Personal Loan Eligibility: How Lenders Decide Your Approval

Getting a personal loan isn’t just about applying, it’s about meeting the right criteria.

Many borrowers get rejected simply because they don’t understand how lenders evaluate eligibility.

This guide explains exactly what lenders look for so you can improve your chances of approval.

What Is Personal Loan Eligibility?

Personal loan eligibility refers to the criteria lenders use to decide whether you qualify for a loan.

These criteria ensure that you have the financial capacity to repay the borrowed amount without defaulting.

Every lender has slightly different requirements, but the core factors remain the same.

If you’re new to borrowing, understanding how personal loans work in real life will give you a strong foundation before focusing on eligibility.

Credit Score: The Most Important Factor

Your credit score is one of the first things lenders check. It reflects your past borrowing behavior and repayment history.

A higher score increases your chances of approval and helps you secure lower interest rates. On the other hand, a low score may lead to rejection or higher costs.

If your score isn’t ideal, you can still explore strategies for getting a loan with low credit, but terms may vary.

Income and Repayment Capacity

Lenders want to ensure that you can comfortably repay the loan. Your monthly income plays a key role in determining your eligibility.

They usually compare your income with your existing financial obligations to calculate your repayment capacity.

If your income is stable and sufficient, your chances of approval improve significantly.

This is why it’s important to plan your EMI using tools and understand your repayment structure before applying.

Debt-to-Income Ratio (DTI)

Your debt-to-income ratio shows how much of your income is already used to pay existing loans. A high DTI signals higher risk to lenders.

Ideally, your total EMIs (including the new loan) should not exceed a certain percentage of your income.

Managing your debts wisely can improve your eligibility and help you secure better loan terms.

Employment Stability and Job Profile

Lenders prefer borrowers with stable jobs or consistent business income. Your employment type, whether salaried or self-employed—also affects your eligibility.

A stable job history with consistent income increases trust and improves your chances of approval.

If you’re self-employed, maintaining proper financial records becomes even more important.

Loan Amount and Tenure Selection

The loan amount and tenure you choose also impact your eligibility. A higher loan amount or shorter tenure increases your EMI, which can reduce your chances of approval.

Using a calculator to choose a realistic EMI can make a big difference. This helps you align your loan with your financial capacity and avoid rejection.

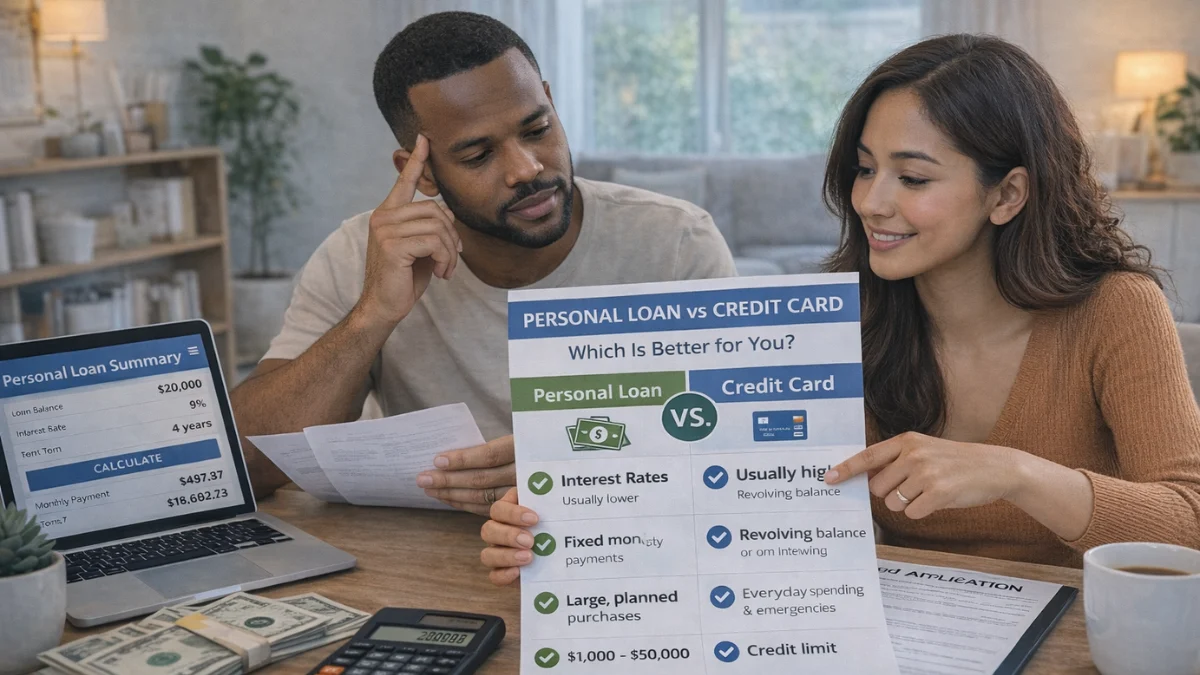

Secured vs Unsecured Loan Impact

Most personal loans are unsecured, but in some cases, lenders may offer secured options that are easier to approve.

Secured loans come with lower risk for lenders, which can improve your chances of approval.

Understanding secured vs unsecured loan differences can help you choose the right option based on your situation.

How to Improve Your Personal Loan Eligibility

Improving your eligibility doesn’t always require major changes. Small adjustments can significantly increase your chances of approval.

You can improve your profile by:

- Maintaining a good credit score

- Reducing existing debt

- Choosing a lower loan amount

- Showing stable income

If you want to maximize your chances, learning how to improve loan approval chances can give you a clear strategy before applying.

Common Reasons Why Loans Get Rejected

Many applications are rejected due to avoidable mistakes. Some common reasons include low credit score, high debt, unstable income, or applying for unrealistic loan amounts.

Understanding these mistakes can help you prepare better and avoid rejection. Learning about common borrowing mistakes can save you time and improve your success rate.

Why Eligibility Matters Before Applying

Checking your eligibility before applying helps you avoid unnecessary rejections, which can negatively impact your credit score.

It also helps you choose the right loan amount and repayment plan.

When combined with a deeper understanding of personal loan strategies and interest reduction, eligibility planning becomes a powerful step toward financial stability.

Frequently Asked Questions

Conclusion

Personal loan eligibility is not just about meeting basic requirements—it’s about presenting a strong financial profile that lenders trust.

By understanding how lenders evaluate your application, you can improve your chances of approval and secure better loan terms.

Before applying, always assess your financial situation, choose the right loan amount, and plan your repayment carefully.

For a complete understanding of borrowing, approval strategies, and cost-saving tips, explore the full guide on how personal loans really work and how to pay less interest to make smarter financial decisions.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.