How to Improve Your Chances of Personal Loan Approval

Getting a personal loan approved isn’t just about applying it’s about presenting a strong financial profile.

Many borrowers get rejected because they don’t prepare properly.

This guide shows practical steps to improve your chances of approval and secure better loan terms.

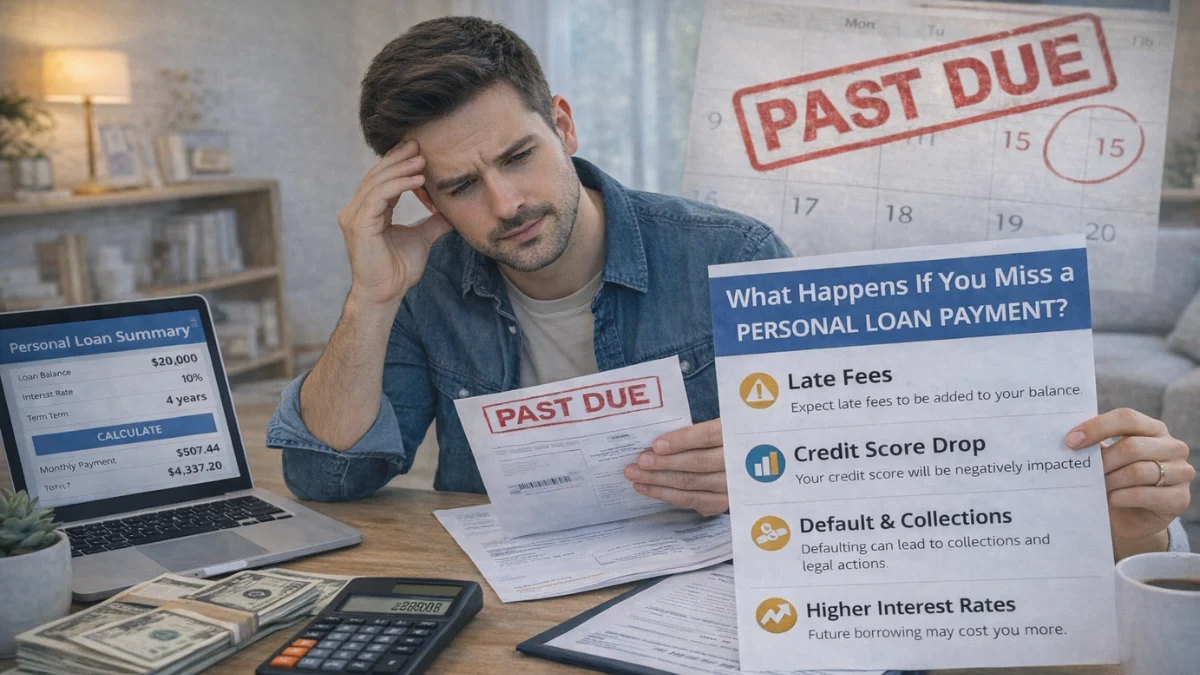

Why Personal Loan Applications Get Rejected

Loan rejections usually happen when lenders see high risk.

This can be due to low credit score, unstable income, high existing debt, or unrealistic loan requests.

Understanding these reasons helps you fix issues before applying.

If you’re new to borrowing, learning how personal loans work in real scenarios can help you approach the process with better preparation.

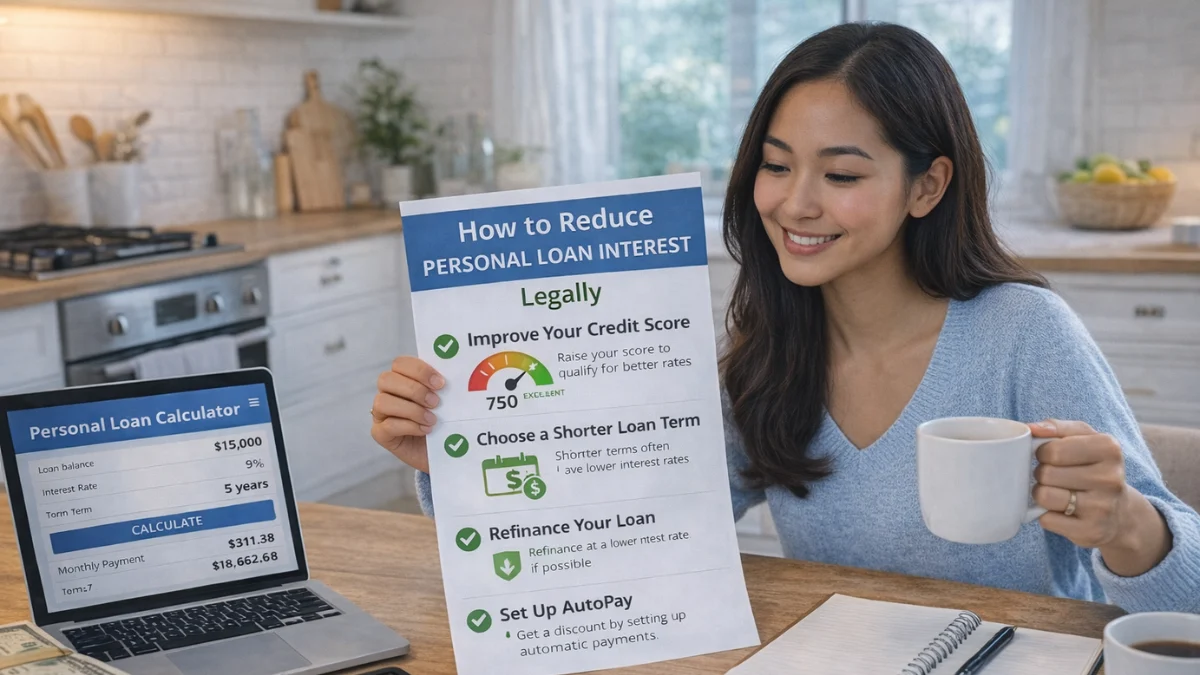

Improve Your Credit Score Before Applying

Your credit score is one of the most important factors lenders consider.

A higher score increases your chances of approval and helps you secure lower interest rates.

You can improve your score by paying bills on time, reducing outstanding debt, and avoiding multiple loan applications. Even small improvements can make a noticeable difference.

Reduce Your Existing Debt

Lenders look at your current financial obligations to assess your repayment capacity.

If you already have multiple loans, your chances of approval may decrease.

Reducing your existing debt lowers your financial burden and improves your profile.

Understanding loan eligibility factors can help you see how your debt level affects approval.

Choose a Realistic Loan Amount

Applying for a loan amount that matches your income increases your chances of approval.

Requesting too much can make lenders see you as a high-risk borrower.

Using a calculator to estimate your EMI can help you choose a realistic amount.

This ensures your loan is affordable and improves approval chances.

Show Stable Income and Employment

A stable income is one of the strongest indicators of your ability to repay a loan.

Lenders prefer borrowers with consistent employment or steady business income.

Providing proof of income, employment history, and financial stability builds trust and increases your chances of approval.

Maintain a Healthy Debt-to-Income Ratio

Your debt-to-income ratio shows how much of your income is already used for repayments. A lower ratio indicates better financial health.

Keeping your total EMIs within a reasonable percentage of your income improves your chances of approval and helps you secure better terms.

Consider Adding a Co-Applicant

Applying with a co-applicant can improve your chances of approval, especially if they have a strong credit profile.

This reduces the lender’s risk and may also help you get a lower interest rate, making the loan more affordable.

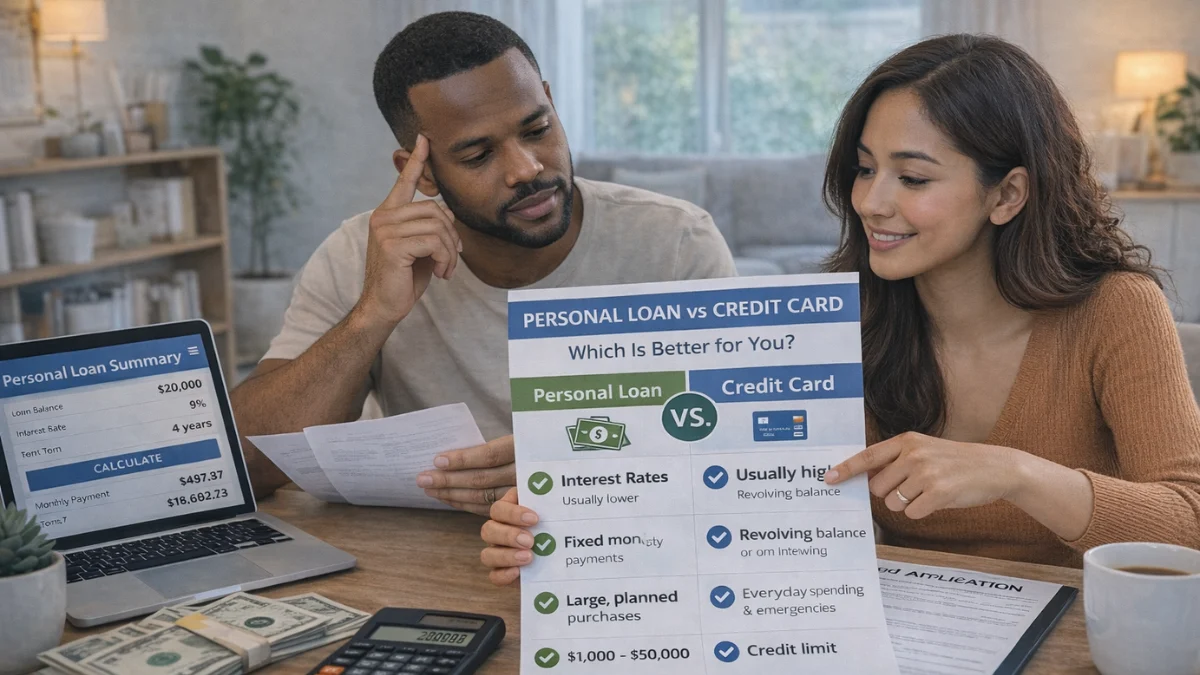

Choose the Right Loan Type

Selecting the right type of loan can also affect your approval chances.

Secured loans are easier to approve because they involve collateral, while unsecured loans require a stronger financial profile.

Understanding secured vs unsecured loan options can help you choose the best approach based on your situation.

Avoid Common Application Mistakes

Simple mistakes like incomplete documentation, multiple applications, or incorrect details can lead to rejection.

Preparing your documents carefully and applying strategically can improve your chances. Learning about common borrowing mistakes can help you avoid these issues.

Why Preparation Matters Before Applying

Improving your approval chances isn’t about luck, it’s about preparation.

By strengthening your financial profile and choosing the right loan structure, you can significantly increase your chances of success.

When combined with a deeper understanding of personal loan strategies and smart borrowing techniques, this preparation becomes even more effective.

Frequently Asked Questions

Conclusion

Improving your chances of personal loan approval requires planning, discipline, and a strong financial profile.

By focusing on key factors like credit score, income, and debt, you can increase your chances of success and secure better loan terms.

Before applying, always prepare carefully and choose a loan that fits your financial situation.

For a complete understanding of borrowing, approval strategies, and cost-saving methods, explore the full guide on how personal loans really work and how to pay less interest to make smarter financial decisions.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.