What Is a Personal Loan and How Does It Work?

A personal loan is one of the most common ways to borrow money, but many people don’t fully understand how it works until they start repaying it.

This guide breaks down everything in simple terms so you can make informed decisions and avoid costly mistakes.

What Is a Personal Loan in Simple Terms?

A personal loan is a type of unsecured loan that allows you to borrow money for almost any purpose—whether it’s medical expenses, home renovation, travel, or debt consolidation.

Unlike secured loans, you usually don’t need to provide collateral. Instead, lenders evaluate your credit score, income, and financial history.

If you’re new to borrowing, understanding how personal loans fit into your overall financial plan becomes easier when you explore personal loan basics and smart borrowing strategies.

How Does a Personal Loan Work Step by Step?

A personal loan follows a simple process from application to repayment.

First, you apply with a lender and provide details about your income and credit profile.

Once approved, the lender disburses a lump sum amount directly to your account.

You then repay the loan in fixed monthly installments over a specific period. Each EMI includes both principal and interest.

If you want to understand this process in detail, exploring a repayment guide can help you see how payments are structured over time.

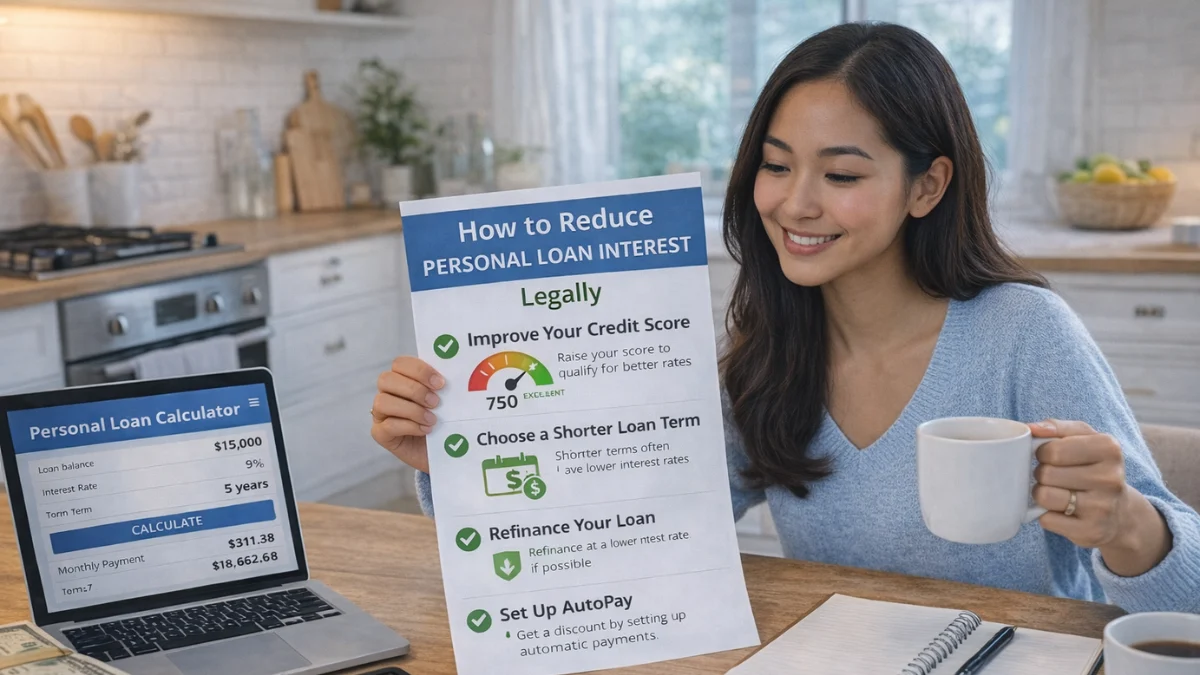

How Interest Works on a Personal Loan

Interest is the cost you pay for borrowing money. It is calculated based on your loan amount, interest rate, and tenure.

Most personal loans use reducing balance interest, meaning you pay interest only on the remaining loan amount.

This makes early repayments very effective in reducing total cost.

Learning how to reduce loan interest legally can help you save a significant amount over the life of your loan.

Secured vs Unsecured Personal Loans

Personal loans are typically unsecured, but in some cases, lenders may offer secured options with lower interest rates.

Unsecured loans are faster to get but may have higher interest rates, while secured loans require collateral but can offer better terms.

Understanding the difference between secured and unsecured loan options can help you choose the right type based on your financial situation.

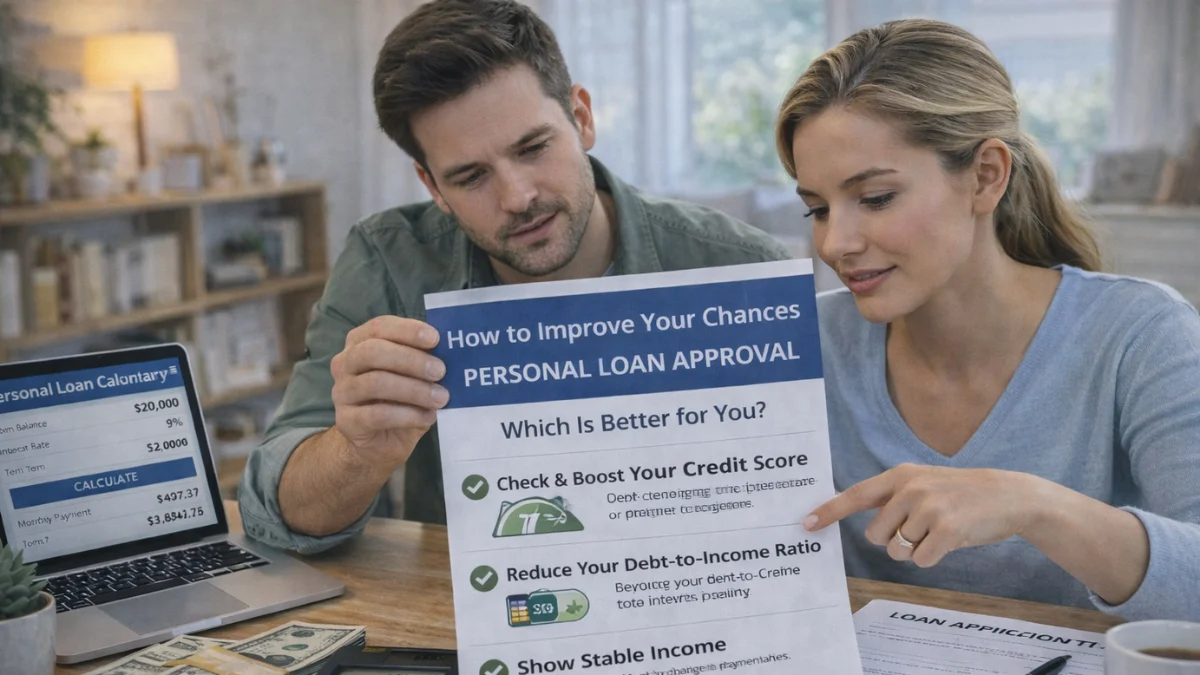

How Lenders Decide Your Eligibility

Not everyone gets approved for a personal loan instantly.

Lenders evaluate several factors, including your income, credit score, employment stability, and existing debts.

A higher credit score and stable income increase your chances of approval and help you secure better interest rates.

If you want to improve your chances, learning about loan eligibility factors can give you a clear idea of what lenders look for.

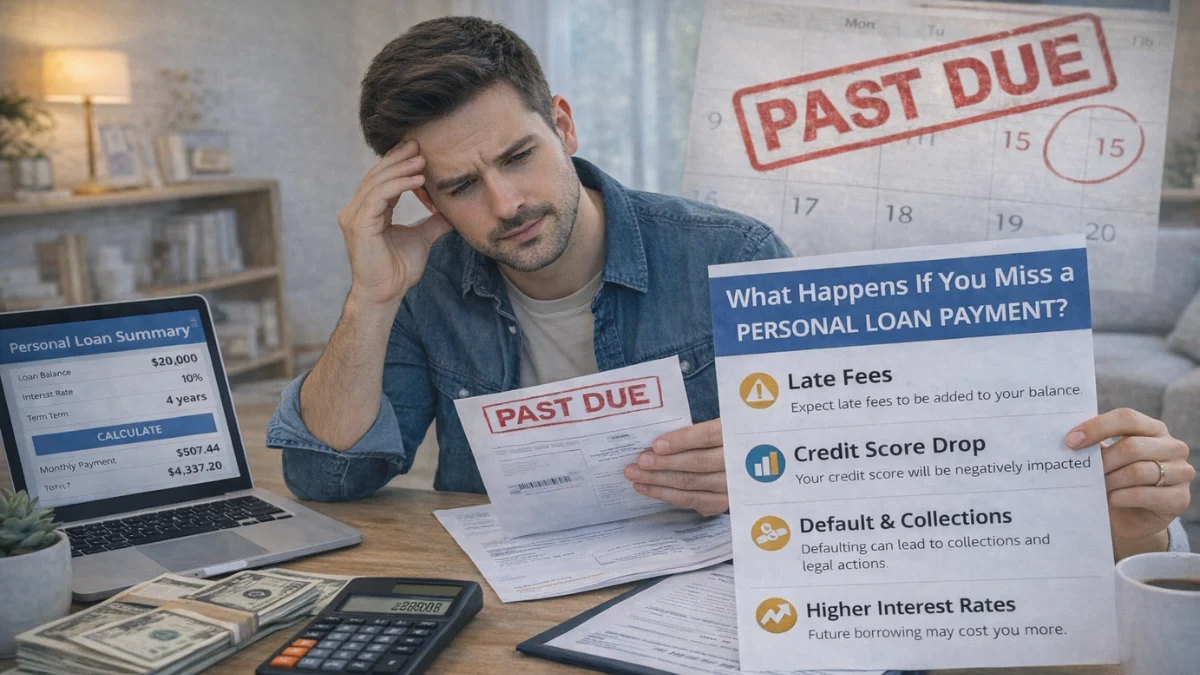

What Happens After You Get the Loan?

Once your loan is approved and disbursed, your repayment journey begins. You are required to pay EMIs every month until the loan is fully repaid.

Missing payments can lead to penalties and damage your credit score. That’s why it’s important to choose a loan amount and EMI that you can comfortably afford.

Understanding what happens when you miss a loan payment can help you avoid serious financial consequences.

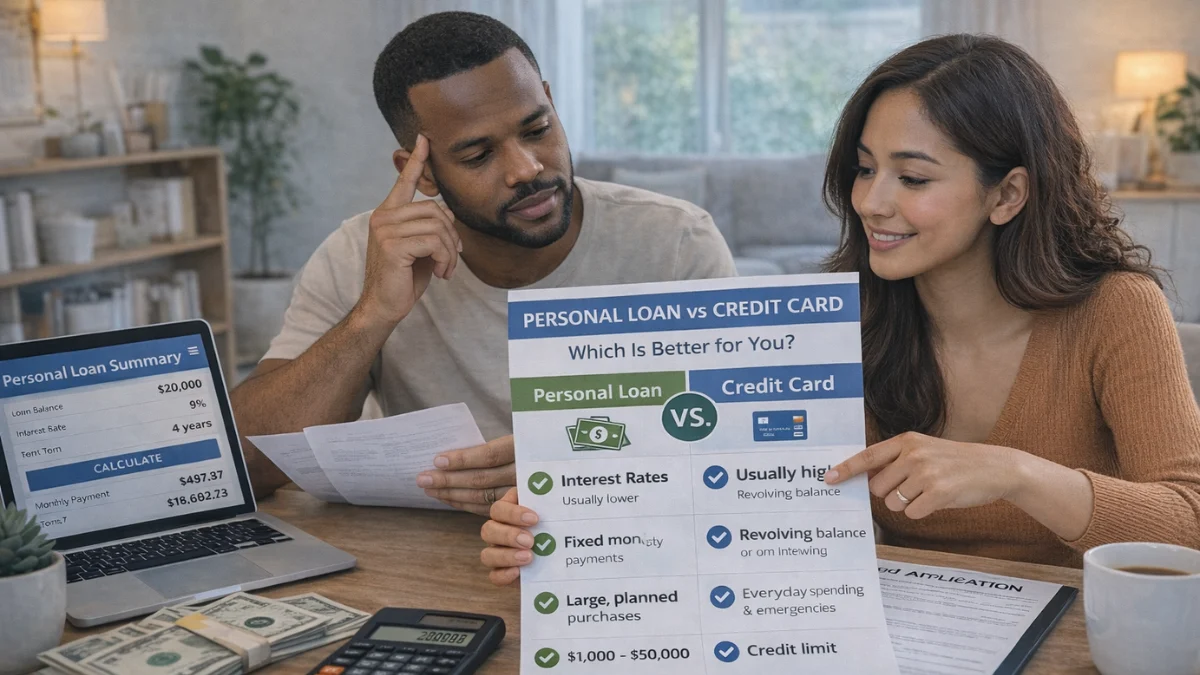

Personal Loan vs Credit Card: Which Is Better?

Many people confuse personal loans with credit cards when it comes to borrowing.

While both allow you to access funds, they work very differently.

Personal loans usually have lower interest rates and fixed repayment schedules, while credit cards offer flexibility but often come with higher interest.

Comparing loan vs credit card options can help you decide which is better for your needs.

How to Get a Personal Loan with Bad Credit

If your credit score is low, getting a personal loan can be challenging—but not impossible.

Some lenders specialize in offering loans to borrowers with lower credit scores, though interest rates may be higher.

Improving your credit profile or choosing the right lender can increase your chances of approval.

You can explore strategies for getting a loan with bad credit to improve your chances and avoid rejection.

Common Mistakes to Avoid When Taking a Personal Loan

Many borrowers make mistakes like borrowing more than they need, choosing long loan terms, or ignoring total interest costs.

These errors can increase your financial burden significantly.

Using a calculator before applying and understanding the full cost of borrowing can help you avoid these issues.

Learning about common borrowing mistakes can protect you from making costly decisions.

Why You Should Understand Personal Loans Before Applying

A personal loan is a powerful financial tool, but only if used wisely.

Understanding how it works helps you borrow responsibly, manage repayments effectively, and avoid unnecessary debt.

Before applying, it’s important to evaluate your needs, compare options, and plan your repayment strategy.

This becomes much easier when you explore a complete guide on how personal loans really work and how to pay less interest, which ties everything together.

Frequently Asked Questions

Conclusion

Understanding what a personal loan is and how it works is the first step toward making smart financial decisions.

It helps you avoid unnecessary costs, choose the right loan, and manage repayments effectively.

Before taking a loan, always analyze your repayment capacity and total cost.

For a deeper understanding of approval strategies, interest reduction, and smart borrowing, explore the full guide on personal loan strategies and smart financial planning to stay in control of your finances.

I create mortgage calculators and simple guides for Mortgage Rates Checker, helping users understand mortgage rates, refinancing, and home loan affordability. Content is for educational purposes only and not financial advice.