What Is an Auto Loan? A Simple Guide for First-Time Borrowers

An auto loan helps you finance a car without paying the full price upfront.

Whether you’re buying your first vehicle or upgrading, understanding how auto loans work can save you money, reduce stress, and help you avoid costly mistakes when borrowing.

What Is an Auto Loan and How Does It Work?

An auto loan is a type of financing that allows you to purchase a vehicle by borrowing money from a lender and repaying it over time with interest.

Instead of paying the full car price upfront, you make fixed monthly payments based on the loan amount, interest rate, and loan term.

The car itself usually acts as collateral, meaning the lender can repossess it if you fail to repay.

Before applying, it’s important to understand how your payments are structured using an auto loan calculator so you can plan your budget effectively and avoid overpaying.

Key Components of an Auto Loan You Must Understand

Every auto loan includes several important elements that directly impact how much you pay over time. The loan amount is the total money borrowed after your down payment.

The interest rate determines the cost of borrowing, while the loan term (such as 36, 60, or 72 months) affects your monthly payment and total interest. Your credit score, income, and debt also influence approval and rates.

If you’re new to borrowing, learning about auto loan approval factors can help you understand what lenders evaluate and how to improve your chances before applying.

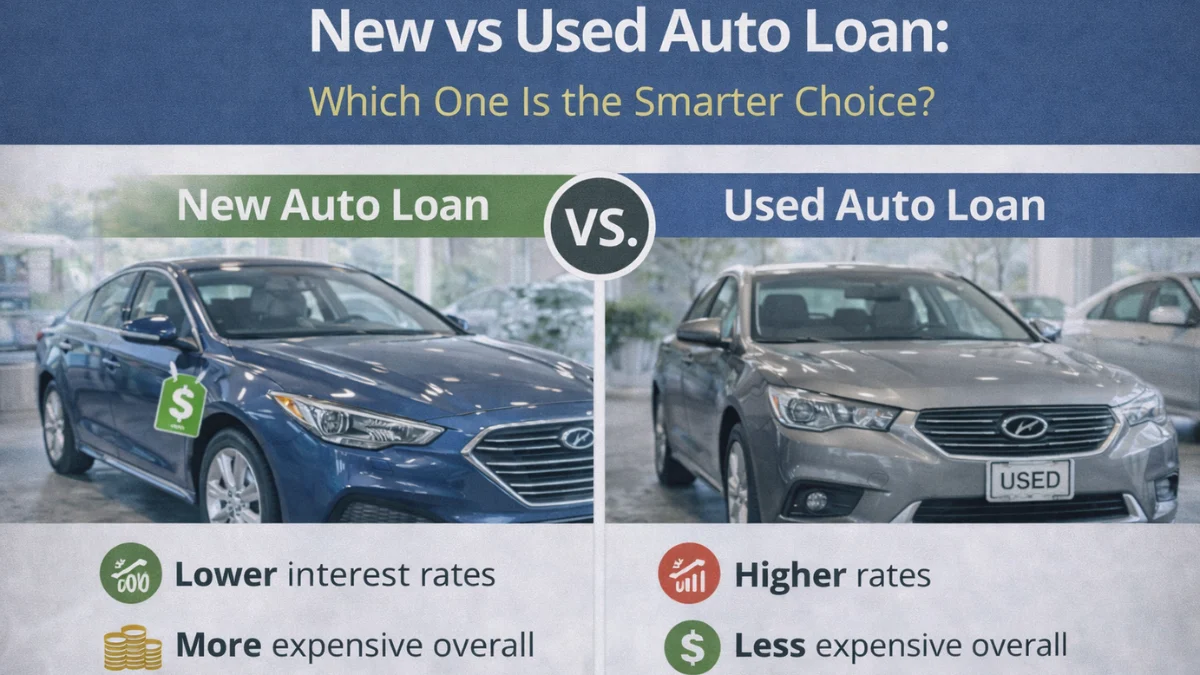

Types of Auto Loans: New vs Used Car Financing

Auto loans are generally divided into new car loans and used car loans, each with different interest rates and conditions.

New car loans often come with lower interest rates because the vehicle has higher value and less risk for lenders.

Used car loans may have slightly higher rates but lower purchase prices. Choosing between them depends on your budget, financial goals, and long-term plans.

If you’re unsure which option suits you better, understanding new vs used auto loan options can help you make a smarter financial decision.

How Auto Loan Interest Works (And Why It Matters)

Interest is the cost you pay for borrowing money, and it plays a major role in your total loan cost.

Even a small difference in interest rates can significantly impact how much you pay over time. Auto loan interest is typically calculated on the remaining loan balance, meaning early payments reduce more interest.

To save money, borrowers should focus on securing lower rates, making larger down payments, or choosing shorter loan terms.

Learning how auto loan interest works can help you reduce overall borrowing costs and avoid paying thousands more than necessary.

How Monthly Payments Are Calculated

Your monthly auto loan payment depends on three main factors: loan amount, interest rate, and loan term.

Longer terms reduce monthly payments but increase total interest, while shorter terms cost more monthly but save money overall.

Lenders also include taxes, fees, and insurance in some cases.

Before committing, it’s smart to estimate payments using an auto loan monthly payment guide so you clearly understand affordability and avoid financial strain after purchase.

What Affects Your Auto Loan Approval?

Lenders evaluate several factors before approving your auto loan application. Your credit score is one of the most important, as it determines your risk level and interest rate.

Income stability, employment history, and existing debts also play a significant role. A higher down payment can improve your chances and reduce borrowing costs.

If you want faster approval, understanding how to get auto loan approval fast can help you prepare documents, improve your credit profile, and avoid unnecessary delays.

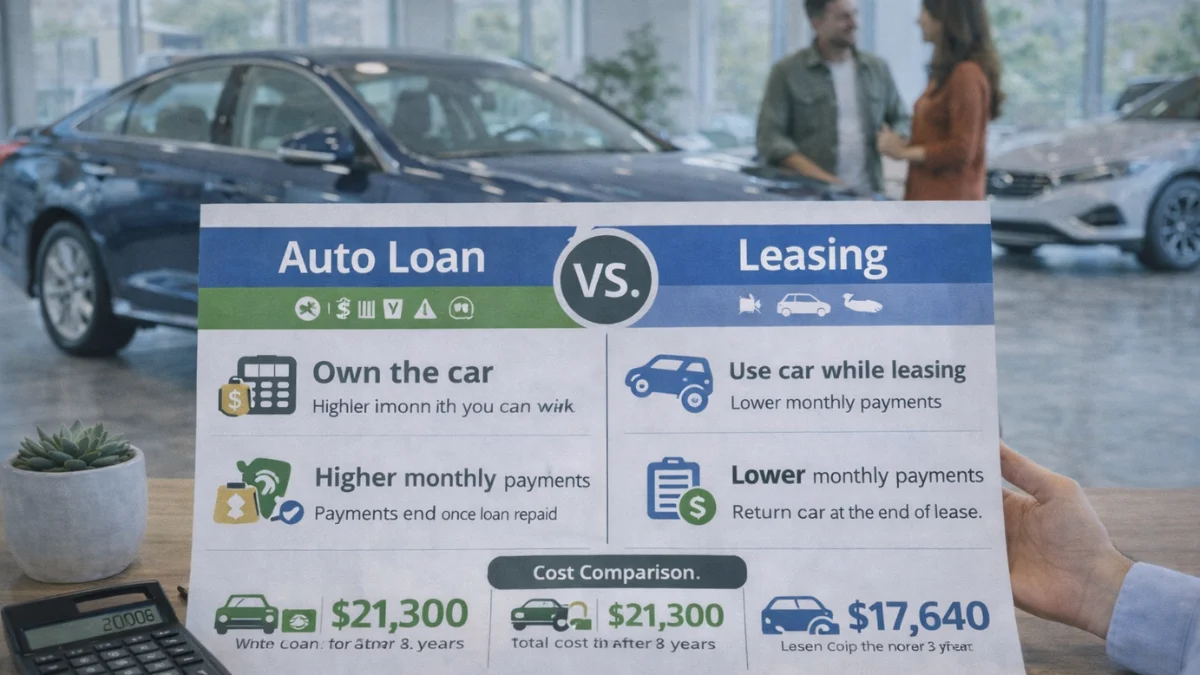

Auto Loan vs Leasing: Which Is Better for You?

Many first-time buyers struggle to decide between financing and leasing a car. With an auto loan, you own the vehicle after completing payments, giving you long-term value.

Leasing, on the other hand, offers lower monthly payments but no ownership at the end.

The right choice depends on how long you plan to keep the car and your financial situation.

Comparing auto loan vs leasing options can help you determine which approach aligns better with your lifestyle and budget.

Common Auto Loan Mistakes First-Time Borrowers Make

Many borrowers make costly mistakes when taking an auto loan, such as focusing only on monthly payments instead of total cost, choosing long loan terms, or ignoring hidden fees.

Others fail to compare lenders or apply without checking their credit score. These mistakes can lead to higher interest rates and financial stress.

Understanding auto loan mistakes to avoid helps you make smarter decisions, negotiate better terms, and save money over the life of the loan.

What Happens If You Miss an Auto Loan Payment?

Missing an auto loan payment can have serious consequences, including late fees, credit score damage, and even vehicle repossession.

Lenders may report missed payments to credit bureaus, making future borrowing more difficult.

If you’re struggling financially, it’s important to contact your lender early to explore options like deferment or restructuring.

Knowing the risks of auto loan default consequences helps you stay prepared and protect your financial stability.

Can You Refinance an Auto Loan Later?

Yes, refinancing allows you to replace your current auto loan with a new one, usually at a lower interest rate or better terms.

This can reduce your monthly payments or total interest cost. Refinancing is especially beneficial if your credit score has improved or market rates have dropped.

However, it’s important to evaluate fees and loan duration before proceeding.

Learning about auto loan refinancing options can help you decide whether refinancing is the right move for your situation.

Frequently Asked Questions

Conclusion

An auto loan is one of the most common ways to finance a vehicle, but understanding how it works is essential before committing.

From interest rates and loan terms to approval factors and hidden costs, every detail impacts your financial outcome.

By using tools like an auto loan calculator, comparing options, and avoiding common mistakes, you can make smarter borrowing decisions.

Whether you’re buying your first car or upgrading, the right knowledge helps you save money and stay in control of your finances.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.