Selling Your First Home: What First-Time Buyers Should Know Early

Most first-time buyers don’t think about selling when they’re focused on buying but they should. Decisions made at purchase..

Most first-time buyers don’t think about selling when they’re focused on buying but they should.

Decisions made at purchase time directly affect how easy, profitable, or stressful it will be to sell later.

From loan terms and closing costs to equity timelines and market conditions, selling a first home isn’t automatic or guaranteed to be profitable.

Understanding the selling side early helps buyers avoid short-term mistakes and make smarter long-term ownership decisions.

First-time buyers should understand that selling a home takes time, costs money, and depends heavily on how long they own it. Short ownership periods often lead to losses after fees, taxes, and market changes.

How Long You Need to Own Before Selling

One of the biggest surprises for first-time buyers is how long it takes for ownership to become financially worthwhile.

In the first few years, most of your payment goes toward interest, not equity.

Selling too soon often means losing money after agent commissions and closing costs.

Buyers who understand how buying a home really works are better prepared to commit for the time needed to build meaningful equity.

Selling Costs Most Buyers Forget

Selling isn’t free. Agent commissions, repairs, staging, concessions, and seller closing costs can easily reach 8-10% of the home’s value.

Many first-time buyers assume appreciation will cover these expenses, which isn’t always true.

Understanding hidden home buying costs early also prepares buyers for hidden selling costs later, helping them avoid unpleasant surprises when it’s time to list.

Market Conditions Matter More Than You Think

Housing markets change. Interest rates, buyer demand, and local inventory all affect how quickly a home sells and at what price. Even good homes can sit longer during slow markets.

Buyers who follow what causes mortgage rates to go up or down gain insight into how broader economic shifts influence future resale demand and pricing power.

How Your Mortgage Affects Selling

Loan type, interest rate, and remaining balance all impact selling flexibility. Buyers who stretch their budget or choose risky loan structures may find it harder to sell without bringing cash to closing.

Understanding mortgage terms first-time buyers should never ignore helps buyers choose financing that supports both ownership and resale.

Equity Isn’t Guaranteed

Home values don’t rise evenly or predictably. Neighborhood changes, local taxes, and maintenance neglect can limit appreciation.

Equity grows slowly at first, making early resale risky.

Buyers who evaluate is homeownership still worth it long-term are more realistic about when selling makes financial sense versus when renting or holding longer is smarter.

Planning for Life Changes

Job moves, family changes, or financial shifts often trigger first-home sales earlier than planned.

Buyers who assume they’ll stay forever may feel stuck later.

Considering does renting or buying make sense helps buyers assess flexibility needs before committing to ownership.

Frequently Asked Questions

Conclusion

Selling your first home is easier and more profitable when you plan for it early.

First-time buyers who understand timelines, costs, and market risks make smarter buying decisions upfront and avoid financial stress later.

Thinking ahead doesn’t reduce excitement; it protects your future options and financial stability.

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Next Read

Featured Mortgage Insights

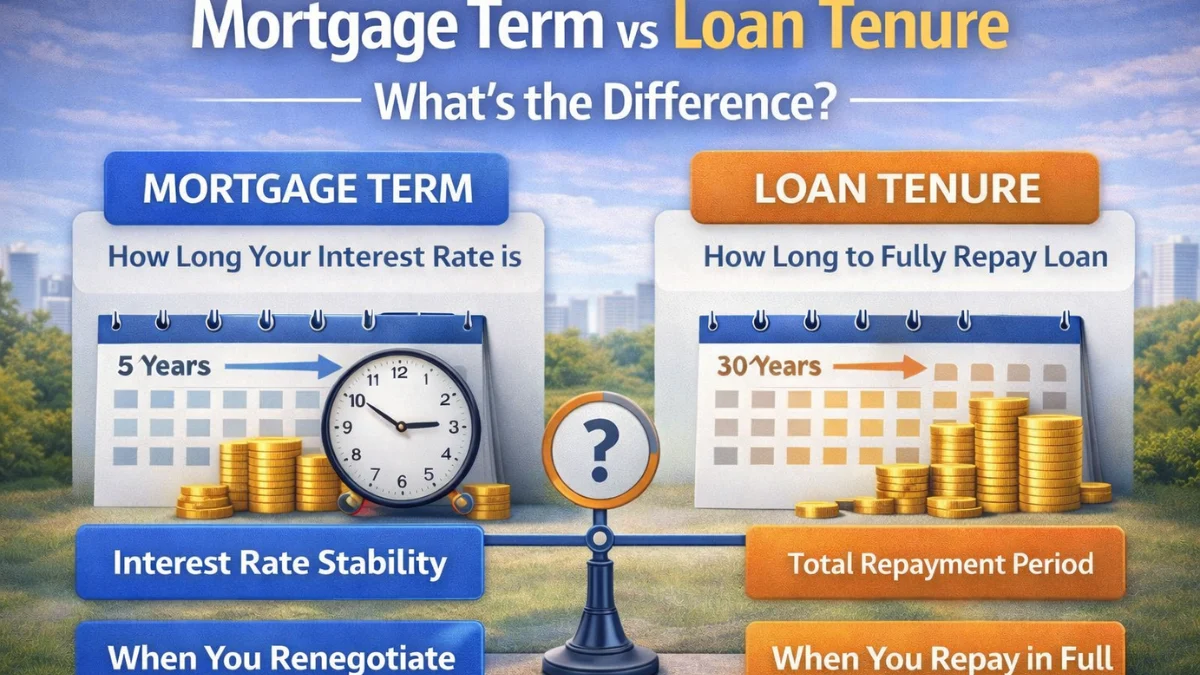

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.

About the Author: Ratiranjan Singha

Don’t Miss These