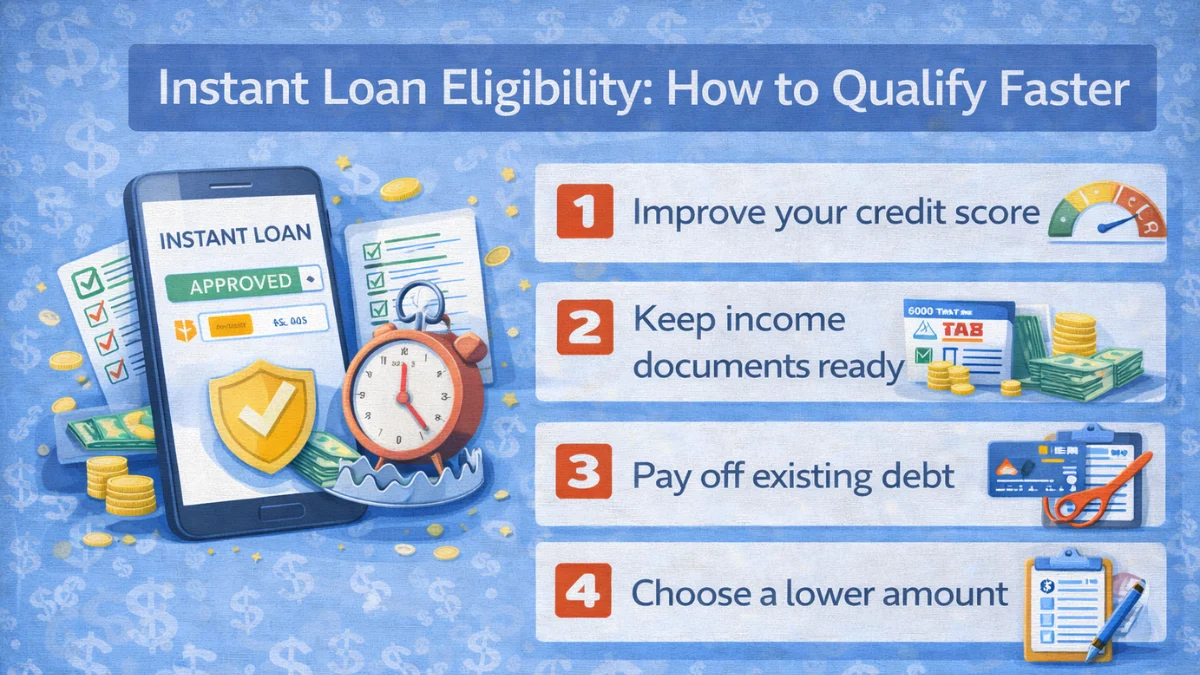

Loan-to-Value (LTV) Calculator (Check Your Mortgage Risk Level)

When it comes to mortgages, one of the most important numbers lenders look at is your loan-to-value ratio (LTV).

But many homeowners don’t fully understand what it means — or why it matters.

That’s where this LTV calculator helps.

It gives you a clear view of:

- your loan compared to your property value

- your equity position

- your financial risk level

If you’re new to mortgage basics, the home loans explained guide will help you understand how LTV fits into the bigger picture.

What is loan-to-value ratio (LTV)

Loan-to-value ratio (LTV) measures how much of your property is financed through a loan.

It is calculated as:

Loan amount ÷ property value × 100

For example:

- loan = $250,000

- property value = $400,000

LTV = 62.5%

The lower your LTV, the more equity you have in your property.

Why LTV matters

LTV plays a major role in your mortgage terms.

It affects:

- whether you need PMI

- your interest rate

- your refinancing eligibility

- your loan approval chances

Lenders use LTV to assess risk — the higher your LTV, the higher the risk.

If you’re close to 80% LTV, insights from when can first-time buyers stop paying pmi can help you understand when you can remove PMI.

How this LTV calculator works

This calculator uses two inputs:

- your loan amount

- your property value

It calculates:

- your LTV percentage

- your total equity

- your risk level

This gives you a quick snapshot of your financial position.

What is a good LTV ratio

Generally:

- below 80% – strong position (no PMI required)

- 80%–90% – moderate risk

- above 90% – higher risk

Reaching 80% LTV is a key milestone because it unlocks better loan terms and reduces costs.

If you want to see how equity impacts your finances, the home equity calculator provides deeper insights.

How to lower your LTV

You can reduce your LTV by:

- paying down your loan balance

- increasing your home value

- making extra principal payments

- refinancing your mortgage

Even small improvements in LTV can lead to better financial opportunities.

If you’re considering refinancing, reviewing refinance mortgage when does it actually make sense can help you decide the right timing.

How LTV affects refinancing

LTV is one of the biggest factors in refinancing.

Lower LTV means:

- better interest rates

- lower fees

- easier approval

Higher LTV can limit your options or increase costs.

To evaluate whether refinancing benefits you, use refinance decision calculator for a complete comparison.

Common mistakes to avoid

Many homeowners misunderstand LTV.

Avoid these mistakes:

- ignoring changes in home value

- focusing only on monthly payments

- not tracking LTV regularly

- assuming equity builds automatically

Tracking your LTV regularly helps you make smarter financial decisions.

Why this calculator matters

This tool helps you:

- understand your mortgage position

- track your equity growth

- plan refinancing or PMI removal

It turns a complex metric into something simple and actionable.

Final thoughts

Your LTV ratio is one of the most powerful indicators of your financial position as a homeowner.

The lower it gets, the more control and flexibility you gain.

By tracking your LTV, you can unlock better rates, lower costs, and smarter mortgage decisions.