How Do Auto Loans Work? Everything You Need to Know Before You Apply

Auto loans make it possible to buy a car without paying the full price upfront, but many borrowers don’t fully understand how they actually work.

Knowing how auto loan payments, interest, and approval factors operate can help you avoid costly mistakes and make smarter financial decisions before applying.

How Auto Loans Work Step by Step

An auto loan works by allowing you to borrow money from a lender to purchase a vehicle, which you then repay in monthly installments over a fixed period.

First, you choose a car and decide your budget. Then, you apply for a loan, and the lender evaluates your creditworthiness.

Once approved, the lender pays the dealer, and you begin monthly payments that include principal and interest. The vehicle acts as collateral, meaning it can be repossessed if you default.

Before applying, it’s smart to estimate payments using an auto loan calculator to understand your financial commitment clearly.

Understanding Auto Loan Interest and Total Cost

Interest is the price you pay for borrowing money, and it significantly impacts the total cost of your auto loan.

Lenders assign interest rates based on your credit score, income, and risk profile. Even a small difference in interest rates can result in paying thousands more over time.

Auto loan interest is typically calculated on the remaining balance, so early payments reduce interest faster.

If you want to minimize costs, understanding how auto loan interest works helps you choose better loan terms, negotiate rates, and save money in the long run.

Loan Term Length and Monthly Payment Impact

The loan term is the length of time you have to repay the loan, usually ranging from 36 to 72 months.

Longer terms reduce monthly payments but increase total interest paid, while shorter terms cost more monthly but save money overall.

Many first-time borrowers focus only on affordability without considering long-term costs. Choosing the right term depends on your budget and financial goals.

Learning about auto loan term length options can help you balance monthly affordability with total cost and avoid paying more than necessary.

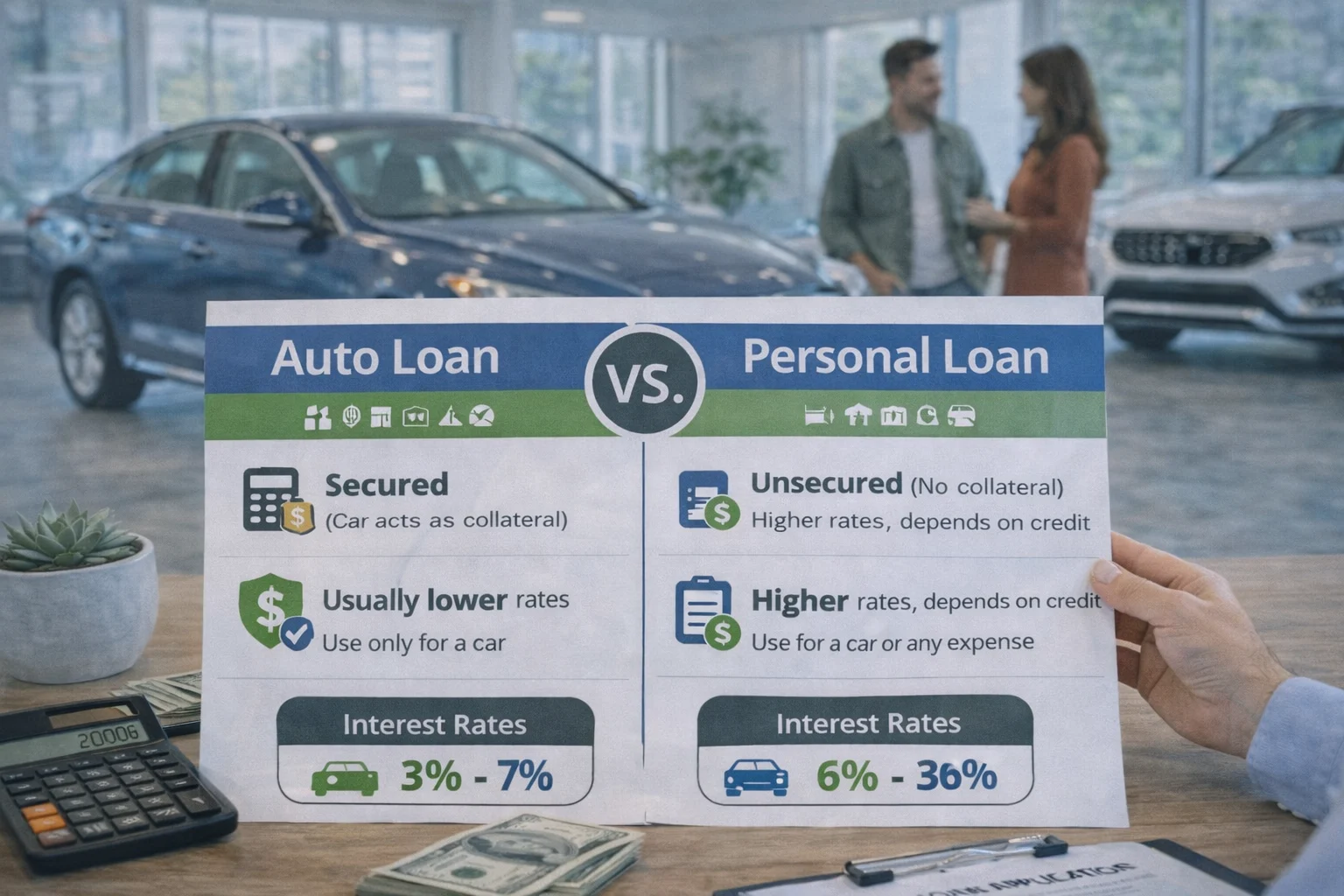

What Lenders Check Before Approving Your Auto Loan

Before approving your auto loan, lenders evaluate several factors to determine your risk level.

Your credit score is the most important, followed by your income, employment stability, and debt-to-income ratio.

A higher credit score typically results in better interest rates. Lenders may also consider your down payment and the value of the vehicle.

Preparing in advance by understanding auto loan approval factors can increase your chances of approval and help you secure better loan terms.

The Role of Down Payment in Auto Loans

A down payment is the amount you pay upfront when purchasing a car, and it directly affects your loan size and interest costs.

A higher down payment reduces the amount you need to borrow, which lowers your monthly payments and total interest.

It also improves your chances of approval and may qualify you for better interest rates. Many financial experts recommend putting down at least 10%–20% of the vehicle price.

Understanding auto loan down payment strategies helps you reduce financial risk and borrow more responsibly.

Pre-Approval vs Final Approval: What’s the Difference?

Pre-approval is when a lender evaluates your financial profile and gives you an estimate of how much you can borrow before you choose a car.

This helps you set a realistic budget and strengthens your negotiating power at dealerships.

Final approval happens after you select the vehicle and finalize loan details. Getting pre-approved can also help you compare lenders and interest rates.

Learning about auto loan pre-approval benefits ensures you enter the car-buying process with confidence and clarity.

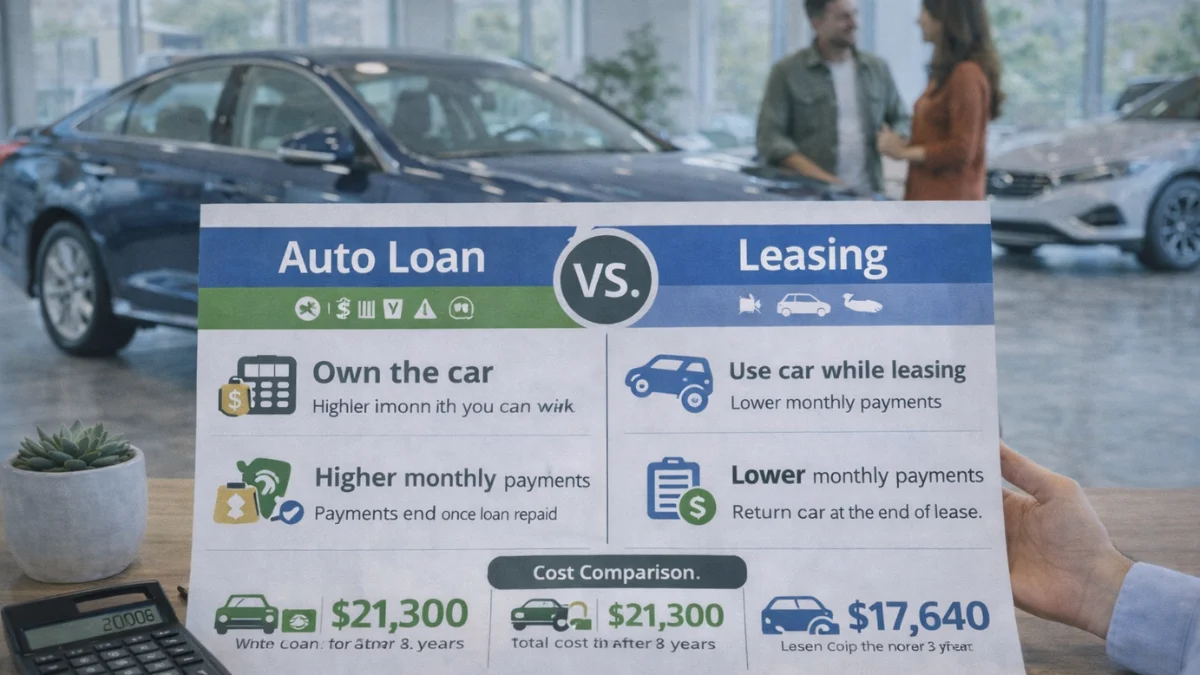

Auto Loan vs Leasing: How They Work Differently

Auto loans and leasing are two common ways to finance a vehicle, but they work very differently. With an auto loan, you eventually own the car after completing payments.

Leasing, however, allows you to use the car for a fixed period with lower monthly payments but no ownership. Leasing often comes with mileage limits and restrictions.

Choosing between the two depends on your financial goals and driving habits. Comparing auto loan vs leasing options can help you decide which approach suits your situation best.

Common Fees and Hidden Costs in Auto Loans

Many borrowers overlook additional costs that come with auto loans, such as origination fees, documentation fees, late payment penalties, and insurance requirements.

These hidden costs can significantly increase the total price of your loan.

Some lenders may also charge prepayment penalties if you pay off your loan early. Understanding these charges before signing any agreement is crucial.

Learning about auto loan hidden fees helps you avoid surprises and ensures you know the true cost of your loan.

What Happens If You Miss Payments or Default?

Missing auto loan payments can lead to serious consequences, including late fees, damage to your credit score, and potential repossession of your vehicle.

Lenders typically report missed payments to credit bureaus, which can affect your ability to borrow in the future.

If financial difficulties arise, it’s important to communicate with your lender early to explore options like deferment or restructuring.

Understanding auto loan default consequences helps you stay prepared and protect your financial health.

Can You Refinance Your Auto Loan Later?

Refinancing an auto loan means replacing your existing loan with a new one, usually to get a lower interest rate or better terms.

This can reduce your monthly payments or save you money over time.

Refinancing is especially useful if your credit score has improved or interest rates have dropped since you first took the loan.

However, it’s important to evaluate fees and loan terms carefully. Exploring auto loan refinancing options can help you decide if refinancing is the right financial move.

Frequently Asked Questions

Conclusion

Understanding how auto loans work is essential before applying, especially if you’re a first-time borrower.

From interest rates and loan terms to approval factors and hidden fees, every detail affects your financial outcome.

By using tools like an auto loan calculator, preparing your finances, and comparing options, you can make smarter decisions and avoid costly mistakes.

The more informed you are, the better your chances of securing a loan that fits your budget and long-term goals.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.