Personal Loan 2026: How It Really Works, Who Gets Approved & How to Pay Less Interest

Getting a personal loan can feel confusing—interest rates, approvals, hidden charges, and repayment terms can quickly overwhelm you.

Whether you’re borrowing for emergencies, debt consolidation, or big expenses, understanding how a personal loan really works can save you thousands and prevent costly mistakes.

Monthly EMI

$0

Total Interest

$0

Total Payment

$0

What Is a Personal Loan and How Does It Work?

A personal loan is a flexible financing option that allows you to borrow money for almost any purpose—medical bills, travel, debt consolidation, or major purchases.

Unlike home or auto loans, most personal loans are unsecured, meaning you don’t need collateral.

If you’re new, start with what is a personal loan and how does it work to understand the basics.

Once approved, you receive a lump sum and repay it through fixed EMIs over a set period. The interest rate, loan tenure, and fees determine your total repayment cost.

Using a personal loan calculator helps you estimate monthly payments and plan better before applying.

Personal Loan Eligibility: Who Gets Approved?

Approval isn’t random, lenders follow strict criteria to decide who qualifies. Your credit score, income stability, employment history, and existing debts all play a role.

To understand this deeply, check personal loan eligibility how lenders decide your approval. Generally, a higher credit score and lower debt-to-income ratio improve your chances significantly.

Lenders also look at your repayment history to assess risk. If you want to boost approval odds, improving your credit profile and maintaining stable income are key strategies.

Secured vs Unsecured Personal Loan: Which One Is Better?

Personal loans come in two types—secured and unsecured. Secured loans require collateral like property or savings, while unsecured loans rely entirely on your creditworthiness.

If you’re unsure which to choose, read secured vs unsecured personal loan key differences explained. Secured loans usually offer lower interest rates but carry risk if you default.

Unsecured loans are faster and easier to access but often come with higher rates. The right choice depends on your financial situation and risk tolerance.

How to Get a Personal Loan with Bad Credit

Having a low credit score doesn’t mean you’re out of options. Many lenders still offer loans, but with stricter terms or higher interest rates.

A detailed approach is explained in how to get a personal loan with bad credit.

You can improve your chances by applying with a co-applicant, choosing smaller loan amounts, or opting for secured loans.

Even small improvements in your credit score before applying can make a big difference in approval and interest rates.

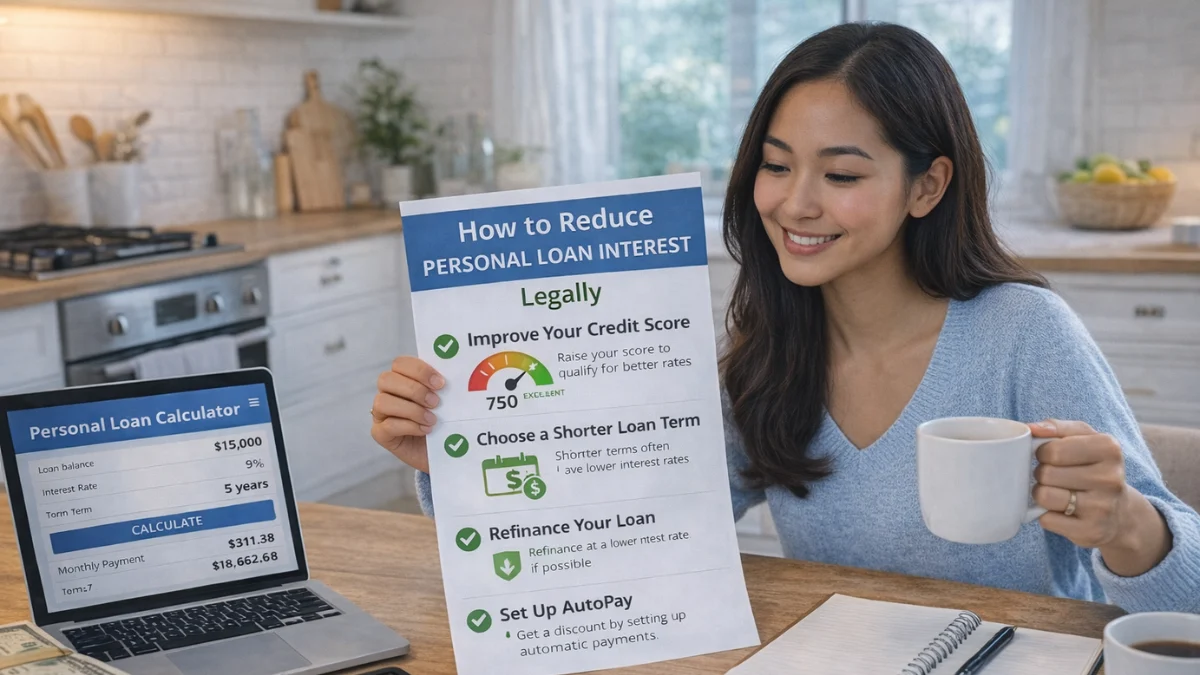

Personal Loan Interest: How It Works and How to Pay Less

Interest is the biggest cost of any personal loan. It can significantly increase your total repayment amount if not managed properly.

To reduce costs, explore how to reduce personal loan interest legally. Choosing shorter loan terms, negotiating rates, and improving your credit score can lower interest.

Comparing lenders before applying is also crucial. Even a small difference in interest rate can save you a large amount over time.

Personal Loan Repayment: What You Need to Know

Repayment is where most borrowers struggle if they don’t plan ahead.

Personal loans are typically repaid in fixed monthly installments, which include both principal and interest.

For a full breakdown, check personal loan repayment guide how it actually works. Missing payments can lead to penalties, increased interest, and credit score damage.

Setting up auto-pay and budgeting your EMIs properly ensures you stay on track and avoid unnecessary stress.

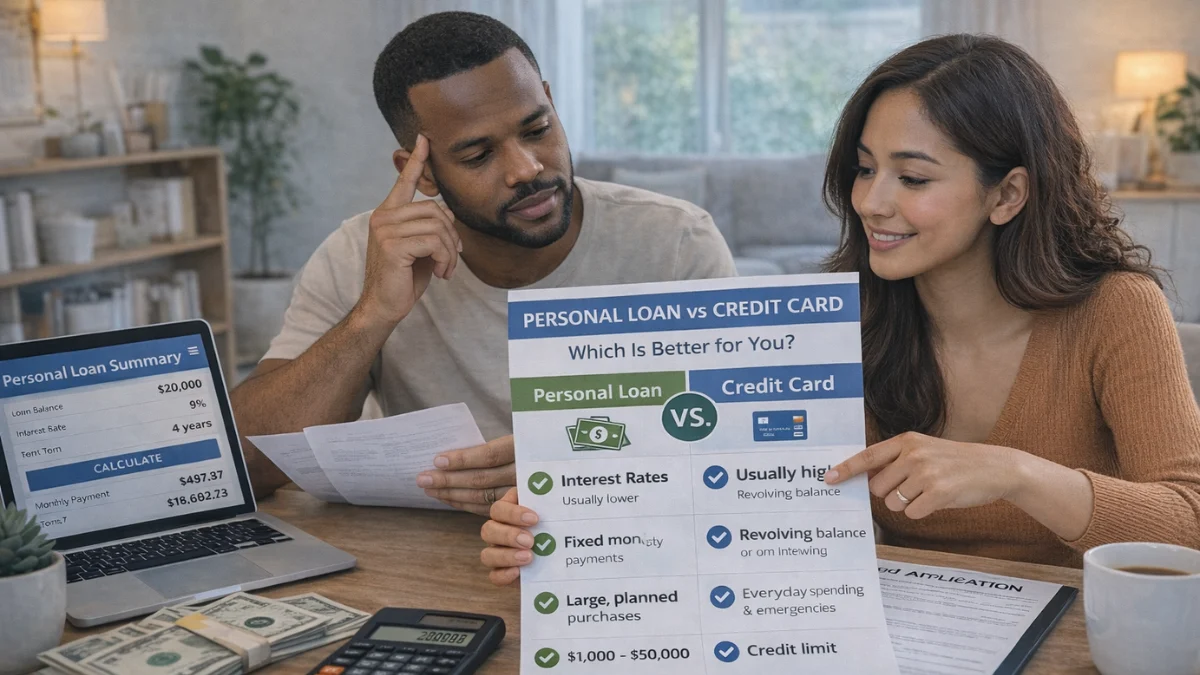

Personal Loan vs Credit Card: Which Is Better?

Many people confuse personal loans with credit cards, but they serve different purposes. Personal loans are better for large, planned expenses, while credit cards are useful for short-term spending.

To compare both, read personal loan vs credit card which is better for you.

Personal loans offer lower interest rates and structured repayment, whereas credit cards provide flexibility but can become expensive if not managed well.

Choosing the right option depends on your financial needs and discipline.

How to Improve Your Chances of Personal Loan Approval

If you want fast approval with better terms, preparation is key. Lenders prefer borrowers who show financial stability and responsible credit behavior.

You can follow proven strategies in how to improve your chances of personal loan approval. This includes maintaining a high credit score, reducing existing debt, and applying for the right loan amount.

Timing also matters—applying when your financial profile is strong increases your approval odds significantly.

Common Personal Loan Mistakes to Avoid

Many borrowers make mistakes that cost them money in the long run.

These include borrowing more than needed, ignoring hidden fees, or choosing longer tenures unnecessarily.

Avoid these pitfalls by reading common personal loan mistakes and how to avoid them.

Always compare lenders, read terms carefully, and calculate your EMI before committing. Smart borrowing decisions can prevent financial stress later.

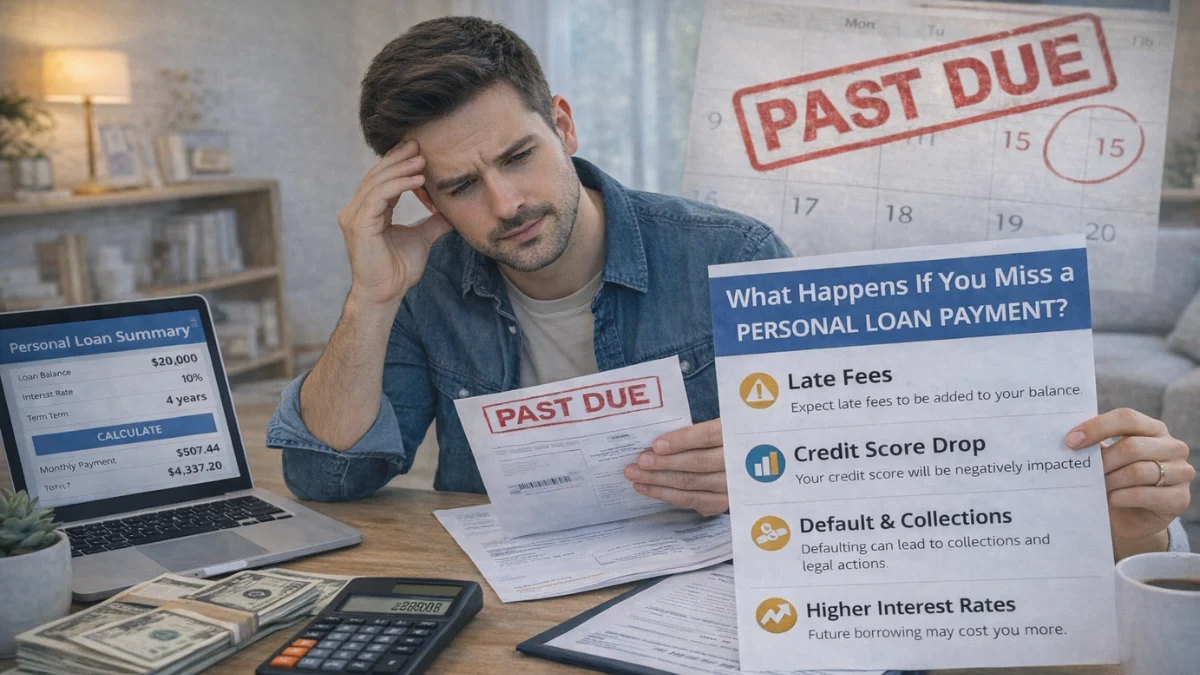

What Happens If You Miss a Personal Loan Payment?

Missing even one payment can have serious consequences. It can affect your credit score, add penalties, and increase your financial burden.

To understand the impact, check what happens if you miss a personal loan payment. Repeated defaults can lead to legal action or collection processes.

If you’re struggling, it’s better to contact your lender early and explore restructuring options instead of ignoring the problem.

Frequently Asked Questions

Conclusion

A personal loan can be a powerful financial tool when used wisely, but it can also become a burden if you don’t understand how it works.

From eligibility and interest rates to repayment and mistakes, every step matters.

The key is to borrow smart, plan your repayment, and always compare options before making a decision.

When you approach it strategically, a personal loan can help you achieve your financial goals without unnecessary stress.