Refinancing Your Mortgage: Rates, Costs & Smart Tips

Refinancing your mortgage is one of the most powerful financial decisions a homeowner can make but it’s also one of the..

Refinancing your mortgage is one of the most powerful financial decisions a homeowner can make but it’s also one of the most misunderstood.

Many people focus only on chasing a lower interest rate, without fully understanding how refinancing affects total loan cost, monthly cash flow, equity, risk exposure, and long-term financial stability.

This guide is designed to give you a complete, understanding of mortgage refinancing, from how rates really work to when refinancing makes sense, how much it costs, and which loan options fit different life situations.

Whether you’re a first-time refinancer or a seasoned homeowner, this page will help you make smarter, safer decisions. For up-to-date tools and rate tracking, you can always start at the mortgage rates checker homepage.

What Does It Mean to Refinance a Mortgage?

Refinancing means replacing your existing home loan with a new one, usually with different terms. The new loan pays off the old mortgage, and you begin making payments on the new loan instead.

Homeowners refinance for several core reasons:

- Lower the interest rate

- Reduce monthly payments

- Shorten or extend the loan term

- Switch from adjustable to fixed rates

- Access home equity as cash

- Consolidate high-interest debt

However, refinancing is not automatically beneficial. The value depends on timing, loan structure, closing costs, and how long you plan to keep the home.

How Refinance Mortgage Rates Really Work?

Mortgage refinance rates are influenced by far more than just “market rates.” Lenders price refinance loans based on:

- Treasury yields and mortgage-backed securities

- Inflation expectations

- Federal Reserve policy (indirectly)

- Borrower credit score

- Loan-to-value (LTV) ratio

- Property type and occupancy

- Loan size and term length

To compare options properly, start with refinance mortgage rates comparison, then review current refinance rates to understand today’s environment.

If you want a deeper explanation, how refinance rates work breaks down what lenders actually factor into pricing.

Many homeowners focus only on advertised offers, but the most accurate picture comes from tracking best refinance rates right now and verifying whether those offers apply to your credit profile.

Historical perspective also matters, rates today vs last year explains why some refinancing windows are far more valuable than others.

When Refinancing Makes Sense ?

Refinancing only makes financial sense when the long-term savings outweigh the costs. This is why understanding break-even points is critical.

Refinancing usually makes sense when:

- You can lower your rate meaningfully

- You plan to stay in the home past the break-even period

- You improve loan stability (ARM - fixed)

- You reduce total interest paid

- You use equity strategically, not emotionally

It may not make sense if:

- Closing costs erase the savings

- You reset the loan term unnecessarily

- You plan to sell soon

- You increase risk for short-term cash

Before moving forward, review when refinancing makes sense and ask yourself should I refinance now based on your financial goals, not just rates.

The Refinancing Process (Step-by-Step)

Refinancing follows a structured process similar to getting a new mortgage:

- Evaluate your goals and current loan

- Check credit and equity position

- Compare loan offers and rates

- Submit documentation

- Lock your rate

- Close the loan

- Begin new payments

Following how to refinance smartly helps avoid common mistakes, while the step-by-step refinance guide explains each stage in detail. Many homeowners are surprised by escrow changes, payment timing, and lender communications - what happens after refinancing covers these adjustments clearly.

Choosing the Right Loan Term: 30-Year vs 15-Year

Loan term selection affects both affordability and lifetime interest costs.

30-Year Refinance Loans

A 30-year refinance offers lower monthly payments and flexibility. It’s ideal for homeowners prioritizing cash flow or long-term stability.

Explore 30-year refinance rates, compare lenders using 30-year rate comparisons, and understand norms through average 30-year mortgage rates and rate trends over time.

15-Year Refinance Loans

A 15-year refinance dramatically reduces interest paid but increases monthly payments. If income is stable and retirement planning is a priority, comparing 15-year mortgage rates today, 15-year vs 30-year rates, and 15-year refinance comparisons can clarify whether switching to 15-year is worth it.

Government Refinance Programs: VA and FHA

VA Refinancing for Veterans

VA loans offer some of the most borrower-friendly refinancing options. Start with VA refinance basics and compare VA refinance rates today.

The VA IRRRL (streamline refinance) allows eligible borrowers to refinance with minimal documentation, details are covered in VA IRRRL explained, with pricing insights in IRRRL rates today and cost-benefit analysis in IRRRL worth it.

Veterans seeking equity access should carefully review VA cash-out refinance pros and cons and compare VA cash-out rates, while eligibility is explained in VA refinance eligibility.

FHA Refinancing Options

FHA borrowers can benefit from flexible credit requirements and streamline programs. The FHA refinance guide and FHA refinance rates today explain current options.

For minimal paperwork, FHA streamline refinance and FHA streamline rates are worth exploring. Equity-based refinancing rules are detailed in FHA cash-out rules and FHA cash-out rate comparisons.

Many homeowners also consider transitioning, FHA to conventional refinance explains when that move makes sense.

Cash-Out Refinancing and Home Equity Use

Cash-out refinancing allows homeowners to convert equity into usable funds, but it increases loan balance and risk.

Before proceeding, understand cash-out refinance basics, review cash-out rates today, and compare cash-out vs standard refinance rates. The trade-offs are clearly outlined in cash-out refinance pros and cons.

Special scenarios include cash-out on rental property, cash-out for investments, and cash-out on a paid-off home. If you’re unsure whether refinancing is the best equity tool, home equity refinance vs cash-out and HELOC vs refinance provide clarity.

Jumbo and Conventional Refinancing

High-balance borrowers should analyze jumbo refinance rates, compare jumbo mortgage refinance options, and monitor jumbo loan rates today. Long-term jumbo planning is covered in 30-year jumbo refinance rates.

For standard loans, conventional refinance rates today and conventional refinance eligibility explain qualification and pricing differences.

Refinance Costs, Fees, and Real Savings

Refinancing is not free. Typical costs include lender fees, appraisal, title insurance, and prepaid items.

Start with refinance closing costs, then review refinance fees to avoid and get a full picture from cost to refinance a house. Market benchmarks are explained in average refinance closing costs.

To calculate whether refinancing actually saves money, use refinance savings calculator and validate estimates through refinance estimate accuracy.

Strategic Reasons to Refinance

Homeowners refinance for more than rates:

- Refinance to pay off debt or refinance house for debt payoff

- Refinance for home improvements

- Refinance to lower rate

- No-closing-cost refinance

- Rate-and-term refinance

- ARM to fixed refinance timing

Each strategy carries different risks and benefits depending on income stability and long-term plans.

Refinancing vs Other Loan Options

Sometimes refinancing isn’t the best choice. Comparing refinance vs home equity loan, refinance vs HELOC, and second mortgage vs refinance can reveal lower-risk alternatives. Pricing differences are covered in second mortgage rates explained.

Mortgage Calculators and Decision Tools

Accurate calculations are essential. Start with the refinance calculator, then explore tools like mortgage payment calculator, amortization calculator, and mortgage rate calculator.

Specialized tools include VA loan calculator, VA closing cost calculator, USDA payment calculator, and mortgage affordability calculator. Advanced planning tools include extra payment calculator and PMI calculator.

Learning Resources for Buyers and Homeowners

If you’re early in your journey, the first-time home buyer guide explains foundational concepts. Ongoing education is available through the mortgage blog, while common questions are answered in the mortgage help FAQs.

Conclusion

Refinancing is not about chasing the lowest rate, it’s about aligning your mortgage with your financial life. The smartest refinances consider cost, timing, loan structure, risk, and long-term goals together.

When done correctly, refinancing can improve cash flow, reduce lifetime interest, and strengthen financial security. When done blindly, it can delay wealth-building and increase risk.

Use this guide as your foundation and make every refinance decision with clarity, not pressure.

Frequently Asked Questions

Refinance means replacing your current home loan with a new one, usually to get a lower interest rate, change the loan term, switch from ARM to fixed, or access home equity through cash-out refinancing.

A good time to refinance is when today’s refinance rates are lower than your current rate, your home value has increased, or your credit score has improved enough to qualify for better terms.

Refinance rates are often slightly higher than purchase rates, but they closely follow today’s 30-year fixed mortgage rates and 15-year refinance rates, depending on loan type and borrower profile.

Refinance closing costs typically range from 2% to 5% of the loan amount. These may include lender fees, appraisal costs, title fees, and prepaid items, though some lenders offer no-closing-cost refinance options.

Yes, many homeowners can refinance after forbearance, including FHA streamline refinance or conventional options, as long as payment history and eligibility guidelines are met.

A rate-and-term refinance changes your interest rate or loan length, while a cash-out refinance lets you borrow against home equity to receive cash, often used for debt consolidation or major expenses.

Yes. If your home value has gone up, refinancing may help you qualify for better refinance mortgage rates, remove PMI, or access equity through a cash-out refinance.

Some homeowners can refinance immediately after closing, but most loan programs require a seasoning period (often 6–12 months), especially for cash-out refinance loans.

Refinancing to a 15-year mortgage usually means higher monthly payments but lower total interest, while a 30-year refinance offers lower monthly payments and more flexibility.

You can estimate your new payment, interest savings, and break-even point using a mortgage refinance calculator, which factors in current refinance rates, loan balance, term, and closing costs.

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Related Posts

Featured Mortgage Insights

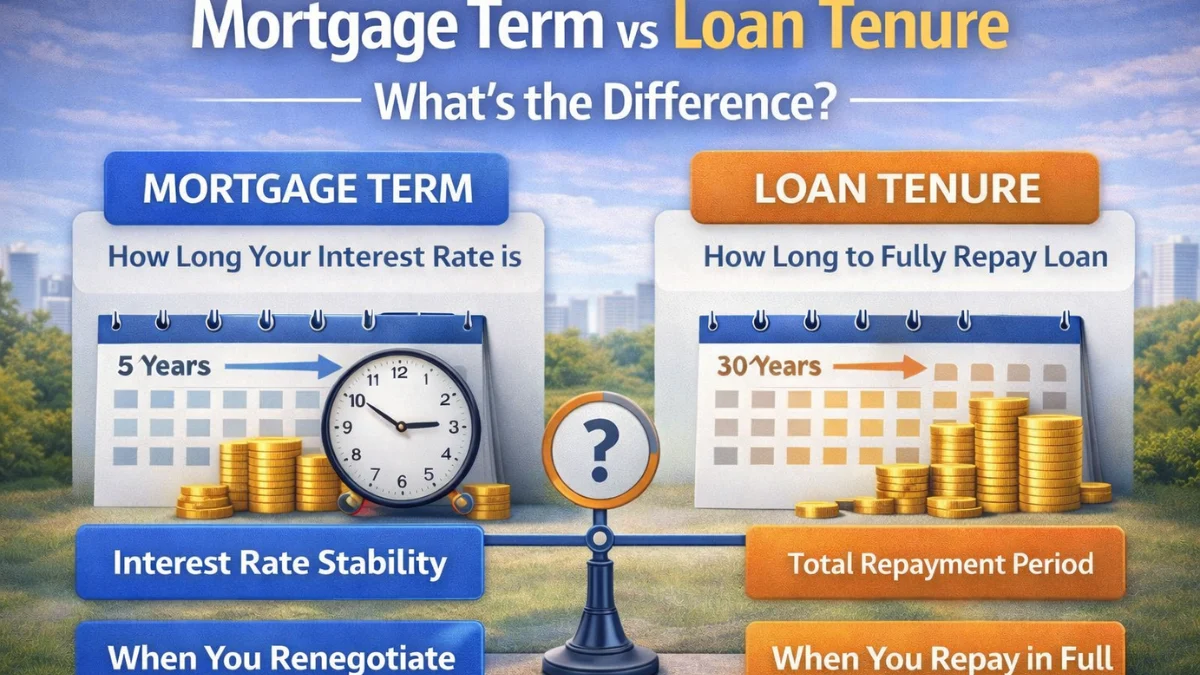

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.