Average Mortgage Length (2026): How Long Loans Really Last

If you’ve ever wondered how long a mortgage really lasts, you’re not alone. Many people assume they’ll be paying for 30..

If you’ve ever wondered how long a mortgage really lasts, you’re not alone.

Many people assume they’ll be paying for 30 years, but the reality is very different.

Mortgage length affects your monthly payments, total interest, and long-term financial flexibility.

Understanding how loan terms actually work can help you make smarter decisions, whether you’re buying your first home or considering refinancing options in today’s changing market.

Mortgage Calculator

Results

Extra Payment Impact

WHAT IS A MORTGAGE LENGTH?

A mortgage length, also known as the loan term, is the number of years you agree to repay your home loan.

Most common terms include 30, 20, and 15 years, with payments divided into monthly installments. For example, a 30-year mortgage equals 360 payments.

Understanding this structure is essential before choosing a loan, especially if you’re just starting with mortgages through a first-time buyer guide or learning from mortgage basics explained simply.

The term you choose directly impacts both affordability and total interest paid.

AVERAGE MORTGAGE LENGTH IN 2026

The average mortgage length in 2026 is still 30 years, but that doesn’t reflect real borrower behavior.

Most homeowners keep their mortgage for about 10 to 12 years before refinancing or selling.

This difference is critical because it changes how you should think about loan planning.

Many borrowers refinance to lower payments using strategies explained in refinance mortgage rates compare options or adjust their loan duration based on market trends.

Understanding both the official term and real holding period gives you a more realistic financial picture.

MOST COMMON MORTGAGE TERMS

Mortgage terms vary, but three options dominate the market: 30-year, 15-year, and 20-year loans.

A 30-year mortgage offers lower monthly payments but higher lifetime interest. A 15-year loan reduces interest significantly but increases monthly costs. The 20-year option sits in between.

Many borrowers compare these options using tools like a mortgage calculator or explore detailed rate differences in current 30-year mortgage rates explained and 15-year mortgage rates today explained.

Choosing the right term depends on your income, goals, and risk tolerance.

30-YEAR VS 15-YEAR MORTGAGE

The biggest difference between 30-year and 15-year mortgages is cost versus affordability.

A 30-year loan lowers monthly payments, making it easier to qualify, but results in much higher total interest.

A 15-year loan builds equity faster and saves thousands in interest, but requires higher monthly payments.

Many homeowners analyze this trade-off using current 15-year mortgage rates vs 30-year rates and compare long-term savings.

The right choice depends on whether you prioritize monthly cash flow or long-term financial efficiency.

WHY MOST PEOPLE DON’T KEEP 30-YEAR MORTGAGES

Although 30-year mortgages are standard, most borrowers never reach the end of the term.

Life changes like job relocation, family growth, or upgrading homes often lead to selling earlier.

Additionally, refinancing plays a huge role. Homeowners frequently adjust their loans using strategies from how to refinance your mortgage smartly or evaluate timing through should I refinance my mortgage right now.

Market conditions, interest rate changes, and financial goals all contribute to shorter actual mortgage durations than originally planned.

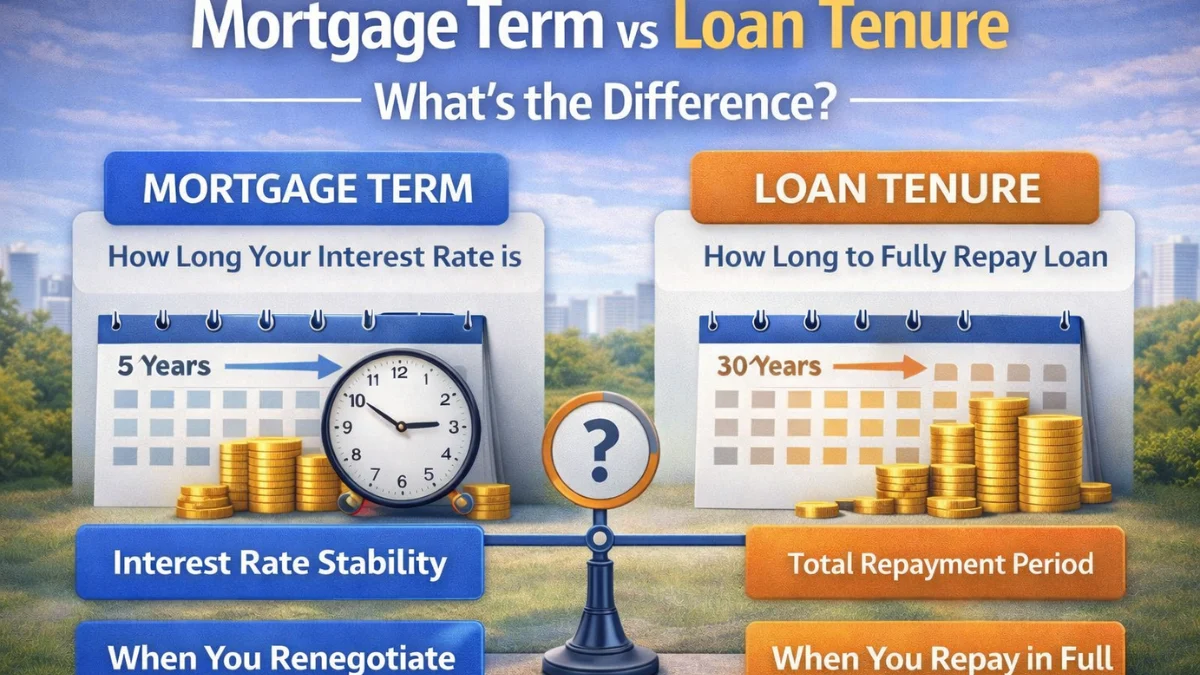

MORTGAGE LENGTH VS LOAN TENURE

Mortgage length and loan tenure are often used interchangeably, but they can have slight differences depending on region.

In the U.S., both typically refer to the repayment period of a home loan.

However, globally, tenure may sometimes include flexible repayment structures.

Understanding this distinction is important when comparing international mortgage systems.

If you’re learning fundamentals, reviewing home loans explained simply can help clarify these terms and avoid confusion when analyzing loan offers or comparing financial products.

HOW MORTGAGE LENGTH AFFECTS YOUR MONEY

Mortgage length directly impacts your financial future in three key ways: monthly payment, total interest, and equity growth.

Longer terms reduce monthly payments but increase interest paid over time.

Shorter terms increase payments but help you build equity faster and save money overall.

Many homeowners use tools like a mortgage payment calculator or explore savings through calculating mortgage refinance savings to understand these trade-offs.

Choosing the right term is not just about affordability, it’s about long-term financial strategy.

WHAT MORTGAGE LENGTH SHOULD YOU CHOOSE

Choosing the right mortgage length depends on your financial situation and future plans. A 30-year loan is ideal if you want lower monthly payments and flexibility.

A 15-year loan is better if you want to minimize interest and pay off your home faster. If you expect to move or refinance, a longer term may make more sense.

Many borrowers evaluate options using mortgage refinance options explained and consider future rate trends before deciding. The best choice balances comfort, savings, and long-term goals.

AVERAGE MORTGAGE LENGTH BY COUNTRY

Mortgage lengths vary globally. In the U.S., 30-year loans dominate, while in the UK, typical terms are closer to 25 years. Canada often uses shorter fixed-rate periods with renewals.

These differences reflect economic conditions and lending systems.

If you’re comparing global housing trends or planning international property investments, understanding these variations is important.

It also highlights why U.S. borrowers rely heavily on refinancing strategies like those discussed in refinance interest rates how they work to adjust loan terms over time.

FUTURE TRENDS IN MORTGAGE LENGTH

Looking ahead, mortgage trends are evolving due to rising interest rates and affordability challenges.

More borrowers are considering shorter terms to reduce interest costs, while others prefer longer loans for flexibility.

Refinancing will continue to play a major role in how long mortgages actually last.

Tools like a refinance readiness checker and insights from mortgage rates today can help homeowners adapt to changing conditions.

Understanding these trends can help you plan smarter and avoid costly long-term mistakes.

Related Mortgage Guides to Understand Loan Length Better

Understanding mortgage length goes beyond just choosing a 30-year or 15-year loan. Several factors like loan structure, borrower behavior, and global mortgage systems can influence how long you actually stay in a mortgage.

If you want a deeper understanding, explore these detailed guides:

- mortgage length by country to compare how loan terms differ across the US, UK, Canada, and Australia.

- mortgage length for first-time buyers to see what new homeowners typically choose and why.

- short vs long mortgage comparison to understand which option fits your financial goals better.

- mortgage term vs loan tenure to learn the key differences that many borrowers misunderstand.

- why most people don’t keep 30-year mortgages and what it means for your loan strategy.

These guides will help you make smarter decisions based on your financial situation, long-term plans, and how mortgages actually work in real life.

Frequently Asked Questions

Conclusion

The average mortgage length may be 30 years, but the reality is far more dynamic.

Most homeowners adjust their loans long before that through refinancing, selling, or changing financial priorities.

Understanding this difference helps you make smarter decisions about loan terms, monthly payments, and long-term costs.

Whether you’re buying your first home or planning to refinance, choosing the right mortgage length can significantly impact your financial future.

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Related Posts

Featured Mortgage Insights

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.