Secured vs Unsecured Personal Loan: Key Differences Explained

Choosing between a secured and unsecured personal loan can significantly impact your interest rate, approval chances, and financial risk.

Many borrowers pick the wrong option simply because they don’t understand the differences.

This guide explains everything clearly so you can make the right decision.

What Is a Secured Personal Loan?

A secured personal loan is backed by an asset such as property, fixed deposits, or other valuable collateral.

This reduces the lender’s risk, which is why secured loans usually come with lower interest rates and higher borrowing limits.

Because the lender has security, approval is often easier, even if your credit score isn’t perfect.

If you’re new to borrowing, understanding how personal loans work in real scenarios can help you see where secured loans fit into your financial strategy.

What Is an Unsecured Personal Loan?

An unsecured personal loan does not require any collateral.

Instead, lenders rely on your credit score, income, and financial history to assess your eligibility.

These loans are faster to process and more flexible, making them popular for urgent needs.

However, they usually come with higher interest rates because the lender takes on more risk.

If you’re unsure about approval, learning about loan eligibility factors can help you understand how lenders evaluate unsecured applications.

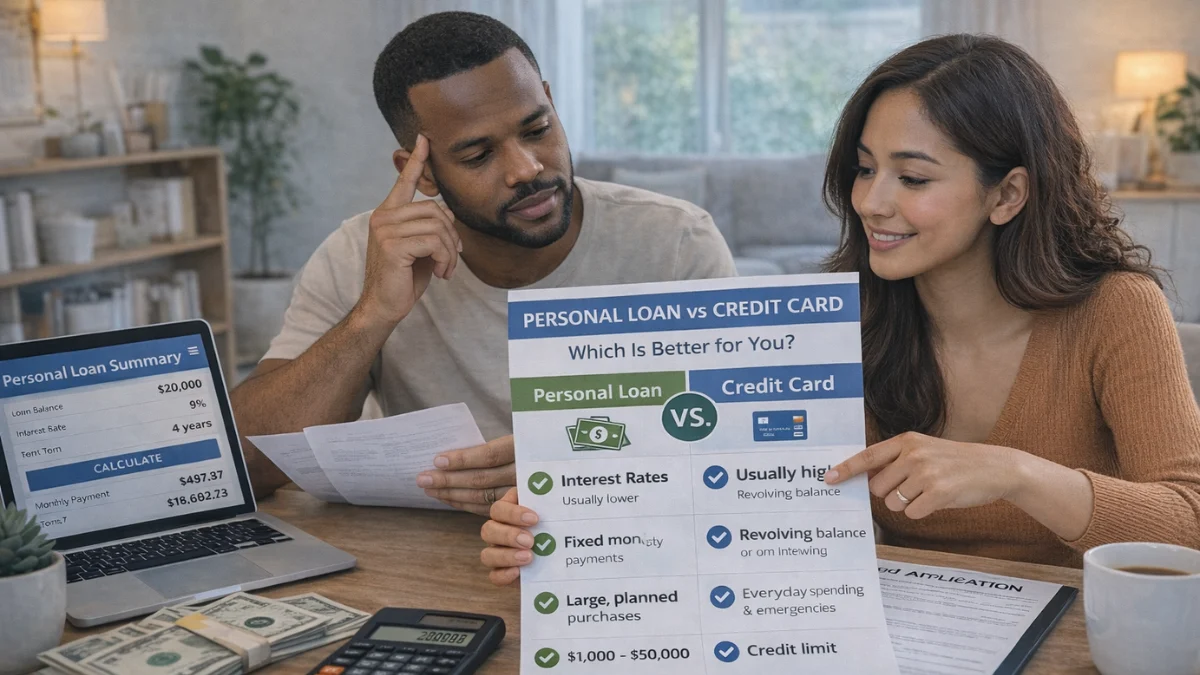

Key Differences Between Secured and Unsecured Loans

The main difference lies in risk and cost. Secured loans are less risky for lenders, which translates into lower interest rates for borrowers.

Unsecured loans, on the other hand, are more convenient but often more expensive.

Another key difference is approval criteria. Secured loans may be easier to obtain, while unsecured loans require a stronger financial profile.

Understanding these differences can help you avoid common borrowing mistakes and choose the right option for your needs.

Interest Rates and Cost Comparison

Interest rates are typically lower for secured loans because the lender has collateral as protection.

This can result in significant savings over time, especially for large loan amounts.

Unsecured loans usually have higher interest rates, which increases your total repayment cost.

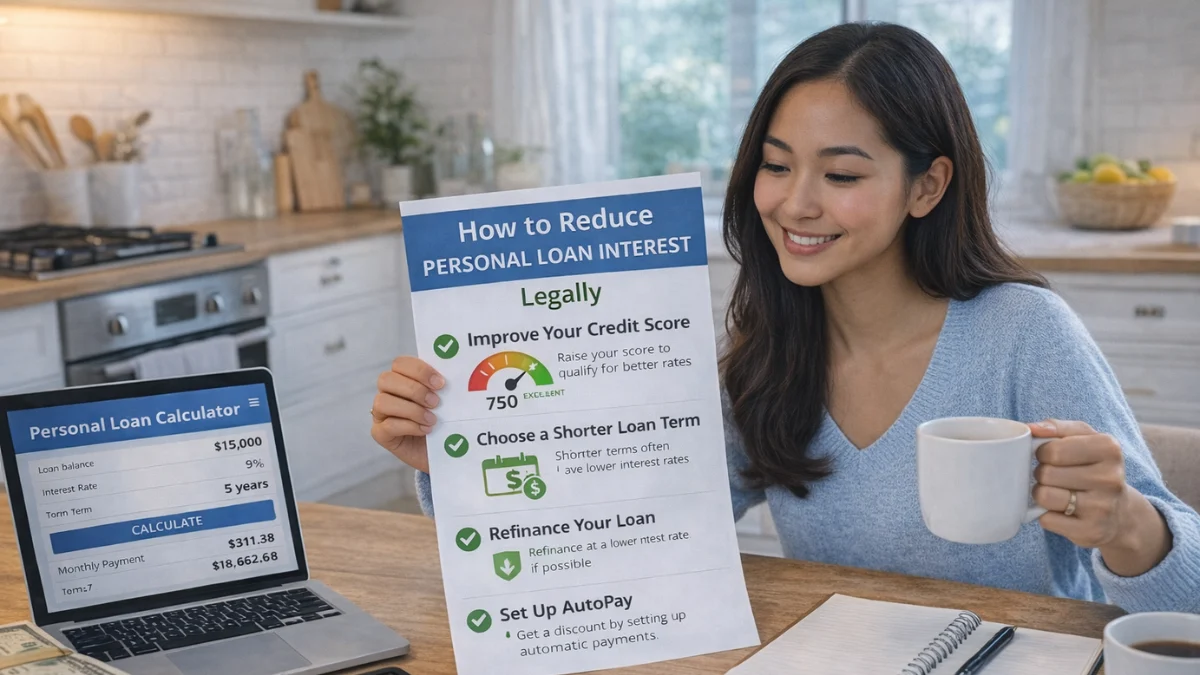

If you want to minimize expenses, exploring strategies to reduce loan interest legally can help you make smarter borrowing decisions.

Approval Process and Eligibility

Secured loans often have a simpler approval process because the collateral reduces risk.

However, they may require additional documentation related to the asset.

Unsecured loans rely heavily on your credit score and income. A strong financial profile improves your chances of approval and helps you secure better terms.

If your credit score is low, you can explore options for getting a loan with bad credit to increase your chances.

Risk and Financial Impact

The biggest risk with secured loans is losing your collateral if you fail to repay the loan.

This makes them riskier from a borrower’s perspective, even though they offer lower interest rates.

Unsecured loans don’t involve collateral, but defaulting can still damage your credit score and lead to legal consequences.

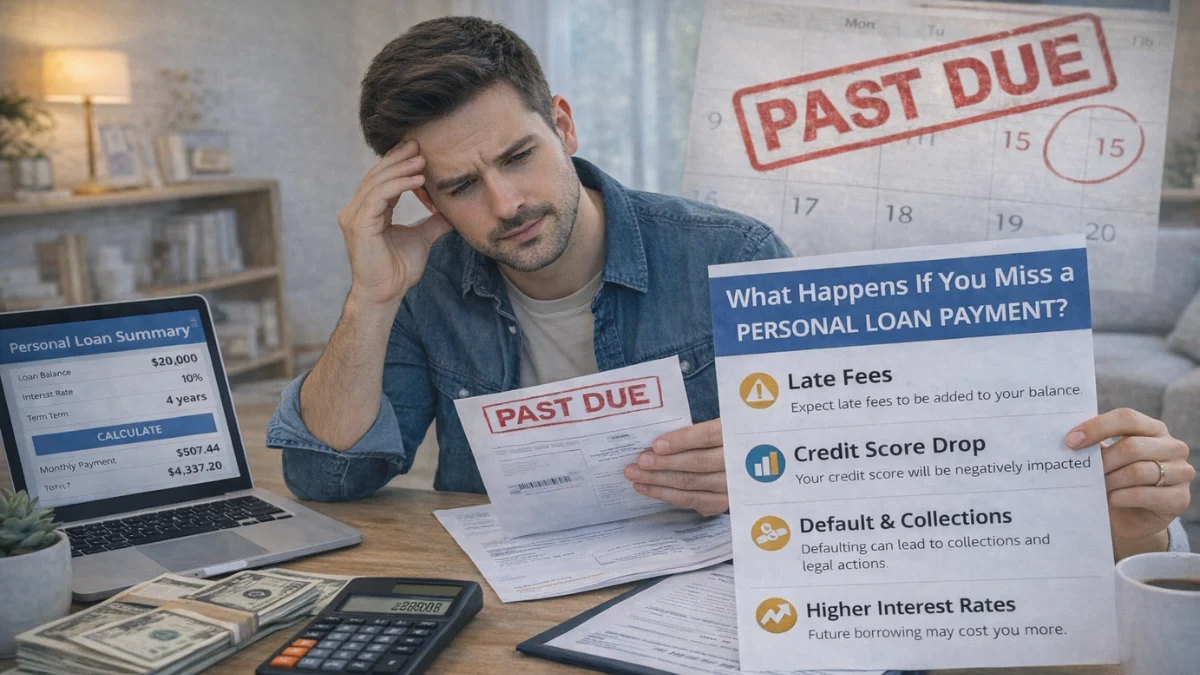

Understanding what happens when you miss a loan payment can help you manage your loan responsibly and avoid long-term financial damage.

Which One Should You Choose?

The right choice depends on your financial situation, risk tolerance, and borrowing needs.

- Choose a secured loan if you want lower interest rates and have an asset to pledge

- Choose an unsecured loan if you need quick access to funds without risking assets

Before deciding, it’s important to evaluate your repayment capacity and loan structure.

This becomes easier when you explore personal loan strategies and smart borrowing techniques to make informed decisions.

When Secured Loans Make More Sense

Secured loans are ideal when you need a large loan amount or want to reduce your interest cost.

They are also useful if your credit score is not strong enough for an unsecured loan.

However, you should only choose this option if you are confident in your repayment ability, as your asset is at risk.

When Unsecured Loans Are Better

Unsecured loans are better for smaller amounts or when you need quick approval. They are also suitable if you don’t want to risk your assets.

While they may cost more in interest, their flexibility and speed make them a popular choice for many borrowers.

Why Understanding This Difference Matters

Choosing the wrong type of loan can lead to higher costs or unnecessary risks.

By understanding the differences between secured and unsecured loans, you can make smarter financial decisions and avoid common pitfalls.

This knowledge becomes even more valuable when combined with a complete understanding of how personal loans really work and how to pay less interest, helping you optimize your borrowing strategy.

Frequently Asked Questions

Conclusion

Secured and unsecured personal loans serve different purposes, and choosing the right one depends on your financial goals and risk tolerance.

While secured loans offer lower costs, unsecured loans provide flexibility and speed.

Before making a decision, always evaluate your repayment capacity and long-term financial impact.

For a complete understanding of borrowing strategies, approval tips, and cost-saving methods, explore the full guide on personal loan strategies and smart financial planning to make confident financial decisions.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.