Current 30 Year Mortgage Rates Explained

Understanding current 30-year mortgage rates helps homeowners whether buying a home or considering a refinance make smarter financial decisions...

Understanding current 30-year mortgage rates helps homeowners whether buying a home or considering a refinance make smarter financial decisions.

Unlike short-term loan structures or adjustable options, a 30-year fixed mortgage rate generally stays the same for the life of the loan, providing predictable payments and long-term budgeting security.

But what exactly influences these rates today, and how should you interpret the numbers you see?

This guide explains how current 30-year mortgage rates work and what factors matter most when you’re thinking about refinancing or buying.

What “Current 30 Year Mortgage Rates” Means

When you see a published “current 30-year mortgage rate,” it’s usually a national average for conventional fixed-rate loans reported by financial institutions or data aggregators.

These averages provide a snapshot of the broader lending environment but don’t account for borrower-specific details like credit score, debt levels, or loan-to-value ratio.

They’re most useful as a directional benchmark for evaluating whether today’s environment is generally favorable for borrowing or refinancing.

How Market Forces Influence Current Rates

Current 30-year mortgage rates primarily move with broader economic signals, especially long-term Treasury yields, inflation expectations, and monetary policy.

When economic growth is strong and inflation rises, mortgage rates tend to increase. When markets expect slower growth or lower inflation, rates usually fall.

This dynamic is why current rates can change daily, they respond to a complex mix of investor behavior and macroeconomic indicators.

Why Your Actual Rate Can Differ From Averages

National averages are a starting point, but your actual 30-year rate is personalized. Lenders adjust pricing based on:

- Credit score and credit history

- Loan-to-value (equity) ratio

- Debt-to-income ratio

- Loan type (conventional, FHA, VA, etc.)

This is why reviewing what lenders look at for refinance approval helps you understand why two homeowners with similar goals may receive different refinance rates.

Current 30-Year Mortgage Rates and Refinance Decisions

If you’re considering refinancing, current 30-year mortgage rates are only part of the picture. You should also compare how today’s rates relate to:

- Your current mortgage interest rate

- Closing costs and fees

- Your planned timeline in the home

- Total interest vs monthly payment savings

Using tools like a refinance calculator helps translate a given rate into real dollars saved, not just advertised percentages.

Current Rates vs Other Loan Structures

Compared with shorter terms (like 15-year fixed), current 30-year mortgage rates are typically higher because lenders assume more risk over a longer timeline.

Adjustable rate mortgages (ARM) may start with a lower initial rate, but they carry uncertainty after the fixed period ends.

When you explore mortgage refinance options, knowing current 30-year rate pricing helps you position it against other structures in a way that supports your overall goals.

How Credit and Equity Affect Your Personalized Rate

While national averages guide expectations, your rate depends heavily on personal factors:

- Higher credit scores usually qualify for lower rates.

- Greater home equity (lower loan-to-value) often unlocks better pricing.

- Stable income and low debt reduce lender risk and can improve your offer.

Understanding these influences helps you see why the “current rate” you’re quoted may not match the published average.

Rate Lock Timing and Current Rates

Because mortgage rates can move between your initial quote and closing, lenders allow you to lock your rate once you are ready to proceed.

Lock duration (30, 45, 60 days, etc.) affects pricing, so understanding how mortgage rates work helps you choose the right timing for locking based on current rate trends.

When Current 30-Year Rates Make Refinancing Attractive

Current 30-year mortgage rates often present a refinancing opportunity when:

- They’re meaningfully lower than your existing mortgage rate

- Expected savings outweigh closing costs

- You plan to stay in the home beyond the break-even point

- You prefer long-term stability right away

Seeing how current rates compare with your own situation helps you decide whether refinancing now improves your financial pictur

Common Misconceptions About Current Rates

- “Lowest rates ever” doesn’t always mean lowest for you – personal factors matter.

- Short-term rate drops may not translate into long-term advantage if other costs are high.

- All lenders see the same rates is false – quotes vary with lender pricing models and borrower profiles.

Understanding these realities helps you interpret current 30-year mortgage rates with clarity instead of confusion.

Conclusion

Knowing today’s 30-year mortgage rates gives you context, but the most important question is how they apply to your refinance or homebuying scenario.

Current rates guide decisions, but personalized lender quotes and total cost comparisons not averages should drive your refinance timing and loan choice.

When you combine current rate context with a clear understanding of your financial goals and eligibility, you’re better positioned to decide whether now is the right time to refinance or lock in a stable 30-year mortgage.

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Next Read

Featured Mortgage Insights

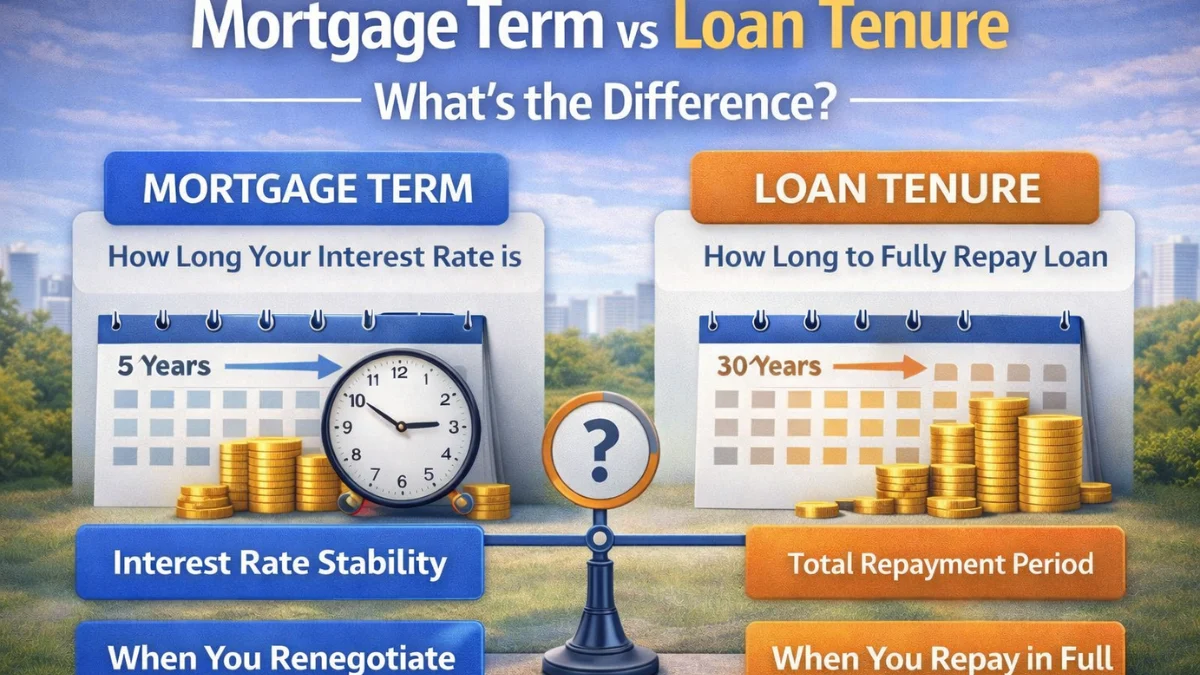

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.

About the Author: Ratiranjan Singha

Don’t Miss These