Refinance Readiness Checker: Are You Ready to Refinance?

Refinancing can feel like an easy decision when you hear people say “rates are dropping” or “you can..

Refinancing can feel like an easy decision when you hear people say “rates are dropping” or “you can save hundreds per month.” But in reality, refinancing only makes sense when your financial profile, home equity, and timeline line up correctly.

This Refinance Readiness Checker is designed to help homeowners estimate whether refinancing could be worth exploring right now.

It evaluates common lender factors like credit score strength, debt-to-income ratio, home equity position, and rate savings potential.

Instead of guessing, you get a score and clear next-step guidance so you can make a smarter refinance decision before requesting lender quotes.

How the Refinance Readiness Checker Works?

This tool is built around the same core questions lenders and experienced homeowners ask before refinancing.

It evaluates whether refinancing may be financially beneficial based on rate improvement potential, credit strength, home equity, debt-to-income ratio, and how long you plan to stay in the home.

These factors determine not just approval, but whether the refinance actually saves money after closing costs.

Many people refinance too early and end up paying fees without breaking even. That’s why the tool gives you a readiness score along with a breakdown of the strongest and weakest areas in your refinance profile.

If you want a deeper explanation of the refinance process, the Ultimate Guide to Refinancing Your Mortgage is a great starting point because it covers refinancing options, timing, and what lenders evaluate.

This tool is designed to give you clarity before you request quotes.

Refinancing only makes sense if the savings outweigh the closing costs. Many homeowners refinance too early, lock in a small rate drop, and end up paying fees without reaching the break-even point. Always compare loan estimates and calculate long-term savings before committing.

When Refinancing Actually Makes Sense?

Refinancing is not automatically a smart move just because rates drop slightly. In most cases, refinancing makes sense when the new loan creates meaningful monthly savings, reduces total interest over time, or improves loan stability.

For example, switching from an adjustable-rate mortgage to a fixed-rate loan can reduce long-term risk even if the rate savings are small. But if your rate improvement is minimal and closing costs are high, refinancing may not be worth it.

Many homeowners forget that refinancing is essentially taking out a brand-new loan, meaning fees, appraisal requirements, and lender underwriting still apply.

If you’re unsure about timing, reading should I refinance my mortgage right now and refinance mortgage when does it actually make sense can help you understand the real-world situations where refinancing works best.

Why Credit Score and Home Equity Matter More Than Most People Expect?

Two homeowners with the same mortgage balance can receive completely different refinance offers based on credit and equity.

Credit score affects the interest rate you qualify for, while equity affects lender risk and loan-to-value requirements. If you have less equity, you may face higher rates or additional mortgage insurance, which reduces savings.

That’s why refinance readiness is not just about interest rates, it’s about your financial profile. Equity becomes even more important if you’re considering cash-out refinancing, because lenders have stricter requirements for pulling money out of your home.

If you want to understand equity-driven options, the guides on cash-out refinance and home equity cash-out refinance explain the risks and benefits clearly.

The tool score helps highlight whether your equity position is strong enough to make refinancing worthwhile or whether waiting could produce a better outcome.

How Closing Costs and Break-Even Time Impact Your Savings?

One of the biggest mistakes homeowners make is focusing only on the monthly payment reduction and ignoring refinance closing costs.

Refinancing usually includes lender fees, appraisal costs, title work, and sometimes discount points. Even if you save money monthly, you may need years to recover the upfront costs.

This is why break-even time matters. If you plan to sell the home soon, refinancing might actually lose money.

A refinance can still make sense if it helps you shorten your loan term, remove mortgage insurance, or switch to a more stable loan structure. But the math must be clear.

If you want to understand cost breakdowns, the articles refinance closing costs what you’ll actually pay and cost to refinance a house full breakdown are extremely helpful.

After using this tool, it’s smart to confirm savings using a refinance break-even tool.

What to Do After You Get Your Refinance Readiness Score?

Once you receive your readiness score, the next step depends on whether refinancing looks strong, moderate, or weak. If your score is strong, your next move should be to compare refinance quotes from multiple lenders and focus on the full loan estimate, not just the advertised rate.

If your score is moderate, improving credit score or increasing equity can significantly improve your refinance offer. If your score is low, refinancing may still be possible but not cost-effective right now.

In that case, waiting for better rates or improving your debt-to-income ratio could lead to better savings later. For quote comparisons, the guide mortgage refinance quotes how to compare them correctly explains what to look for.

If you want to check current market direction, current refinance rates and refinance interest rates how they really work are useful resources.

This tool is designed to guide your decision before you commit.

Frequently Asked Questions

Mortgage Calculator

Recommended Mortgage Tools

Refinance Break-Even Calculator

See how long it takes to recover refinance costs.

Debt-to-Income Ratio Calculator

Check if your income supports mortgage approval.

Refinance Readiness Checker

Find out if now is the right time to refinance.

Mortgage Eligibility Checker

Quickly see if you qualify for a home loan.

First-Time Buyer Readiness

Know if you're ready to buy your first home.

Mortgage Pre-Approval Calculator

Estimate how much you can borrow instantly.

Related Posts

Featured Mortgage Insights

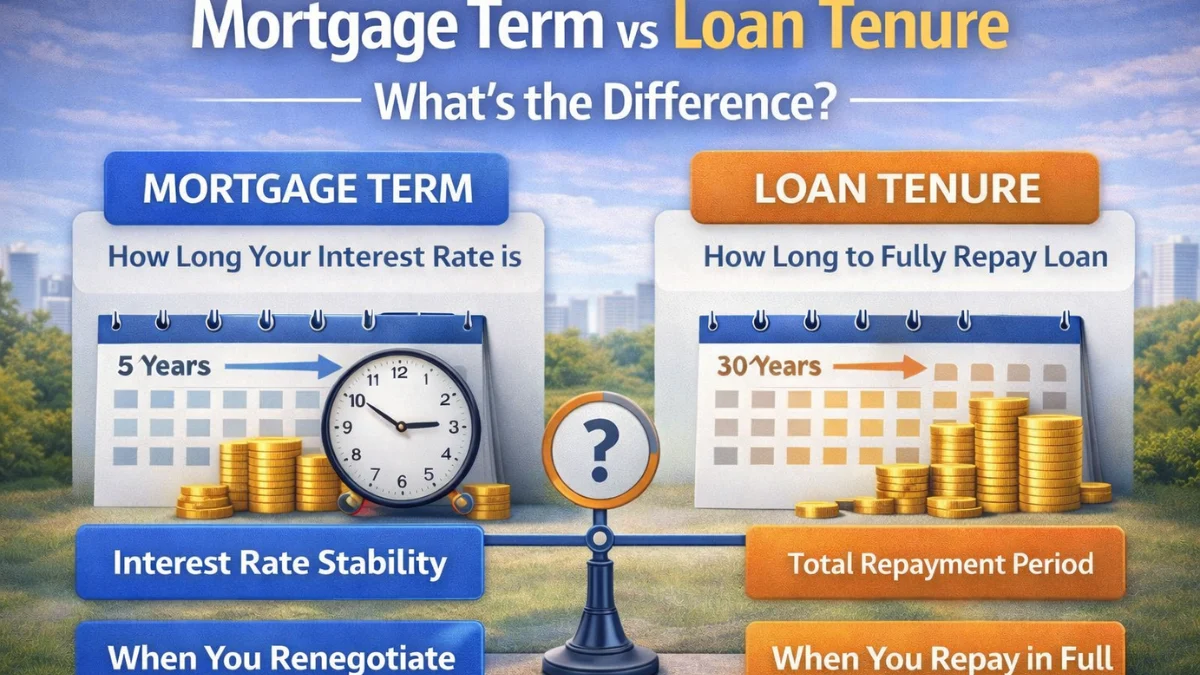

Mortgage term is the period your interest rate is fixed, while loan tenure is the total time to repay the loan. Both impact payments, refinancing, and total interest.

Featured Mortgage Insights

Mortgage rates are influencing buyer budgets more than expected as borrowing costs directly affect monthly payments and long-term affordability. Many buyers are adjusting spending limits and home search plans to align mortgage commitments with financial stability.

Featured Mortgage Insights

Many homebuyers are closely watching mortgage rates before making property offers, as borrowing costs directly influence affordability and monthly payments. Rate movements are increasingly shaping purchase timing and buyer confidence across today’s housing market.