Conventional vs FHA vs VA Loans: Which Mortgage Is Best for You in 2026?

Compare conventional, FHA, and VA loans side by side. Learn differences in rates, eligibility, down payments, and choose the best mortgage option for your financial situation in 2026.

Choosing the right mortgage loan is one of the most important decisions buyers make, especially the first time around.

Conventional, FHA, and VA loans are the most common options, yet many buyers don’t fully understand how they differ or which one actually fits their situation. Each loan type comes with unique rules, costs, and long-term implications.

Comparing them side by side helps buyers avoid assumptions, reduce risk, and choose a mortgage that aligns with their finances rather than just meeting minimum requirements.

Conventional loans suit buyers with stronger credit, FHA loans help buyers with limited savings or credit, and VA loans offer exceptional benefits to eligible veterans. The best option depends on credit profile, savings, eligibility, and long-term plans.

Conventional Loans Favor Strong Credit and Long-Term Value

Conventional loans are not backed by the government and typically offer the lowest long-term costs for buyers with solid credit and stable income.

They often require higher credit scores than FHA loans but reward qualified buyers with lower mortgage insurance costs and more flexibility.

Buyers who already understand mortgage basics often prefer conventional loans because they’re easier to refinance later and don’t carry lifetime insurance requirements.

While down payments can be low, buyers with stronger financial profiles benefit most. Over time, conventional loans often provide better value and fewer restrictions.

FHA Loans Lower the Barrier to Entry

FHA loans are designed to help buyers who may not qualify for conventional financing due to limited credit history, lower scores, or smaller savings.

They allow more flexible qualification standards and lower down payment requirements.

However, FHA loans come with mortgage insurance that increases monthly costs and often lasts for the life of the loan.

Buyers comparing options should evaluate how FHA insurance affects monthly mortgage payments long term. FHA loans are excellent for getting into a home sooner but not always the cheapest option over time.

VA Loans Offer Unmatched Benefits for Eligible Buyers

VA loans are available only to eligible veterans, active-duty service members, and some surviving spouses.

These loans stand out because they often require no down payment and no monthly mortgage insurance. VA loans also feature competitive interest rates and flexible credit standards.

For eligible buyers, VA loans frequently outperform both conventional and FHA options.

Buyers who qualify should strongly consider VA loans, especially when comparing down payment options and long-term affordability. The main limitation is eligibility, not cost.

Down Payment Requirements Change Affordability

Down payments vary significantly across loan types. Conventional loans may allow low down payments but often require stronger credit.

FHA loans typically allow smaller down payments but increase monthly costs through insurance.

VA loans often eliminate the down payment entirely. Buyers evaluating how much house they can afford should consider how down payments affect both upfront cash and monthly obligations.

A lower down payment may preserve savings, but it can also increase long-term costs depending on loan type.

Mortgage Insurance Is a Key Differentiator

Mortgage insurance works very differently across these loans. Conventional loans allow insurance to be removed once equity builds.

FHA insurance usually stays for the life of the loan. VA loans generally don’t require monthly mortgage insurance at all.

Buyers who compare mortgage terms carefully see how insurance affects affordability years down the line. This difference alone can outweigh small rate advantages and significantly impact total cost.

Credit Score Expectations Vary by Loan Type

Conventional loans typically require higher credit scores but reward buyers with better pricing.

FHA loans accept lower scores but offset risk with insurance.

VA loans offer flexibility while still providing strong terms.

Buyers working on credit improvement benefit from knowing what credit score they need to buy before choosing a loan.

Selecting the wrong loan type based on assumptions can increase costs unnecessarily.

Interest Rates Don’t Tell the Full Story

Buyers often compare loans based only on interest rates, but rates don’t reflect total cost. Insurance, fees, and flexibility matter just as much.

Buyers who track mortgage rates today alongside loan structure make more informed comparisons.

A slightly higher rate with no mortgage insurance can cost less over time than a lower rate with permanent insurance.

Pre-Approval Clarifies Which Loan Fits You

Mortgage pre-approval shows which loan types you actually qualify for and what they cost in real terms.

Buyers familiar with mortgage pre-approval can compare conventional, FHA, and VA loans using actual numbers instead of estimates.

Pre-approval removes guesswork and helps buyers avoid chasing options they don’t qualify for.

Use Tools to Compare Loan Scenarios

Mortgage calculators help buyers compare payments, insurance costs, and long-term outcomes across loan types.

Using a mortgage calculator allows side-by-side comparisons that make differences obvious.

Buyers who test scenarios before committing feel more confident and avoid costly surprises later.

Conclusion

Conventional, FHA, and VA loans each serve different types of buyers. The right choice depends on credit strength, savings, eligibility, and long-term plans, not marketing or assumptions.

When buyers understand how each loan works and how costs add up over time, they choose mortgages that support stability instead of stress.

Reviewing the first-time home buyer guide and understanding home loans explained helps ensure your loan choice fits both today’s needs and tomorrow’s goals.

Frequently Asked Questions

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Next Read

Featured Mortgage Insights

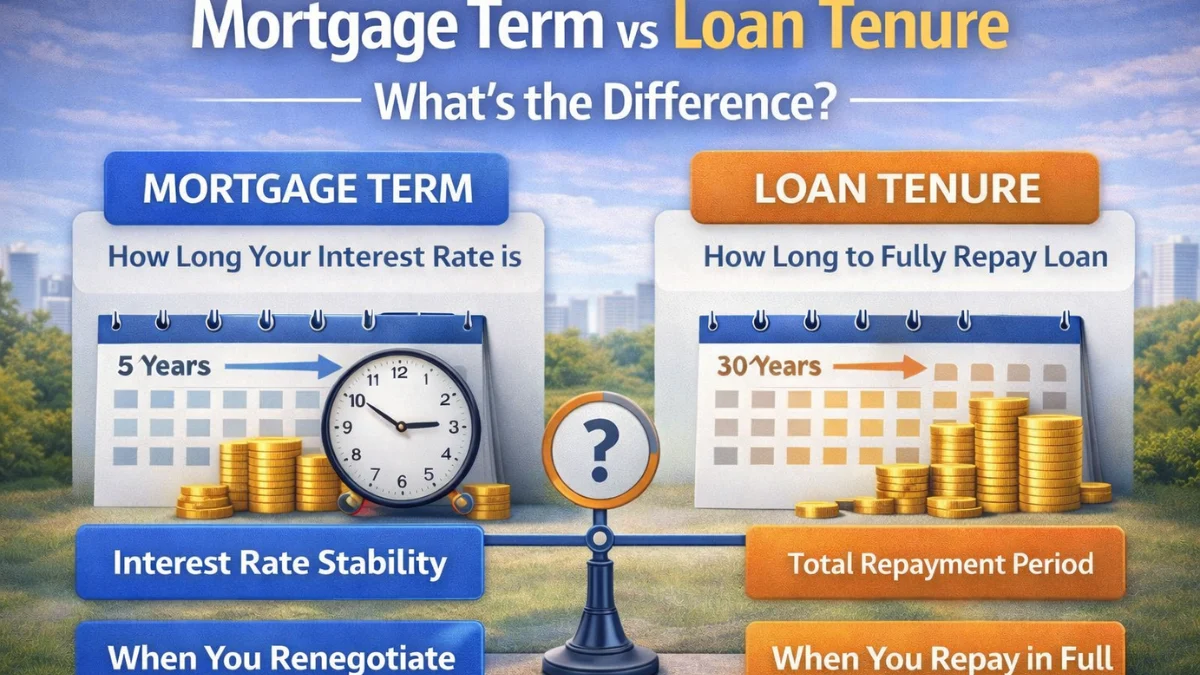

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.

About the Author: Ratiranjan Singha

Don’t Miss These