Personal Loan vs Credit Card: Which Is Better for You?

When you need money, choosing between a personal loan and a credit card can be confusing. Both offer quick access to funds, but they work very differently.

This guide helps you understand which option is better based on your needs and financial situation.

What Is a Personal Loan?

A personal loan is a lump sum amount borrowed from a lender and repaid in fixed monthly installments over a specific period.

It usually comes with a fixed interest rate and predictable repayment schedule.

This makes it ideal for planned expenses like medical bills, home improvement, or debt consolidation.

If you’re new to borrowing, understanding how personal loans work in real situations can help you see why they are often more structured and cost-effective.

What Is a Credit Card?

A credit card allows you to borrow money up to a certain limit and repay it later.

Unlike personal loans, it offers revolving credit, meaning you can reuse the available limit after repayment.

While this flexibility is convenient, credit cards often come with higher interest rates, especially if you don’t pay your full balance on time.

Key Differences Between Personal Loan and Credit Card

The biggest difference lies in how the money is borrowed and repaid.

Personal loans provide a fixed amount with a clear repayment plan, while credit cards offer ongoing access to funds without a fixed schedule.

Interest rates are typically lower for personal loans, making them more cost-effective for larger expenses. Credit cards, on the other hand, are better suited for short-term or smaller purchases.

Understanding these differences can help you avoid common borrowing mistakes and choose the right option.

Interest Rates and Cost Comparison

Personal loans generally have lower interest rates compared to credit cards. This makes them a better choice for large expenses that require longer repayment periods.

Credit cards can become expensive if you carry a balance, as interest rates are usually much higher.

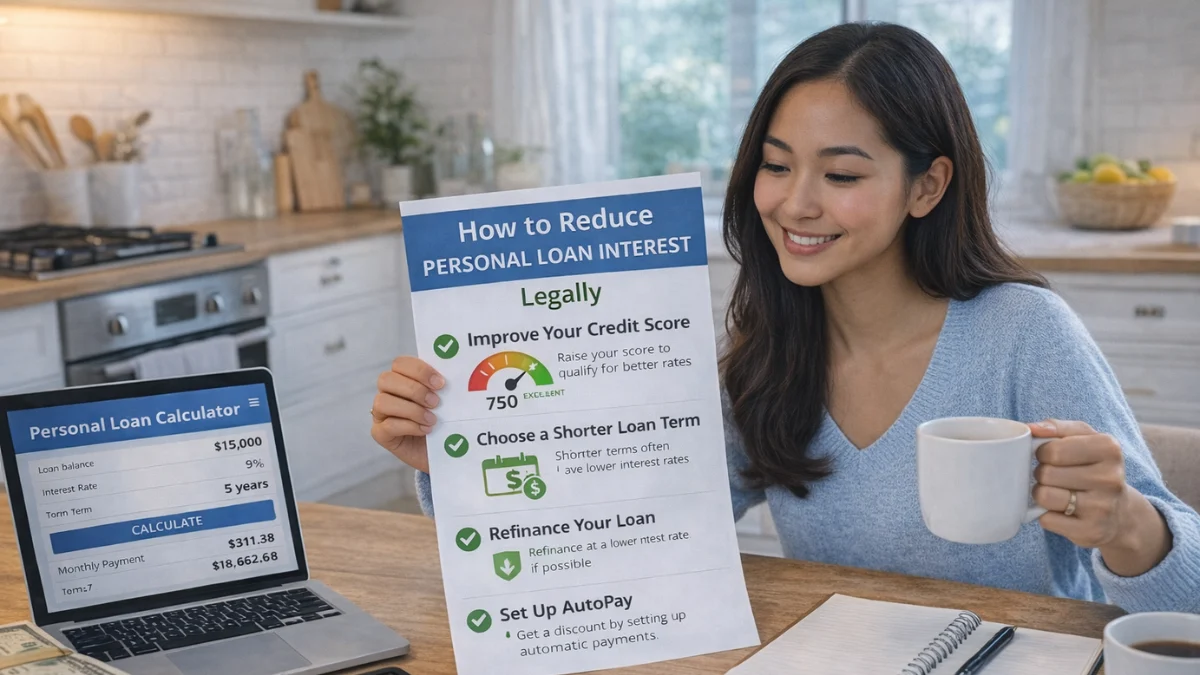

If you want to minimize costs, exploring ways to reduce loan interest legally can help you save money with personal loans.

Flexibility vs Structure

Credit cards offer more flexibility because you can borrow and repay repeatedly without reapplying. This makes them useful for emergencies or short-term needs.

Personal loans, however, provide structure with fixed EMIs and a defined repayment period. This makes budgeting easier and reduces the risk of long-term debt.

When a Personal Loan Is Better

A personal loan is usually the better option when:

- You need a large amount of money

- You want lower interest rates

- You prefer fixed monthly payments

- You need a clear repayment timeline

It is especially useful for planned expenses where you want to control your total cost.

When a Credit Card Is Better

A credit card may be a better choice when:

- You need quick access to small amounts

- You can repay the balance quickly

- You want flexibility in spending

- You want to take advantage of rewards or cashback

However, it’s important to use it responsibly to avoid high interest charges.

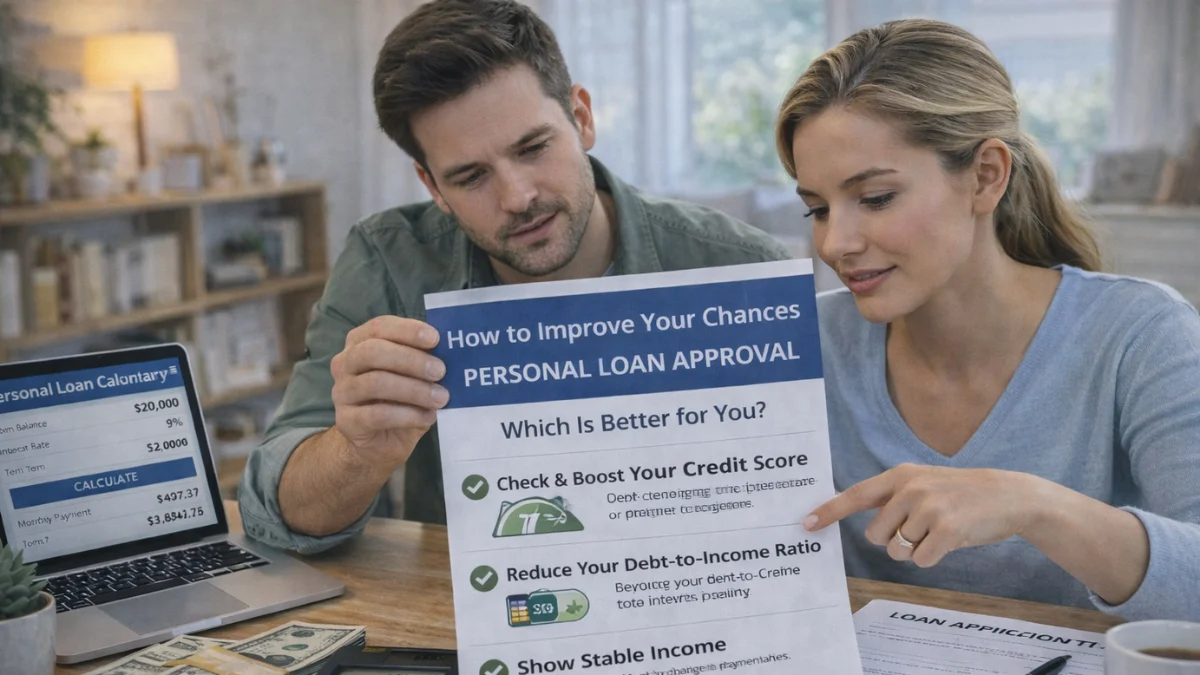

Impact on Approval and Eligibility

Personal loans require a detailed approval process based on your income, credit score, and financial profile.

Credit cards also consider these factors but may have simpler approval requirements.

If you’re unsure about qualifying for a loan, understanding loan eligibility factors can help you prepare and improve your chances of approval.

Risk and Financial Impact

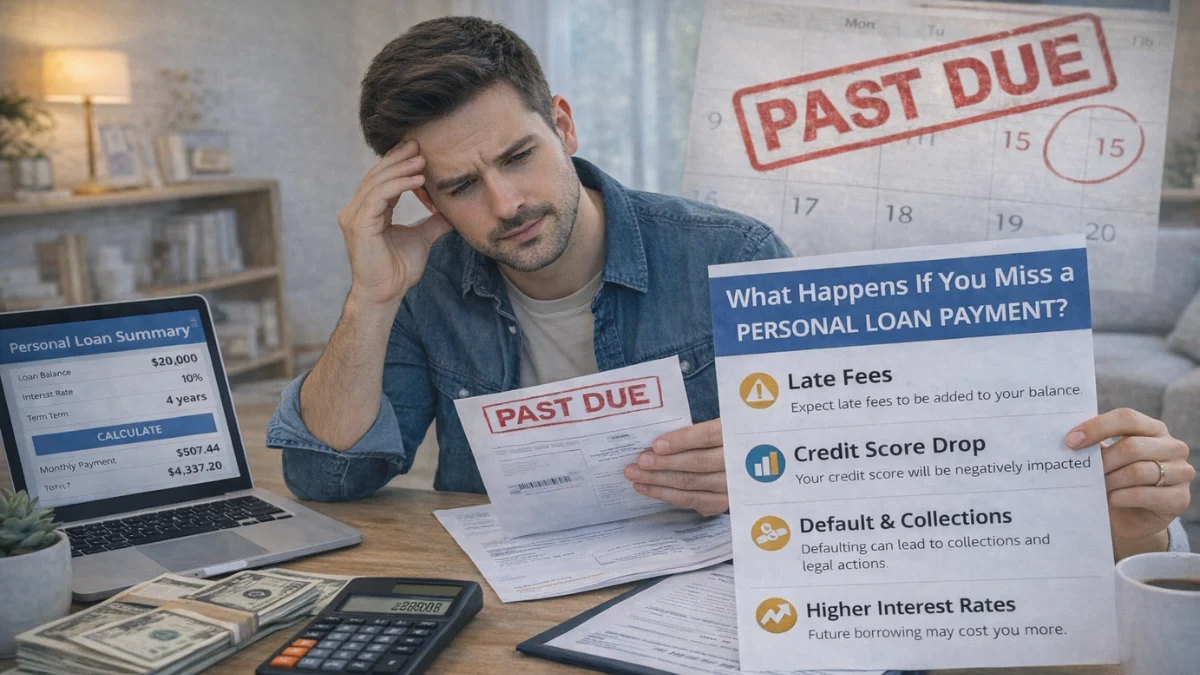

Both options come with risks if not managed properly. Missing payments on a personal loan can lead to penalties and credit score damage.

With credit cards, carrying a balance over time can result in high interest and growing debt.

Understanding what happens when you miss a loan payment can help you stay disciplined and avoid financial trouble.

Which One Should You Choose?

The right choice depends on your financial needs and repayment ability.

- Choose a personal loan for large, planned expenses with structured repayment

- Choose a credit card for short-term, flexible borrowing

Before deciding, evaluate your budget, interest costs, and repayment capacity.

This becomes easier when you explore personal loan strategies and smart borrowing techniques to make informed decisions.

Frequently Asked Questions

Conclusion

Both personal loans and credit cards have their advantages, but choosing the right one depends on your financial situation and borrowing needs.

Understanding the differences helps you avoid unnecessary costs and manage your finances more effectively.

Before making a decision, always compare options and plan your repayment carefully.

For a complete understanding of borrowing strategies, approval tips, and cost-saving methods, explore the full guide on how personal loans really work and how to pay less interest to make smarter financial decisions.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.