smart decision that fits your budget.

Ultimately, the best option is the one that balances affordability with long-term financial benefits.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.