First-Time Home Buyer Guide: Steps, Costs & Tips

Buying your first home can feel confusing, even if you’ve spent weeks reading about mortgages online. Between mortgage rates today, preapproval..

Buying your first home can feel confusing, even if you’ve spent weeks reading about mortgages online.

Between mortgage rates today, preapproval rules, down payments, and long-term costs, it’s hard to know what actually matters first.

Many first time home buyers worry about getting approved, choosing the right loan, or whether they should refinance later if rates drop.

This page exists to guide you through the entire home buying journey step by step using clear explanations.

First Time Home Buyer Guide

This guide acts as a central roadmap for first time home buyers who want to understand mortgages before making big financial decisions.

Whether you’re trying to get preapproved for a mortgage, compare home loan options, or plan for future refinance opportunities like cash out refinance or VA mortgage refinance, this page connects you to detailed resources across every stage of buying a home.

You’ll find beginner-friendly explanations that help you understand how lenders evaluate applications, how mortgage rates affect affordability, and how decisions made today can impact future options like home refinance, debt consolidation refinance, or refinancing your mortgage when rates improve.

Instead of overwhelming you with everything at once, each section below points you to focused guides so you can learn at your own pace and make confident decisions.

If you’re a first time home buyer, the hardest part is knowing where to begin. Mortgages, lenders, credit scores, and rates can feel overwhelming at first.

This section helps you understand the early steps of buying a home, including how the mortgage process works, what lenders expect, and what mistakes to avoid early on.

Most first-time buyers feel overwhelmed because they don’t know where to begin.

Learning where to start with mortgages gives clarity on the full process before money or emotions get involved.

Understanding mortgage basics for first-time buyers and how the home buying process works helps you see what lenders, agents, and underwriters actually do behind the scenes.

Before contacting a lender, knowing mortgage basics before talking to a lender and learning from things buyers wish they knew early can prevent rushed decisions and costly long-term mistakes.

One of the biggest mistakes first time home buyers make is focusing only on the home price instead of the monthly reality.

Budgeting isn’t just about whether a lender approves you, it’s about whether your payment still feels safe after utilities, groceries, emergencies, and life changes.

Affordability isn’t about the maximum loan amount a lender approves, it’s about what fits your real life. Tools like how much house you can afford and what monthly payment is safe help you set realistic limits.

Many buyers forget expenses explained in hidden home buying costs, which can strain budgets later.

If you’re undecided, renting vs buying helps compare long-term outcomes. Strong preparation includes how much money to save before buying, ensuring emergencies don’t turn into financial stress.

Not all home loans work the same way, and choosing the wrong mortgage type can cost you thousands over time.

First-time buyers should understand the differences between fixed-rate mortgages, adjustable-rate loans, FHA, VA, and conventional options.

Choosing the right loan matters more than chasing the lowest rate. Exploring best mortgage options for first-time buyers helps match loans to income, credit, and savings.

Understanding fixed vs adjustable mortgages prevents surprises later. Buyers comparing programs benefit from conventional vs FHA vs VA loans, while limited savings may require low down payment loan options.

Not every incentive is helpful, first-time buyer programs worth using explains when assistance helps and when it creates hidden costs.

Your credit profile plays a much bigger role in home buying than most first time buyers expect. It affects not just approval, but interest rates, loan options, and long-term cost.

Credit readiness affects both approval and interest rates. Knowing credit score needed to buy sets expectations early. If your credit isn’t perfect, average credit mortgage options and how to improve credit before applying show realistic paths forward.

Many borrowers overlook how student loan debt affects mortgages, while avoidable errors outlined in credit mistakes that hurt approval cause unnecessary denials. Preparing credit properly can save thousands over the life of your loan.

Mortgage preapproval is one of the most important steps for first time home buyers, yet it’s often misunderstood. This section explains how preapproval works, how it differs from prequalification, and what documents lenders require.

Pre-approval is one of the most important steps buyers skip or misunderstand. Learning mortgage pre-approval explained clarifies why it strengthens offers.

Many confuse it with pre-qualification vs pre-approval, which can lead to delays. Knowing documents buyers need and how long approval takes helps avoid last-minute surprises.

Understanding why buyers get denied empowers you to fix issues before submitting applications instead of guessing afterward.

Mortgage rates can change quickly, and timing plays a major role in your monthly payment and long-term cost.

First-time buyers often wonder whether it’s a good time to buy, how rate locks work, and what causes mortgage rates to rise or fall.

Timing affects affordability more than most buyers realize. Reviewing is now a good time to buy helps align decisions with market conditions.

Borrowers who understand how to get the best mortgage rate focus on credit and structure, not just headlines.

Locking decisions are critical; should buyers lock their rate explains the risks of waiting. To avoid confusion, what causes mortgage rates to change and how mortgage rates work provide clarity on why rates move daily.

Many first-time buyers delay buying a home because they believe they need a huge down payment.

In reality, down payment requirements vary by loan type, and closing costs often surprise buyers more than the down payment itself.

Down payments are often misunderstood and overestimated.

Learning how much down payment buyers really need and debunking down payment myths helps buyers move forward sooner.

Many are surprised by fees explained in closing costs for first-time buyers, while assistance options are covered in down payment and closing cost help.

Some loans advertise zero-down options, no down payment mortgages explains when they help and when they increase long-term costs.

Buying your first home comes with hidden assumptions, many of which lenders and agents don’t always explain clearly.

Many first-time buyers lose money due to avoidable mistakes. Learning buyer mistakes that cost thousands helps protect long-term finances.

Understanding what lenders don’t tell buyers and what realtors assume buyers know fills critical knowledge gaps.

Before signing anything, reviewing questions buyers should ask before signing ensures clarity on rates, fees, penalties, and long-term obligations you’ll live with for years.

Getting approved for a mortgage isn’t the finish line, it’s the transition into homeownership.

Approval isn’t the finish line, it’s the transition to ownership. Knowing what happens after approval reduces anxiety before closing.

New homeowners benefit from understanding first mortgage payment expectations, which often differ from estimates.

Many don’t realize how escrow accounts work or when PMI can be removed, both of which directly affect monthly payments. Planning early avoids confusion during your first year of ownership.

Homeownership comes with legal responsibilities, property taxes, and long-term financial decisions that first-time buyers rarely think about upfront.

Homeownership includes long-term responsibilities beyond monthly payments. Understanding mortgage terms buyers should never ignore protects you legally and financially.

Taxes play a major role, how property taxes affect payments explains year-to-year changes.

Buyers should also consider is homeownership worth it long-term, plan for risks like missing a mortgage payment, and think ahead with selling your first home early planning to avoid costly surprises later.

How Mortgage Rates Checker Help First Time Buyers

Mortgage Rates Checker is built for first time home buyers who want clarity before talking to lenders. Instead of guessing numbers, you can start on the Mortgage Rates Checker to understand how home loans, rates and affordability connect in real life.

Tools like the mortgage calculator and mortgage affordability calculator help you estimate realistic monthly payments based on income, down payment, and loan terms, so you don’t fall in love with a home outside your budget.

If you’re trying to time the market, mortgage rates today shows how rate changes affect long-term costs, while calculators like the estimated mortgage calculator and mortgage payment calculator break down principal, interest, taxes, and insurance.

For buyers comparing loan programs, options like the VA loan calculator and USDA home loan calculator explain payments clearly without lender pressure.

If you want deeper Insights, the Mortgage Rates Checker blog and mortgage help FAQs guide you through every step.

Final Thoughts

Buying your first home isn’t something you figure out in one sitting and it shouldn’t be.

Most first time buyers feel confused not because they’re unprepared, but because the information online is scattered, sales-driven, or overly technical.

That’s exactly why Mortgage Rates Checker exists.

You don’t need to rush or talk to a lender before you’re ready. Mortgage Rates Checker is here to help you connect the dots and build confidence.

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Related Posts

Featured Mortgage Insights

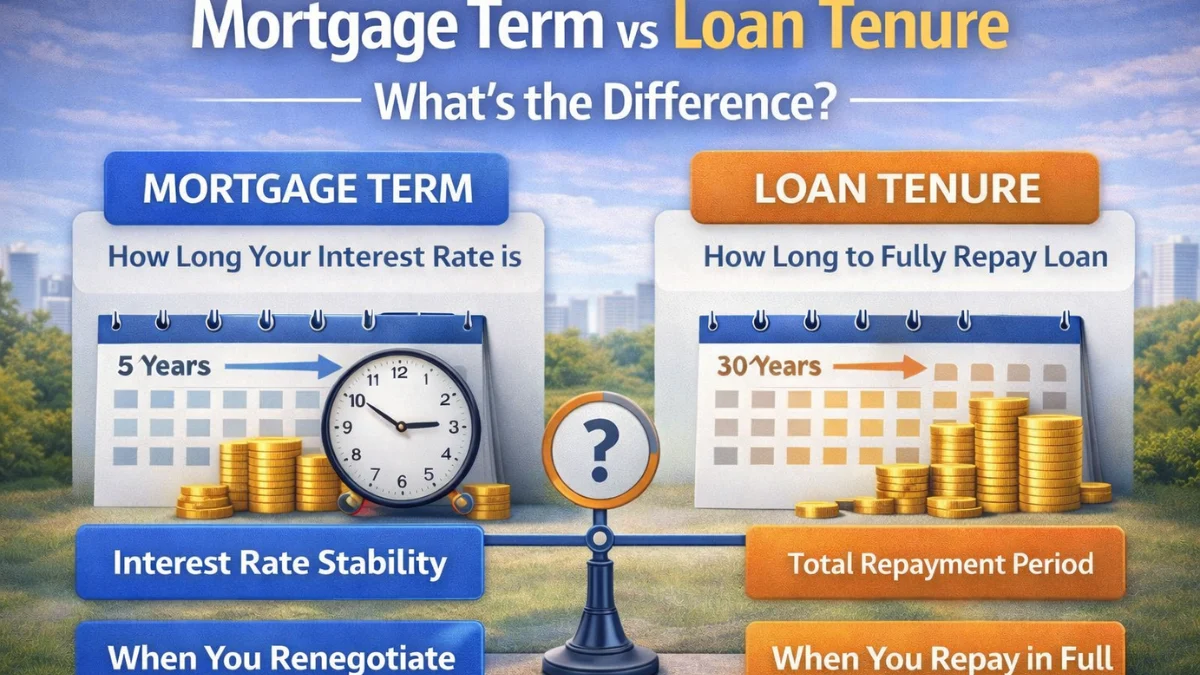

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.